Download as pdf or txt

You might also like

- Kolnai - On DisgustDocument63 pagesKolnai - On DisgustEverton Rangel100% (1)

- Uncommon GST TopicsDocument36 pagesUncommon GST TopicsEugeniePaxtonNo ratings yet

- Time and Value of Supply-4Document73 pagesTime and Value of Supply-4Muhammad MehrajNo ratings yet

- On GST 1Document56 pagesOn GST 1Gayathri Nathan100% (1)

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument56 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaRithik S AnandNo ratings yet

- Time of SupplyDocument31 pagesTime of SupplyNalin KNo ratings yet

- 5.time and Value of Supply18Document54 pages5.time and Value of Supply18Naveen HanchinamaniNo ratings yet

- Time of SupplyDocument6 pagesTime of SupplygriefernjanNo ratings yet

- Chapter 5 WhentoPayTaxonSupplyofGoods ServicesDocument24 pagesChapter 5 WhentoPayTaxonSupplyofGoods ServicesDR. PREETI JINDALNo ratings yet

- Chapter 6 - Time of SupplyDocument7 pagesChapter 6 - Time of SupplyDrafts StorageNo ratings yet

- UNIT 2 (4) Time of SupplyDocument15 pagesUNIT 2 (4) Time of SupplySania KhanNo ratings yet

- Time of SupplyDocument7 pagesTime of SupplyTushar MadanNo ratings yet

- Time of Supply (New)Document14 pagesTime of Supply (New)naveenaspblrNo ratings yet

- Time of SupplyDocument12 pagesTime of SupplyKshitij TandonNo ratings yet

- Levy in GST S.No Particulars 1 Time of SupplyDocument7 pagesLevy in GST S.No Particulars 1 Time of SupplyAnonymous ikQZphNo ratings yet

- 6.time and Value of SupplyDocument54 pages6.time and Value of SupplyRahul GhosaleNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- TOS of Goods+services NotesDocument7 pagesTOS of Goods+services NotesKanha MishraNo ratings yet

- Project On GSTDocument16 pagesProject On GSTSonal JhaNo ratings yet

- Rules For Determining Time of Supply For Goods and Services1Document9 pagesRules For Determining Time of Supply For Goods and Services1KhushiNo ratings yet

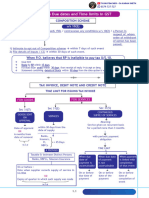

- Tax Invoice, Debit Note and Credit Note PDFDocument29 pagesTax Invoice, Debit Note and Credit Note PDFNaveed AnsariNo ratings yet

- TOS and VOS Notes Sent To B.Com Hons 2023Document38 pagesTOS and VOS Notes Sent To B.Com Hons 2023ANSHIKA SHUKLANo ratings yet

- Time of Supply PDFDocument16 pagesTime of Supply PDFNaveed AnsariNo ratings yet

- Time of Supply NotesDocument5 pagesTime of Supply NotesAishuNo ratings yet

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument54 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaManjunathreddy SeshadriNo ratings yet

- TH02TOSDocument2 pagesTH02TOSjainviren34No ratings yet

- GST Divyastra CH 5 Time of Supply RDocument10 pagesGST Divyastra CH 5 Time of Supply Rabhishek334ambaniandassociatesNo ratings yet

- Time of SupplyDocument28 pagesTime of SupplySam RockerNo ratings yet

- GST - Lecture 5 - Time of SupplyDocument6 pagesGST - Lecture 5 - Time of SupplyPoke GuruNo ratings yet

- 4 GST Time and Value of Supply NotesDocument6 pages4 GST Time and Value of Supply NotesMurali Krishnan RNo ratings yet

- Time of SupplyDocument4 pagesTime of SupplyAarushi GuptaNo ratings yet

- Time & Value of SupplyDocument2 pagesTime & Value of SupplyRahul NegiNo ratings yet

- All The Due Dates and Time Limits in GSTDocument10 pagesAll The Due Dates and Time Limits in GST2d77gp69kzNo ratings yet

- Invoicing Under GSTDocument53 pagesInvoicing Under GSTkomal tanwaniNo ratings yet

- Time of SupplyDocument27 pagesTime of Supplyishita sabooNo ratings yet

- GST Practice Session 5 PDFDocument58 pagesGST Practice Session 5 PDFadvrashmichhapariaNo ratings yet

- Time of Supply-20Document44 pagesTime of Supply-20Sidhant GoyalNo ratings yet

- Reverse Charge Mechanism Under GSTDocument7 pagesReverse Charge Mechanism Under GSTramaiahNo ratings yet

- GST - Time of Supply of Goods (Summary)Document1 pageGST - Time of Supply of Goods (Summary)Saksham KathuriaNo ratings yet

- Time of Supply: CMA Bhogavalli Mallikarjuna GuptaDocument5 pagesTime of Supply: CMA Bhogavalli Mallikarjuna Guptagurusha bhallaNo ratings yet

- 4 Time of SupplyDocument43 pages4 Time of SupplynashwauefaNo ratings yet

- Time of Supply of ServicesDocument10 pagesTime of Supply of ServicesShiwang AgrawalNo ratings yet

- Unit II - Part IV - Revised - Time and Value of Supply 04-08-2021Document9 pagesUnit II - Part IV - Revised - Time and Value of Supply 04-08-2021Milan ChandaranaNo ratings yet

- GST1Document25 pagesGST1DeepikaNo ratings yet

- Chapter 11 Tax Invoice, Credit and Debit NotesDocument24 pagesChapter 11 Tax Invoice, Credit and Debit Notesjabbi2100No ratings yet

- Chapter - 5 Time & Value of SupplyDocument16 pagesChapter - 5 Time & Value of SupplyRaja BahlNo ratings yet

- GST 4Document3 pagesGST 4likithaggowdaaNo ratings yet

- Summary of Section 12-14Document5 pagesSummary of Section 12-14Yashwanth Sonu0% (1)

- Amendment in Section 43B of Income Tax Related To MSME - Taxguru - inDocument5 pagesAmendment in Section 43B of Income Tax Related To MSME - Taxguru - indinesh kumarNo ratings yet

- Basic Concepts of Transition & Invoice I20177804Document28 pagesBasic Concepts of Transition & Invoice I20177804vishalNo ratings yet

- 04 Time of Supply GST 22Document22 pages04 Time of Supply GST 22AmanNo ratings yet

- New PPTX PresentationDocument9 pagesNew PPTX PresentationdataprotaxNo ratings yet

- GST - Documents & Records-May 18Document29 pagesGST - Documents & Records-May 18Sanjay DwivediNo ratings yet

- Letter Template-1Document21 pagesLetter Template-1QwertyNo ratings yet

- 6input Tax Credit1867ihhgghDocument35 pages6input Tax Credit1867ihhgghvinit tandelNo ratings yet

- Finance DepartmentDocument16 pagesFinance DepartmentAkriti SrivastavaNo ratings yet

- MCQs On Chap 10 ADocument11 pagesMCQs On Chap 10 AAman AgarwalNo ratings yet

- 4600023821, dt.14.09.2022 IHTE OrderDocument11 pages4600023821, dt.14.09.2022 IHTE Ordernavap ramukNo ratings yet

- 13 Time of Supply of SerDocument2 pages13 Time of Supply of SerSachin KumarNo ratings yet

- Tax Invoice & E-Way BillDocument33 pagesTax Invoice & E-Way BillDayal SinghNo ratings yet

- Extinguishment of ObligationDocument5 pagesExtinguishment of ObligationMesje Trumph100% (1)

- EC2C90B8 - Anurat Anantanatorn CVDocument2 pagesEC2C90B8 - Anurat Anantanatorn CVDiyah NurmawatiNo ratings yet

- Jurisprudence On Recalling The WitnessDocument2 pagesJurisprudence On Recalling The Witnessfennyrose nunalaNo ratings yet

- Outline For A Typical Wedding in VietnamDocument3 pagesOutline For A Typical Wedding in VietnamTrang Thái Nguyễn ThuNo ratings yet

- Lec#2 TaklifiDocument20 pagesLec#2 TaklifiSaba BatoolNo ratings yet

- DAO - 2015-07 - IsO CertificationDocument4 pagesDAO - 2015-07 - IsO Certificationjoycesapla18No ratings yet

- Tort Exam 2020 ADocument4 pagesTort Exam 2020 ASUTHARSHINI TAMILSELVAMNo ratings yet

- Hlhs 105 Sellersburg Master Check List 20141Document4 pagesHlhs 105 Sellersburg Master Check List 20141api-274660713No ratings yet

- Diversity & Inclusion in Tech: A Practical Guide For EntrepreneursDocument73 pagesDiversity & Inclusion in Tech: A Practical Guide For EntrepreneursDomagoj Bakota100% (1)

- Dissertation 14 Points de WilsonDocument4 pagesDissertation 14 Points de WilsonWillYouWriteMyPaperForMeCanada100% (1)

- Obsessive-Compulsive Disorder 0Document10 pagesObsessive-Compulsive Disorder 0Faris Aziz PridiantoNo ratings yet

- Meeting 1 - Greetings and IntroductionsDocument23 pagesMeeting 1 - Greetings and Introductionsadelia kusmiajiNo ratings yet

- FNB Script 2022Document5 pagesFNB Script 2022nhel d.No ratings yet

- Enq-2333 - Tender Resume - Rev.0 - Lamprell - Crpo 125 & 126 Offshore FacilitiesDocument23 pagesEnq-2333 - Tender Resume - Rev.0 - Lamprell - Crpo 125 & 126 Offshore FacilitiesNIRBHAY TIWARYNo ratings yet

- Opmt Case StudyDocument7 pagesOpmt Case StudysapnashekhawatNo ratings yet

- Home Is Where The Heart IsDocument1 pageHome Is Where The Heart IsIrfan SayedNo ratings yet

- Coron Span: Wrecks OFDocument78 pagesCoron Span: Wrecks OFMaximNo ratings yet

- Airbus Procurement Organisation Major Suppliers June2015Document11 pagesAirbus Procurement Organisation Major Suppliers June2015Mohit OstwalNo ratings yet

- Resource Planning PolicyDocument3 pagesResource Planning Policymadhvi GajjarNo ratings yet

- Revision4 Variance1Document7 pagesRevision4 Variance1adamNo ratings yet

- Characteristics of The CallerDocument35 pagesCharacteristics of The CallerHarun MusaNo ratings yet

- Structural Design Criteria - Gemini SpacecraftDocument102 pagesStructural Design Criteria - Gemini SpacecraftBob AndrepontNo ratings yet

- Yoga Varga Yoga Givers Results Ascribed To Yoga Brief Definition of YogaDocument2 pagesYoga Varga Yoga Givers Results Ascribed To Yoga Brief Definition of YogaboraNo ratings yet

- Tourism in LebanonDocument11 pagesTourism in LebanonSarah ShamiNo ratings yet

- InformationDocument2 pagesInformationkathleenanne2No ratings yet

- Euthenics 01act1Document1 pageEuthenics 01act1Dheniel AmuraoNo ratings yet

- Mahatma Gandhi and The USA PDFDocument56 pagesMahatma Gandhi and The USA PDFHariNo ratings yet

- Prelim Exam - Forum 1Document3 pagesPrelim Exam - Forum 1Adam CuencaNo ratings yet

- Group 1 Finance Presentation - BSTM1BDocument17 pagesGroup 1 Finance Presentation - BSTM1BMark DavidNo ratings yet