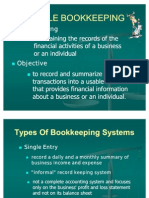

Bookkeeping

Bookkeeping

Download as ppt, pdf, or txt

You might also like

- 06 REO BASIC HO-MAS VarianceDocument11 pages06 REO BASIC HO-MAS VarianceMichelle Angelaine Manalang100% (1)

- Bueno MarketingDocument31 pagesBueno MarketingEnges Formula100% (1)

- Bookkeeping Made EasyDocument19 pagesBookkeeping Made Easycriss_relu100% (4)

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- Retail Pro 9 User's Guide: Chapter 10. Recording Sales and ReturnsDocument175 pagesRetail Pro 9 User's Guide: Chapter 10. Recording Sales and ReturnsRyan corominas100% (1)

- Bookkeeping Training ManualDocument36 pagesBookkeeping Training ManualRodolfo CorpuzNo ratings yet

- Bookkeeping ExamDocument6 pagesBookkeeping Examhanny6135No ratings yet

- Bookkeeping Forms and Templates BookDocument33 pagesBookkeeping Forms and Templates Bookkentkun100% (5)

- Bookkeeping BasicsDocument19 pagesBookkeeping BasicsAbeer Shennawy0% (1)

- Bookkeeping Handouts (Basic Comp)Document8 pagesBookkeeping Handouts (Basic Comp)raquelNo ratings yet

- CBC Bookkeeping NC IIIDocument85 pagesCBC Bookkeeping NC IIIDhet Pas-Men100% (7)

- Simple BookkeepingDocument33 pagesSimple BookkeepingNlNl Palmes BermeoNo ratings yet

- Cooperative BookkeepingDocument41 pagesCooperative Bookkeepingjaydeeado67% (6)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Case Analysis LongchampDocument7 pagesCase Analysis LongchampPaula Andrea GarciaNo ratings yet

- BookkeepingDocument63 pagesBookkeepingRheneir Mora100% (12)

- Bookkeeping Course Syllabus - SDPDFDocument0 pagesBookkeeping Course Syllabus - SDPDFjasonmendez2010No ratings yet

- Training Manual Bookkeeping Financial & ManagementDocument81 pagesTraining Manual Bookkeeping Financial & ManagementJhodie Anne Isorena100% (2)

- 1 Learn-Bookkeeping Pg81Document101 pages1 Learn-Bookkeeping Pg81Jose Mendee100% (1)

- BookkeepingDocument93 pagesBookkeepingIc Abacan100% (5)

- Book-Keeping: Jayant Sethia C.A.FinalistDocument29 pagesBook-Keeping: Jayant Sethia C.A.FinalistShreekumar100% (1)

- Competency-Based Curriculum: A. Course DesignDocument48 pagesCompetency-Based Curriculum: A. Course DesignRheysan Sandro100% (1)

- To The: Course OnDocument48 pagesTo The: Course OnMilagros Cardona100% (9)

- Earn More With An Industry Recognised Bookkeeping Qualification!Document11 pagesEarn More With An Industry Recognised Bookkeeping Qualification!Lilia0% (1)

- Introduction To Bookkeeping and Accounting PrintableDocument68 pagesIntroduction To Bookkeeping and Accounting PrintableDimitra100% (2)

- Accounting For Non-AccountantsDocument15 pagesAccounting For Non-AccountantsMarlou Paige Cortes100% (1)

- What Are The Basics of Bookkeeping?Document15 pagesWhat Are The Basics of Bookkeeping?AdeNo ratings yet

- Bookkeeping 101: A Comprehensive Guide For The Self-EmployedDocument23 pagesBookkeeping 101: A Comprehensive Guide For The Self-EmployedMark Anthony Bartolome Carig100% (3)

- Bookkeeping NC 3 Review GuideDocument6 pagesBookkeeping NC 3 Review GuideCatherine Hidalgo100% (2)

- Bookkeeping Basics EbookDocument6 pagesBookkeeping Basics Ebookredz00No ratings yet

- NC3 Bookeeping Practice Set Answer (Blank Form)Document29 pagesNC3 Bookeeping Practice Set Answer (Blank Form)AcissejNo ratings yet

- Double Entry Bookkeeping Joan MartinDocument13 pagesDouble Entry Bookkeeping Joan MartinTyra RobinsonNo ratings yet

- Bookkeeping TemplatesDocument51 pagesBookkeeping TemplatesKyle100% (2)

- Date Account Account Debit CreditDocument11 pagesDate Account Account Debit CreditClaudine bea NavarreteNo ratings yet

- Fundamentals of Bookkeeping: Ucpb Savings Bank Operations DivisionDocument71 pagesFundamentals of Bookkeeping: Ucpb Savings Bank Operations DivisionJames ToNo ratings yet

- Bookkeeping NC Iii Coverage and Reviewer: Disbursements JournalDocument3 pagesBookkeeping NC Iii Coverage and Reviewer: Disbursements JournalHermin Austria0% (1)

- BookkeepingDocument92 pagesBookkeepingJhinete Rizada Estoy100% (1)

- Basic AccountingDocument12 pagesBasic AccountingDiana Grace SierraNo ratings yet

- TR Bookkeeping NC IIIDocument71 pagesTR Bookkeeping NC IIIMichael V. Magallano100% (1)

- Basic BookkeepingDocument61 pagesBasic BookkeepingJayson Reyes50% (4)

- Bookkeeping NC IiiDocument4 pagesBookkeeping NC IiiKristine Marie TrillesNo ratings yet

- Bookkeeping NC IIIDocument72 pagesBookkeeping NC IIImary ann dieronNo ratings yet

- Accounting For Non-AccountantsDocument44 pagesAccounting For Non-AccountantsKittenNo ratings yet

- Introduction To Bookkeeping and AccountingDocument194 pagesIntroduction To Bookkeeping and AccountingdhenNo ratings yet

- Bookkeeping NC Level 3Document76 pagesBookkeeping NC Level 3Jennica MontanesNo ratings yet

- QuickBooks For Agricultural Financial RecordsDocument89 pagesQuickBooks For Agricultural Financial RecordsAbdalla Nizar Al-busaidy100% (2)

- Bookkeeping Engagement LetterDocument11 pagesBookkeeping Engagement LetterFortune William LedesmaNo ratings yet

- CBC Bookkeeping JournalizeDocument9 pagesCBC Bookkeeping JournalizeKenneth Catalan SaelNo ratings yet

- Chart of Accounts ExplanationDocument9 pagesChart of Accounts Explanationellapot89No ratings yet

- ACCOUNTINGDocument31 pagesACCOUNTINGCHARAK RAYNo ratings yet

- QuickBooks For BeginnersDocument3 pagesQuickBooks For BeginnersZain U Ddin0% (1)

- Book of Accounts Part 1. JournalDocument12 pagesBook of Accounts Part 1. JournalJace AbeNo ratings yet

- Posting To LedgerDocument34 pagesPosting To LedgerBridgett Florence CaldaNo ratings yet

- QuickBooks Training &global Certification - IndiaDocument10 pagesQuickBooks Training &global Certification - IndiaswayamNo ratings yet

- QuickBooks 2014 The Missing ManualDocument1,129 pagesQuickBooks 2014 The Missing ManualCesar Mendoza100% (4)

- Inventory Report 2021-FinalDocument19 pagesInventory Report 2021-FinalEngr Mohammad Al-AminNo ratings yet

- Reasons of Keeping Business RecordsDocument50 pagesReasons of Keeping Business RecordsJhianne EstacojaNo ratings yet

- Basic Accounting EquationDocument49 pagesBasic Accounting Equationwhyme_b100% (1)

- QuickBooks Online for Beginners: The Step by Step Guide to Bookkeeping and Financial Accounting for Small Businesses and FreelancersFrom EverandQuickBooks Online for Beginners: The Step by Step Guide to Bookkeeping and Financial Accounting for Small Businesses and FreelancersNo ratings yet

- Your Amazing Itty Bitty® Book of QuickBooks® Best PracticesFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® Best PracticesNo ratings yet

- How to Learn Intuit Quickbooks Quickly!: Intuit Quickbooks Mastery: Quick and Easy LearningFrom EverandHow to Learn Intuit Quickbooks Quickly!: Intuit Quickbooks Mastery: Quick and Easy LearningNo ratings yet

- F AccountingDocument43 pagesF Accountingvcpc2008No ratings yet

- Tax Alert (December 2020)Document10 pagesTax Alert (December 2020)Rheneir MoraNo ratings yet

- Cit U Bsma ProspectusDocument4 pagesCit U Bsma ProspectusRheneir MoraNo ratings yet

- Form45 3Document2 pagesForm45 3Rheneir MoraNo ratings yet

- RDO No. 47 - East MakatiDocument83 pagesRDO No. 47 - East MakatiRheneir MoraNo ratings yet

- Cit U Bsa ProspectusDocument4 pagesCit U Bsa ProspectusRheneir MoraNo ratings yet

- 49 Insights June 2022V2Document24 pages49 Insights June 2022V2Rheneir MoraNo ratings yet

- Tax Alert September 2020 Final v2Document6 pagesTax Alert September 2020 Final v2Rheneir MoraNo ratings yet

- October 2020 Tax AlertDocument5 pagesOctober 2020 Tax AlertRheneir MoraNo ratings yet

- Tax Alert Special Issue March 31, 2020 (Final)Document15 pagesTax Alert Special Issue March 31, 2020 (Final)Rheneir MoraNo ratings yet

- Tax Alert (June 2020)Document7 pagesTax Alert (June 2020)Rheneir MoraNo ratings yet

- Obligations and Contracts: Atty. Rheneir P. Mora, CPADocument55 pagesObligations and Contracts: Atty. Rheneir P. Mora, CPARheneir MoraNo ratings yet

- Tax Alert Regular Issue (March 2020)Document19 pagesTax Alert Regular Issue (March 2020)Rheneir MoraNo ratings yet

- Tax Alert (April 2020) FinalDocument30 pagesTax Alert (April 2020) FinalRheneir MoraNo ratings yet

- 2020soar 2019 Ifiar Survey ReportDocument28 pages2020soar 2019 Ifiar Survey ReportRheneir MoraNo ratings yet

- KAMMP Seminar - AccountingDocument37 pagesKAMMP Seminar - AccountingRheneir MoraNo ratings yet

- KAMMP SeminarDocument2 pagesKAMMP SeminarRheneir MoraNo ratings yet

- Summer Internship Project ReportDocument10 pagesSummer Internship Project ReportPraveen Sehgal0% (1)

- Assignment 1Document7 pagesAssignment 1Dat DoanNo ratings yet

- Iti ResumeDocument2 pagesIti Resumebdp2n8d6hjNo ratings yet

- Bus. Comb. Handout 2Document2 pagesBus. Comb. Handout 2Eriane Mae C. SamaneNo ratings yet

- Producer SurplusDocument1 pageProducer SurpluspenelopegerhardNo ratings yet

- Local Church Audit ReportDocument5 pagesLocal Church Audit ReportJennie Hastings100% (2)

- The Process of Strategic Brand Management Basically Involves 4 StepsDocument17 pagesThe Process of Strategic Brand Management Basically Involves 4 StepsBoopathi MaharajaNo ratings yet

- Shangai Tang Case StudyDocument2 pagesShangai Tang Case StudyManel CanavarroNo ratings yet

- Business Plan - Fajardo, AlonaDocument11 pagesBusiness Plan - Fajardo, AlonaAlona FajardoNo ratings yet

- International Trade in The Presence of Product Differentiation, Economies of Scale and Monopolistic Competition A Chamberlin-Heckscher-Ohlin ApproachDocument36 pagesInternational Trade in The Presence of Product Differentiation, Economies of Scale and Monopolistic Competition A Chamberlin-Heckscher-Ohlin ApproachDavid CernaNo ratings yet

- Nasiya Electric Projected BS & P&L Ac 2024Document5 pagesNasiya Electric Projected BS & P&L Ac 2024anupNo ratings yet

- Lesson 2.2 - Demand and Supply in Relation To The Prices of Basic Commodities (Ignacio, Mary - Ledda)Document26 pagesLesson 2.2 - Demand and Supply in Relation To The Prices of Basic Commodities (Ignacio, Mary - Ledda)Andrea Nicole Hernandez100% (3)

- Exercise ExcelDocument7 pagesExercise Excelhelennguyen242004No ratings yet

- 8 Filters of Game DesignDocument12 pages8 Filters of Game DesignpnishkaNo ratings yet

- Igcse Accounting 2-2Document43 pagesIgcse Accounting 2-2Yenny Tiga88% (8)

- Mcqs Based & Very Short Answer Type QuestionsDocument5 pagesMcqs Based & Very Short Answer Type QuestionsjashanjeetNo ratings yet

- Chapter 2 - Approaches of International Business & TradeDocument18 pagesChapter 2 - Approaches of International Business & TradeArmie LandritoNo ratings yet

- Oracle Managed Cloud Services Global Price ListDocument18 pagesOracle Managed Cloud Services Global Price ListnikhilNo ratings yet

- Managing The Marketing Function SHERWIN ESPIRITUDocument35 pagesManaging The Marketing Function SHERWIN ESPIRITUangelo95% (20)

- B2B E-Commerce: Selling and Buying in Private E-MarketsDocument54 pagesB2B E-Commerce: Selling and Buying in Private E-MarketsKrisel IbanezNo ratings yet

- San Mateo Municipal College: General Luna ST., Guitnang Bayan I, San Mateo, Rizal Tel. No. (02) 997-9070Document10 pagesSan Mateo Municipal College: General Luna ST., Guitnang Bayan I, San Mateo, Rizal Tel. No. (02) 997-9070Chan YeolNo ratings yet

- Standard Costing Quiz 2Document2 pagesStandard Costing Quiz 2Shafni DulnuanNo ratings yet

- Auditing 2019 P S CH 8Document16 pagesAuditing 2019 P S CH 8barakat801No ratings yet

- Meena Bazar Internship Report PT 2Document16 pagesMeena Bazar Internship Report PT 2jasia.samihaNo ratings yet

- Theme 1 A New Geo-EconomyDocument47 pagesTheme 1 A New Geo-Economyreginaamondi133No ratings yet

- Accounting Basics 1 QuizDocument6 pagesAccounting Basics 1 QuizRegine Pahigo Hillado100% (1)

- Unit - 2 Information Technology and BusinessDocument22 pagesUnit - 2 Information Technology and Businessayushrauniyargupta100% (1)