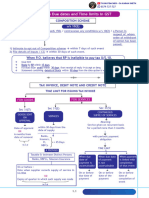

Time & Value of Supply

Time & Value of Supply

Download as pdf or txt

You might also like

- Winfield CaseDocument8 pagesWinfield CaseAbhinandan Singh67% (3)

- Lesson 11 International Aspects of Corporate FinanceDocument17 pagesLesson 11 International Aspects of Corporate Financeman ibe0% (1)

- New Earth Mining Inc.Document16 pagesNew Earth Mining Inc.Asif Rahman100% (1)

- Batch 93 FAR First Preboard February 2023 - SolutionDocument5 pagesBatch 93 FAR First Preboard February 2023 - SolutionlorenzNo ratings yet

- Levy in GST S.No Particulars 1 Time of SupplyDocument7 pagesLevy in GST S.No Particulars 1 Time of SupplyAnonymous ikQZphNo ratings yet

- Chapter 6 - Time of SupplyDocument7 pagesChapter 6 - Time of SupplyDrafts StorageNo ratings yet

- GST 4Document3 pagesGST 4likithaggowdaaNo ratings yet

- 5 Time of SupplyDocument18 pages5 Time of SupplyDhana SekarNo ratings yet

- Time of Supply of ServicesDocument10 pagesTime of Supply of ServicesShiwang AgrawalNo ratings yet

- Time of SupplyDocument31 pagesTime of SupplyNalin KNo ratings yet

- UNIT 2 (4) Time of SupplyDocument15 pagesUNIT 2 (4) Time of SupplySania KhanNo ratings yet

- Time of Supply PDFDocument16 pagesTime of Supply PDFNaveed AnsariNo ratings yet

- GST - Time of Supply of Goods (Summary)Document1 pageGST - Time of Supply of Goods (Summary)Saksham KathuriaNo ratings yet

- All The Due Dates and Time Limits in GSTDocument10 pagesAll The Due Dates and Time Limits in GST2d77gp69kzNo ratings yet

- GST - Documents & Records-May 18Document29 pagesGST - Documents & Records-May 18Sanjay DwivediNo ratings yet

- Time of SupplyDocument23 pagesTime of SupplyvarunagarwalNo ratings yet

- Time of SupplyDocument7 pagesTime of SupplyAghila R.S.No ratings yet

- 4 GST Time and Value of Supply NotesDocument6 pages4 GST Time and Value of Supply NotesMurali Krishnan RNo ratings yet

- Tax Points - Reference Material: Pro Forma InvoicesDocument2 pagesTax Points - Reference Material: Pro Forma Invoicesanon_178447188No ratings yet

- New PPTX PresentationDocument9 pagesNew PPTX PresentationdataprotaxNo ratings yet

- Time of SupplyDocument28 pagesTime of SupplySam RockerNo ratings yet

- Invoicing Under Goods and Service TAXDocument21 pagesInvoicing Under Goods and Service TAXMichealNo ratings yet

- GST For Nov 2022 & May 2023 Exams (GST Time of Supply of ServicesDocument1 pageGST For Nov 2022 & May 2023 Exams (GST Time of Supply of ServicesVikasNo ratings yet

- Time of SupplyDocument6 pagesTime of SupplygriefernjanNo ratings yet

- Time of SupplyDocument7 pagesTime of SupplyTushar MadanNo ratings yet

- TH02TOSDocument2 pagesTH02TOSjainviren34No ratings yet

- Time of SupplyDocument4 pagesTime of SupplyAarushi GuptaNo ratings yet

- Transitional Provisions in GST S.No Particulars 1 Transitional ProvisionsDocument8 pagesTransitional Provisions in GST S.No Particulars 1 Transitional ProvisionsAnonymous ikQZphNo ratings yet

- GST - Lecture 5 - Time of SupplyDocument6 pagesGST - Lecture 5 - Time of SupplyPoke GuruNo ratings yet

- GST Seminar: Hosted By:-Akola Branch of WICASA of ICAIDocument40 pagesGST Seminar: Hosted By:-Akola Branch of WICASA of ICAINavneetNo ratings yet

- EIDT Unit 2 (Notes)Document4 pagesEIDT Unit 2 (Notes)Samarth SahuNo ratings yet

- Transitional ProvisionsDocument21 pagesTransitional ProvisionsRahul AkellaNo ratings yet

- Uncommon GST TopicsDocument36 pagesUncommon GST TopicsEugeniePaxtonNo ratings yet

- Finance DepartmentDocument16 pagesFinance DepartmentAkriti SrivastavaNo ratings yet

- WorksContractServices PraDocument22 pagesWorksContractServices PraManikantaNo ratings yet

- Klein Construction Act Reforms 1Document26 pagesKlein Construction Act Reforms 1hasanNo ratings yet

- Ilovepdf MergedDocument9 pagesIlovepdf Mergedm37384965No ratings yet

- GST PresentationDocument22 pagesGST PresentationSakshi SinghNo ratings yet

- Time of Supply-IDocument50 pagesTime of Supply-IVaibhav GawadeNo ratings yet

- Time and Value of Supply-4Document73 pagesTime and Value of Supply-4Muhammad MehrajNo ratings yet

- Chapter 11 Tax Invoice, Credit and Debit NotesDocument24 pagesChapter 11 Tax Invoice, Credit and Debit Notesjabbi2100No ratings yet

- Time of Supply NotesDocument5 pagesTime of Supply NotesAishuNo ratings yet

- Impact of GST On Real Estate Sector: by Ca Umesh SharmaDocument58 pagesImpact of GST On Real Estate Sector: by Ca Umesh SharmaRavindra PoteNo ratings yet

- 7 Input Tax CreditDocument16 pages7 Input Tax CreditinstainstantuserNo ratings yet

- Ifrs 2Document44 pagesIfrs 2samrawithagos2002No ratings yet

- Basic Concepts of Transition & Invoice I20177804Document28 pagesBasic Concepts of Transition & Invoice I20177804vishalNo ratings yet

- Changes in Service Tax Laws: Prepared By: CA - Narottam Rawat & CA - Ritesh DagaDocument12 pagesChanges in Service Tax Laws: Prepared By: CA - Narottam Rawat & CA - Ritesh DagaAkhil PrasharNo ratings yet

- Finance Quick Guide For Customers English RevDocument3 pagesFinance Quick Guide For Customers English RevMarcelo BorsiniNo ratings yet

- Input Tax credit-GSTDocument17 pagesInput Tax credit-GSTSandhya DangiNo ratings yet

- Recognition of Revenue From Non-Exchange TransactionsDocument31 pagesRecognition of Revenue From Non-Exchange TransactionsRemon ValmonteNo ratings yet

- GST - Tax Invoice, Debit or Credit Notes, Returns, Payment of Tax PDFDocument78 pagesGST - Tax Invoice, Debit or Credit Notes, Returns, Payment of Tax PDFSapna MalikNo ratings yet

- Minerals Australia Guidance Note Supportive Arrangements For Supplier Payment TermsDocument4 pagesMinerals Australia Guidance Note Supportive Arrangements For Supplier Payment Termskhk84jfxchNo ratings yet

- 13 Time of Supply of SerDocument2 pages13 Time of Supply of SerSachin KumarNo ratings yet

- Point of TaxationDocument11 pagesPoint of TaxationAmrit TejaniNo ratings yet

- Tax Invoice, Debit Note and Credit Note PDFDocument29 pagesTax Invoice, Debit Note and Credit Note PDFNaveed AnsariNo ratings yet

- Time of Supply: CMA Bhogavalli Mallikarjuna GuptaDocument5 pagesTime of Supply: CMA Bhogavalli Mallikarjuna Guptagurusha bhallaNo ratings yet

- GSTDocument40 pagesGSTdurairajNo ratings yet

- Idt 3Document10 pagesIdt 3manan agrawalNo ratings yet

- Taxpayer Being Provided Goods or Services?Document2 pagesTaxpayer Being Provided Goods or Services?ycho1992No ratings yet

- GST Handbook EnglishDocument8 pagesGST Handbook EnglishMohd AsadNo ratings yet

- Chapter - 5 Time & Value of SupplyDocument16 pagesChapter - 5 Time & Value of SupplyRaja BahlNo ratings yet

- Charge Under Companies ActDocument13 pagesCharge Under Companies ActAsma SaeedNo ratings yet

- Toa 38 40Document17 pagesToa 38 40Mary Joy AlbandiaNo ratings yet

- Homework - Set - Solutions Finance 2.2 PDFDocument18 pagesHomework - Set - Solutions Finance 2.2 PDFAnonymous EgWT5izpNo ratings yet

- Capital Budgeting 1st PartDocument8 pagesCapital Budgeting 1st PartPeng Guin100% (1)

- The New Swap MathDocument5 pagesThe New Swap MathbrohopparnNo ratings yet

- CFA Level III Mock Exam 5 June, 2017 Revision 1Document35 pagesCFA Level III Mock Exam 5 June, 2017 Revision 1menabavi2No ratings yet

- Project IdentificationDocument89 pagesProject Identificationtadgash4920100% (3)

- 11 ReceivablesDocument4 pages11 ReceivablesuncianojhezrhyllemhaeNo ratings yet

- FM09-CH 21Document4 pagesFM09-CH 21Mukul KadyanNo ratings yet

- SNL Permitting Delay Report-OnlineDocument32 pagesSNL Permitting Delay Report-OnlineheatherNo ratings yet

- Role of Actuary in InsuranceDocument14 pagesRole of Actuary in Insurancerajesh_natarajan_4100% (1)

- Deterministic Cash Flows and The Term Structure of Interest RatesDocument15 pagesDeterministic Cash Flows and The Term Structure of Interest RatesC J Ballesteros MontalbánNo ratings yet

- Model Solutions: Cma December, 2020 Examination Professional Level - I Subject: 101. Intermediate Financial AccountingDocument7 pagesModel Solutions: Cma December, 2020 Examination Professional Level - I Subject: 101. Intermediate Financial AccountingTaslima AktarNo ratings yet

- Partnerships-1Document20 pagesPartnerships-1samuelNo ratings yet

- Mihir Desai - The Finance Function in A Global CorporationDocument5 pagesMihir Desai - The Finance Function in A Global CorporationkaitlinkaitlinflynnNo ratings yet

- Current-Liabilities-Management, Jessa, LausDocument14 pagesCurrent-Liabilities-Management, Jessa, LausAldrin Jon Madamba, MAED-ELMNo ratings yet

- Module 5 - Ia2 Final CBLDocument13 pagesModule 5 - Ia2 Final CBLErik Lorenz Palomares0% (1)

- Cash Management Theory and QuestionsDocument9 pagesCash Management Theory and QuestionsAyush PrakashNo ratings yet

- Chu de 3 Nhom 6 Hay PDFDocument10 pagesChu de 3 Nhom 6 Hay PDFNhư NhưNo ratings yet

- Question BankDocument453 pagesQuestion BankkaushikagarwalNo ratings yet

- Exercise InvestmentsDocument14 pagesExercise InvestmentsAlizah Lariosa Bucot43% (7)

- Chapter 10 (Stock Valuation) ClassDocument58 pagesChapter 10 (Stock Valuation) ClasswstNo ratings yet

- PPT-Economics - Unit 1Document53 pagesPPT-Economics - Unit 1Karan SinghNo ratings yet

- ACCA FM TuitionExam CBE 2021-2022 Qs JG21Jan SPi15MarDocument14 pagesACCA FM TuitionExam CBE 2021-2022 Qs JG21Jan SPi15MarchimbanguraNo ratings yet

- Metals and Engineering Corporation: Feasibility Study ONDocument15 pagesMetals and Engineering Corporation: Feasibility Study ONkinfegetaNo ratings yet

- Valuations - DamodaranDocument308 pagesValuations - DamodaranharleeniitrNo ratings yet

- Quiz 4 With SolutionDocument5 pagesQuiz 4 With SolutionKarl Lincoln TemporosaNo ratings yet