0% found this document useful (0 votes)

398 viewsPearson R Correlation

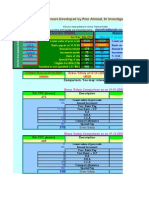

Pearson's correlation coefficient measures the linear correlation between two variables X and Y. It has a value between +1 and -1, where 1 is total positive linear correlation, 0 is no linear correlation, and -1 is total negative linear correlation. The coefficient is calculated as the covariance of the two variables divided by the product of their standard deviations. It is a widely used measure of how two variables change together or are related to each other.

Uploaded by

Ammar SaleemCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

398 viewsPearson R Correlation

Pearson's correlation coefficient measures the linear correlation between two variables X and Y. It has a value between +1 and -1, where 1 is total positive linear correlation, 0 is no linear correlation, and -1 is total negative linear correlation. The coefficient is calculated as the covariance of the two variables divided by the product of their standard deviations. It is a widely used measure of how two variables change together or are related to each other.

Uploaded by

Ammar SaleemCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 2