Business Economics Complete

Business Economics Complete

Download as pdf or txt

You might also like

- Managerial EconomicsDocument248 pagesManagerial EconomicsGaurav gusai100% (1)

- ME Unit1-5 NotesDocument15 pagesME Unit1-5 Notesshruthijg866No ratings yet

- MEFADocument23 pagesMEFAR̶e̶c̶o̶n̶n̶e̶c̶t̶i̶n̶g̶ M̶e̶No ratings yet

- ME UNIT 1Document5 pagesME UNIT 1Aliya NasarNo ratings yet

- Solved Qustion Pe 4 Year - RemovedDocument109 pagesSolved Qustion Pe 4 Year - RemovedHemant Dnyaneshwar JakateNo ratings yet

- Important Questions & AnswerDocument76 pagesImportant Questions & Answer19JJ-1253 asrith SriramojuNo ratings yet

- EEA-Unit-2-Detailed NotesDocument27 pagesEEA-Unit-2-Detailed Noteshimajashree06No ratings yet

- UNIT 1Document12 pagesUNIT 1Aliya NasarNo ratings yet

- ME1Document37 pagesME1hemaNo ratings yet

- Economics PPRDocument22 pagesEconomics PPRpriyankaverma7421No ratings yet

- Introduction To Managerial EconomicsDocument70 pagesIntroduction To Managerial EconomicsSavantNo ratings yet

- Eco Imp Q Internals With SolutionDocument14 pagesEco Imp Q Internals With Solutionsaspara2022No ratings yet

- Introduction To Managerial EconomicsDocument28 pagesIntroduction To Managerial EconomicsAnweshaNo ratings yet

- Engineering Economics and Accountancy Final PPT Unit-1Document64 pagesEngineering Economics and Accountancy Final PPT Unit-1Shashi KUMARNo ratings yet

- Managerial Economics MidDocument18 pagesManagerial Economics MidSIDDHARTHNo ratings yet

- MEch101 PindyckDocument15 pagesMEch101 PindyckBiz E-ComNo ratings yet

- Engineering Economics Imon11Document7 pagesEngineering Economics Imon1181No ratings yet

- Fy EconomicsDocument33 pagesFy Economicssontakkeashmit0No ratings yet

- Microeconomics (1)Document11 pagesMicroeconomics (1)Flink pikeNo ratings yet

- Micro Economics NotesDocument28 pagesMicro Economics NotestawandaNo ratings yet

- ECONOMICS END SEM STUDY MATERIALDocument21 pagesECONOMICS END SEM STUDY MATERIALaryanparmar1601No ratings yet

- Chapter-1: Managerial EconomicsDocument24 pagesChapter-1: Managerial EconomicsVivek SharmaNo ratings yet

- A Review in Managerial Economics: Prepared By: Jeams E. VidalDocument8 pagesA Review in Managerial Economics: Prepared By: Jeams E. Vidaljeams vidalNo ratings yet

- UNIT 1 EAMSDocument55 pagesUNIT 1 EAMSNadipelli SougandhiNo ratings yet

- MEFADocument38 pagesMEFA20eg112247No ratings yet

- Principles of Economics - UpdatedDocument72 pagesPrinciples of Economics - UpdatedHabibullah Sarker0% (1)

- MA U2Document10 pagesMA U2Priyanshu SinghNo ratings yet

- MBA Semester 1 MB0042Document12 pagesMBA Semester 1 MB0042Ravi BijalwanNo ratings yet

- BE AssignmentDocument8 pagesBE Assignmenttanishqkumar060No ratings yet

- Basic Concepts and Principles of EconomicsDocument23 pagesBasic Concepts and Principles of EconomicsAnurag ShuklaNo ratings yet

- Managerial EconomicsDocument8 pagesManagerial EconomicsBalakumar ViswanathanNo ratings yet

- Economics NotesDocument8 pagesEconomics Notes19281565No ratings yet

- Economics:: According To Prof. Joel Dean "The Purpose of Managerial Economics Is ToDocument12 pagesEconomics:: According To Prof. Joel Dean "The Purpose of Managerial Economics Is Toravi.youNo ratings yet

- Manegerial EconomicsDocument7 pagesManegerial Economicsmusharf2022bciv068No ratings yet

- Economics 1Document77 pagesEconomics 1Sravaan ReddyNo ratings yet

- HSMCDocument8 pagesHSMCankitasahasaha008No ratings yet

- Mangerial EconomicsDocument353 pagesMangerial Economicsrajan2778No ratings yet

- Unit 1Document51 pagesUnit 1Anonymous WVEy0mgGKNo ratings yet

- Economic Analysis For Business Decisions 103Document31 pagesEconomic Analysis For Business Decisions 103umeshshinde614No ratings yet

- Unit - 1Document21 pagesUnit - 1faizancscmailNo ratings yet

- Me Nov2023 SolutionDocument18 pagesMe Nov2023 Solutionshruthijg866No ratings yet

- Module 2 - Demand Analysis and ForecastingDocument6 pagesModule 2 - Demand Analysis and ForecastingNash Christopher DiazNo ratings yet

- EconomicsDocument57 pagesEconomicsSherwin RafelNo ratings yet

- UNIT 1 ECONOMICS Notes MBADocument5 pagesUNIT 1 ECONOMICS Notes MBAMegha ChoudharyNo ratings yet

- Managerial Eco-1Document28 pagesManagerial Eco-1YoNo ratings yet

- EconomicsDocument61 pagesEconomicsHIDDEN Life OF 【शैलेष】No ratings yet

- Demand ForecastingDocument28 pagesDemand ForecastingRamteja SpuranNo ratings yet

- Module 1 - Introduction To Managerial EconomicsDocument6 pagesModule 1 - Introduction To Managerial EconomicsNash Christopher DiazNo ratings yet

- MICRO ECONOMICSDocument21 pagesMICRO ECONOMICSns6115173No ratings yet

- The Entrepreneurs. It Provides Remedies For Overcoming Such Problems in BusinessDocument16 pagesThe Entrepreneurs. It Provides Remedies For Overcoming Such Problems in Businessremruata rascalralteNo ratings yet

- Economics PPT 1Document81 pagesEconomics PPT 1Durgesh SinghNo ratings yet

- EconomicsDocument16 pagesEconomicsShahab AhmedNo ratings yet

- Mangerialeconomics 150313132610 Conversion Gate01Document394 pagesMangerialeconomics 150313132610 Conversion Gate01agustinn agustinNo ratings yet

- Unit 1Document6 pagesUnit 1prateeksharma3358No ratings yet

- Managerial Economics KMBN102Document31 pagesManagerial Economics KMBN102Shivani PandeyNo ratings yet

- Economics of Effective ManagementDocument37 pagesEconomics of Effective Managementnavuhb007No ratings yet

- Value-based Marketing Strategy: Pricing and Costs for Relationship MarketingFrom EverandValue-based Marketing Strategy: Pricing and Costs for Relationship MarketingNo ratings yet

- Economics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsFrom EverandEconomics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsNo ratings yet

- Mocroeconomics Notes Week2 PresentationDocument43 pagesMocroeconomics Notes Week2 PresentationSakshiNo ratings yet

- Basic Microeconomics Module 2Document10 pagesBasic Microeconomics Module 2jessamaepinas5No ratings yet

- Introduction To Industry and Company Analysis: Presenter Venue DateDocument29 pagesIntroduction To Industry and Company Analysis: Presenter Venue DatePierre TurgotNo ratings yet

- UNIT 6 - Inventory ManagementDocument48 pagesUNIT 6 - Inventory Managementrub786No ratings yet

- The Gravity ModelDocument47 pagesThe Gravity Modelsumanta.dasNo ratings yet

- Chapter 4 Practice QuestionsDocument2 pagesChapter 4 Practice QuestionsNomvuma GubesaNo ratings yet

- Soal Latihan AkhirDocument5 pagesSoal Latihan AkhirWira Suhendra TanjungNo ratings yet

- Chapter 20 Real Estate Development and InvestmentDocument13 pagesChapter 20 Real Estate Development and InvestmentRy.KristNo ratings yet

- Risk Identification Map For A Fashion Retail Supply ChainDocument9 pagesRisk Identification Map For A Fashion Retail Supply ChainErick CaizaNo ratings yet

- A Study of Customer Satisfaction Towards Organic India in LucknowDocument30 pagesA Study of Customer Satisfaction Towards Organic India in LucknowChandanNo ratings yet

- A Case Study On Dabur LTDDocument3 pagesA Case Study On Dabur LTDgarimaamityNo ratings yet

- MIcro Tutorial 5 ANSDocument5 pagesMIcro Tutorial 5 ANSBintang David SusantoNo ratings yet

- C2525-GL Global Consumer Electronics Manufacturing Industry ReportDocument39 pagesC2525-GL Global Consumer Electronics Manufacturing Industry ReportYuan YaoNo ratings yet

- Focus: The Concept of Modern MarketingDocument21 pagesFocus: The Concept of Modern Marketingnew232323No ratings yet

- Simulated Examination in Agricultural Economics and Marketing (Post-Test) Name - Score - General DirectionsDocument10 pagesSimulated Examination in Agricultural Economics and Marketing (Post-Test) Name - Score - General Directionsmaica balaoasNo ratings yet

- Ncuk Ify Econs Eos1 V2 2122Document8 pagesNcuk Ify Econs Eos1 V2 2122callista.1109088No ratings yet

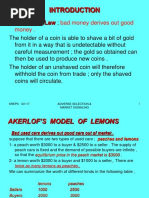

- Bad Money Derives Out Good Money .: Greshman 'S LawDocument39 pagesBad Money Derives Out Good Money .: Greshman 'S LawdscsdxcNo ratings yet

- Instruments of Trade PolicyDocument38 pagesInstruments of Trade PolicyADHADUK RONS MAHENDRABHAINo ratings yet

- Cambridge International AS & A Level: Economics 9708/12Document12 pagesCambridge International AS & A Level: Economics 9708/12Vũ Minh ThưNo ratings yet

- Micro Economics II Monopolistic CompetitionDocument11 pagesMicro Economics II Monopolistic Competitiontegegn mogessieNo ratings yet

- Elasticity Indices For Economic Analysis: A Case Study For Hydrous Ethanol and Gasoline in BrazilDocument12 pagesElasticity Indices For Economic Analysis: A Case Study For Hydrous Ethanol and Gasoline in Brazilsomewhere_below6762No ratings yet

- Glossary of Key Terms: International EconomicsDocument21 pagesGlossary of Key Terms: International EconomicsAjay KaundalNo ratings yet

- Macroeconomics Canadian 8th Edition Sayre Test Bank 1Document36 pagesMacroeconomics Canadian 8th Edition Sayre Test Bank 1marychaveznpfesgkmwx98% (50)

- Business Plan (Document32 pagesBusiness Plan (Antonio Seares100% (3)

- Chapter 1-5Document28 pagesChapter 1-5Jericho CarabidoNo ratings yet

- IB Notes UnemploymentDocument14 pagesIB Notes UnemploymentAnderson MaradzaNo ratings yet

- BBADocument12 pagesBBAonuplus9363No ratings yet

- DINOLETEDocument9 pagesDINOLETEMelvyn LedesmaNo ratings yet

- Marketing Project Report On Advertising EffectivenessDocument33 pagesMarketing Project Report On Advertising EffectivenessParteek MahajanNo ratings yet

- AAE 120 Agricultural Marketing I Learning Log: Week 3 Name: Lopez, Jhun Jhun T. Section: AAE 120 Section C Student No.: 2018-04344Document2 pagesAAE 120 Agricultural Marketing I Learning Log: Week 3 Name: Lopez, Jhun Jhun T. Section: AAE 120 Section C Student No.: 2018-04344Jhun Jhun LopezNo ratings yet