4 - Taxation Law

4 - Taxation Law

Download as docx, pdf, or txt

You might also like

- Question 67 (5 Minutes) (Chapter 14)Document59 pagesQuestion 67 (5 Minutes) (Chapter 14)Vu Khanh LeNo ratings yet

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2024 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2024 Edition)No ratings yet

- Syllabus UCC Business Law and Taxation IntegrationDocument9 pagesSyllabus UCC Business Law and Taxation IntegrationArki Torni100% (3)

- Answer Key To QuizzersDocument52 pagesAnswer Key To QuizzersQueen ValleNo ratings yet

- Deed of RescissionDocument2 pagesDeed of RescissionNikkiAndradeNo ratings yet

- Taxation Law Review SyllabusDocument14 pagesTaxation Law Review SyllabusRoxanne Peña100% (2)

- Quiz Compensation Income Pension and Retirement Benefit PDF FreeDocument60 pagesQuiz Compensation Income Pension and Retirement Benefit PDF FreeMichael Brian TorresNo ratings yet

- People V Panis Case DigestDocument1 pagePeople V Panis Case DigestNikkiAndrade100% (4)

- General Milling Corp V CasioDocument3 pagesGeneral Milling Corp V CasioNikkiAndradeNo ratings yet

- Tax1 4compiDocument49 pagesTax1 4compiAnne Marieline Buenaventura100% (2)

- Taxation Law SyllabusDocument10 pagesTaxation Law SyllabusLost StudentNo ratings yet

- Barops Taxation 2020Document241 pagesBarops Taxation 2020Gerry Ombrog100% (1)

- I. General PrinciplesDocument8 pagesI. General PrinciplesJed LipaNo ratings yet

- Bar 2020 Syllabus - TAXDocument9 pagesBar 2020 Syllabus - TAXSBCA Legal Aid CenterNo ratings yet

- 2020 Bar Exam Syllabus in Taxation LawDocument11 pages2020 Bar Exam Syllabus in Taxation LawMyBias KimSeokJinNo ratings yet

- Taxation Law Notes 2020Document9 pagesTaxation Law Notes 2020Kim WaNo ratings yet

- Tax Law Syllabus 2021Document4 pagesTax Law Syllabus 2021Francisco BanguisNo ratings yet

- Syllabus For Taxation Bar Exam 2019Document5 pagesSyllabus For Taxation Bar Exam 2019Vebsie De la CruzNo ratings yet

- Taxation LAW: I. General PrinciplesDocument5 pagesTaxation LAW: I. General PrinciplesclarizzzNo ratings yet

- Taxation Law: I. General PrinciplesDocument11 pagesTaxation Law: I. General PrinciplesCnfsr KayceNo ratings yet

- Tax Syllabus 2019Document6 pagesTax Syllabus 2019Diding BorromeoNo ratings yet

- Proposed Syllabus Taxation 1 Atty. SaniDocument13 pagesProposed Syllabus Taxation 1 Atty. SaniZubair BatuaNo ratings yet

- Taxation 2 Syllabus Atty SaniDocument4 pagesTaxation 2 Syllabus Atty Saniyasser lucmanNo ratings yet

- Income Tax - OutlineDocument5 pagesIncome Tax - OutlineMa. Corazon M. CristobalNo ratings yet

- TAXATION LAW REVIEW TopicsDocument13 pagesTAXATION LAW REVIEW TopicsKimberly RamosNo ratings yet

- J. Bernabe Case Digests - TaxationDocument36 pagesJ. Bernabe Case Digests - TaxationHestia VestaNo ratings yet

- SYLLABUS Tax FOR 2023 BARDocument3 pagesSYLLABUS Tax FOR 2023 BARJournal SP DabawNo ratings yet

- Taxation Laws OnlyDocument4 pagesTaxation Laws Onlyrichard28asentista100% (2)

- Syllabus. Income Tax. Mvavjanuary 15, 2018Document6 pagesSyllabus. Income Tax. Mvavjanuary 15, 2018Christine Ang CaminadeNo ratings yet

- 2019 Bar Examinations TAXATION LAWDocument10 pages2019 Bar Examinations TAXATION LAWEric RamilNo ratings yet

- Tax Rev SyllabusDocument14 pagesTax Rev SyllabusIanLightPajaroNo ratings yet

- Taxation Law 1Document9 pagesTaxation Law 1Eunice NavarroNo ratings yet

- Aw On Axation: Coverage 2016 B EDocument14 pagesAw On Axation: Coverage 2016 B Etito leeNo ratings yet

- An Act Amending The National Internal Revenue Code, As Amended, and For Other PurposesDocument12 pagesAn Act Amending The National Internal Revenue Code, As Amended, and For Other PurposesVada De Villa RodriguezNo ratings yet

- ACCTAX3 SyllabusDocument5 pagesACCTAX3 SyllabusEi Ar TaradjiNo ratings yet

- Paper 11 PDFDocument6 pagesPaper 11 PDFKaysline Oscar CollinesNo ratings yet

- Taxation Course OutlineDocument6 pagesTaxation Course OutlineMawanda Ssekibuule SuudiNo ratings yet

- Tax Review Syllabus A.Y. 2019-2020Document6 pagesTax Review Syllabus A.Y. 2019-2020Kelvin Culajará100% (1)

- Taxrev SyllabusDocument12 pagesTaxrev SyllabusDiane JulianNo ratings yet

- Taxation 2 Course Outline Midterms DraftDocument6 pagesTaxation 2 Course Outline Midterms DraftIra Francia AlcazarNo ratings yet

- Taxation Law: I. General PrinciplesDocument7 pagesTaxation Law: I. General PrinciplesKarinNo ratings yet

- 2.1 Income Tax - General PrinciplesDocument9 pages2.1 Income Tax - General PrinciplesMarco RvsNo ratings yet

- Taxation I Syllabus PDFDocument4 pagesTaxation I Syllabus PDFzeigfred badanaNo ratings yet

- Fundamental of Income TaxationDocument17 pagesFundamental of Income TaxationLilian FredelucesNo ratings yet

- Comprehensive Exam-Income TaxationDocument5 pagesComprehensive Exam-Income TaxationKaren May JimenezNo ratings yet

- Dsadada23 Qedxeqev QQDocument13 pagesDsadada23 Qedxeqev QQCheol-ah KiNo ratings yet

- Finals Syllabus (Tax 02 - Atty. Acas)Document19 pagesFinals Syllabus (Tax 02 - Atty. Acas)AprilNo ratings yet

- Tax I Syllabus - GoDocument8 pagesTax I Syllabus - GoJane SudarioNo ratings yet

- 10 Question Exam Income TaxDocument1 page10 Question Exam Income TaxLei MorteraNo ratings yet

- Assessment 3 Tax 1Document5 pagesAssessment 3 Tax 1Judy Ann GacetaNo ratings yet

- Gross Income With Answer KeyDocument4 pagesGross Income With Answer KeyFallaria Paulo A.No ratings yet

- 06 Gross IncomeDocument23 pages06 Gross IncomeEloisa MonatoNo ratings yet

- TAXREV SANTOSsyllabusDocument7 pagesTAXREV SANTOSsyllabusJoma CoronaNo ratings yet

- Tax Quiz 4Document61 pagesTax Quiz 4Seri CrisologoNo ratings yet

- 06txr Final TaxDocument11 pages06txr Final TaxJemaica BongosiaNo ratings yet

- Tax UpdatesDocument40 pagesTax UpdatesTenshi OideNo ratings yet

- Taxation Law ReviewerDocument18 pagesTaxation Law ReviewerFrancis Puno100% (2)

- Assignment No. 6 Law On Income TaxationDocument1 pageAssignment No. 6 Law On Income TaxationFRANCO LUIS NOVENARIONo ratings yet

- Inclusions in Gross IncomeDocument2 pagesInclusions in Gross Incomeloonie tunesNo ratings yet

- MULTIPLE CHOICE QUESTIONS IN TAX REVIEW Jan 5Document1 pageMULTIPLE CHOICE QUESTIONS IN TAX REVIEW Jan 5Quasi-Delict89% (18)

- Multiple Choice Questions in Tax Review Jan 5Document1 pageMultiple Choice Questions in Tax Review Jan 5Gileah ZuasolaNo ratings yet

- MULTIPLE CHOICE QUESTIONS IN TAX REVIEW Jan 5 PDFDocument1 pageMULTIPLE CHOICE QUESTIONS IN TAX REVIEW Jan 5 PDFGileah ZuasolaNo ratings yet

- MULTIPLE CHOICE QUESTIONS IN TAX REVIEW Jan 5 PDFDocument1 pageMULTIPLE CHOICE QUESTIONS IN TAX REVIEW Jan 5 PDFKyll MarcosNo ratings yet

- Acca - F6 CitDocument131 pagesAcca - F6 CitNile NguyenNo ratings yet

- Income Taxation Quiz 1Document2 pagesIncome Taxation Quiz 1Yi Zara100% (1)

- 1 - Political and International LawDocument17 pages1 - Political and International LawNikkiAndradeNo ratings yet

- Shortened Bar SyllabusDocument4 pagesShortened Bar SyllabusNikkiAndradeNo ratings yet

- Lim Tanhu V RamoleteDocument2 pagesLim Tanhu V RamoleteNikkiAndrade100% (1)

- Domagas Vs JensenDocument2 pagesDomagas Vs JensenNikkiAndrade100% (1)

- Miguel Vs Sandiganbayan-REMDocument2 pagesMiguel Vs Sandiganbayan-REMNikkiAndradeNo ratings yet

- Republic vs. MarcosDocument9 pagesRepublic vs. MarcosNikkiAndradeNo ratings yet

- Avelino Vs CuencoDocument1 pageAvelino Vs CuencoNikkiAndrade100% (5)

- Lim V PeopleDocument6 pagesLim V PeopleNikkiAndradeNo ratings yet

- Sales CasesDocument18 pagesSales CasesEm Asiddao-DeonaNo ratings yet

- Disbursements Through Tax Remittance AdviceDocument3 pagesDisbursements Through Tax Remittance AdvicePostbae GaloneNo ratings yet

- IntxDocument6 pagesIntxSophia KeratinNo ratings yet

- Lesson 2 Tax Laws and Tax AdministrationDocument33 pagesLesson 2 Tax Laws and Tax AdministrationAndrie John BaclaanNo ratings yet

- Value Added Tax: NotesDocument26 pagesValue Added Tax: NotesSamantha AlejandroNo ratings yet

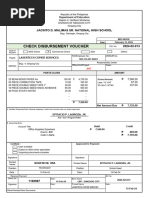

- Jacinto Lasertech PODocument4 pagesJacinto Lasertech POjeffreylois.maestradoNo ratings yet

- 2023-Exercises Law 1Document9 pages2023-Exercises Law 1abelonalysa0No ratings yet

- RR No. 11-2018 SummaryDocument6 pagesRR No. 11-2018 SummaryCaliNo ratings yet

- Tax InterviewDocument1 pageTax InterviewZaim verseNo ratings yet

- All Important Excel Lookup Formulas - Excel Worksheet, Power Query & DAX - 28 Examples! - 365 MECS 08 08-M365ExcelClassDocument171 pagesAll Important Excel Lookup Formulas - Excel Worksheet, Power Query & DAX - 28 Examples! - 365 MECS 08 08-M365ExcelClassMohammed KohailNo ratings yet

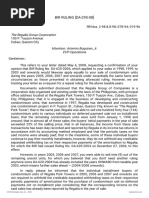

- The Regalia Group Corporation: BIR RULING (DA-295-08)Document4 pagesThe Regalia Group Corporation: BIR RULING (DA-295-08)Johnallen MarillaNo ratings yet

- AOM No. 2022-001 (20-22) - Audit of Accounts and Transactions Brgy. Banggot, BambangDocument25 pagesAOM No. 2022-001 (20-22) - Audit of Accounts and Transactions Brgy. Banggot, BambangGilbert D. AfallaNo ratings yet

- PCSC vs. CIRDocument15 pagesPCSC vs. CIRrobinNo ratings yet

- Cards Application Form1Document29 pagesCards Application Form1ygy1730632298No ratings yet

- Vat Return All Annex S 1822020Document122 pagesVat Return All Annex S 1822020Syeda Mariyam ZehraNo ratings yet

- BIR - Remittance of CWT (Form 1606) Discussion 1Document92 pagesBIR - Remittance of CWT (Form 1606) Discussion 1Roy RitagaNo ratings yet

- Cloud AP IADocument21 pagesCloud AP IAmails.rakesh94No ratings yet

- APV 139540 202309 1-15 PCF REPLENISHMENT-BAT (TY) Princess Camille MacatangayDocument15 pagesAPV 139540 202309 1-15 PCF REPLENISHMENT-BAT (TY) Princess Camille MacatangayEniger CaspeNo ratings yet

- Annual Income Tax Return: I I 0 1 1 I I 0 1 2 I I 0 1 1 I I 0 1 1 I I 0 1 2 I I 0 1 3Document5 pagesAnnual Income Tax Return: I I 0 1 1 I I 0 1 2 I I 0 1 1 I I 0 1 1 I I 0 1 2 I I 0 1 3Jhanrich MatalaNo ratings yet

- 90,000 40,000 102,000 Correct Answer 110,000 100,000 300,000 312,000 314,000Document11 pages90,000 40,000 102,000 Correct Answer 110,000 100,000 300,000 312,000 314,000Hazel Grace PaguiaNo ratings yet

- Taxation of Partnerships and Partners Learning ObjectivesDocument8 pagesTaxation of Partnerships and Partners Learning ObjectivesClaire BarbaNo ratings yet

- Memo Bir sECDocument2 pagesMemo Bir sECalbycadavisNo ratings yet

- 6 Activities For Business Structure & TaxationDocument16 pages6 Activities For Business Structure & TaxationDawit TilahunNo ratings yet

- Taxable Corporatio Ns by Enrico D. Tabag, CPA, MBADocument83 pagesTaxable Corporatio Ns by Enrico D. Tabag, CPA, MBATrisha RafalloNo ratings yet

- Taxation Preweek and Additional MaterialsDocument26 pagesTaxation Preweek and Additional MaterialsMarvin ClementeNo ratings yet

- Liabilities Exercises SolutionsDocument8 pagesLiabilities Exercises Solutionsthanh subNo ratings yet

- Final Tax On Passive Income For NuDocument6 pagesFinal Tax On Passive Income For NuLynn TaneoNo ratings yet

- Taxation MCQ (Laco)Document12 pagesTaxation MCQ (Laco)Marie GrayNo ratings yet

- BBLL enDocument13 pagesBBLL enBorah SashankaNo ratings yet