Chap005 (A)

Chap005 (A)

Download as ppt, pdf, or txt

You might also like

- Fastern Case Notes - Docx - Fasten Challenging Uber and Lyft..Document18 pagesFastern Case Notes - Docx - Fasten Challenging Uber and Lyft..Salman Azeem0% (1)

- Simple Numbers, Straight Talk, Big Profits! - 4 Keys To Unlock Your Business Potential (PDFDrive)Document159 pagesSimple Numbers, Straight Talk, Big Profits! - 4 Keys To Unlock Your Business Potential (PDFDrive)SameedNo ratings yet

- 11.1. Practice Exercise - Cumberland Inc - BlankDocument5 pages11.1. Practice Exercise - Cumberland Inc - Blank155- Salsabila GadingNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- CH 5 - AdjustmentsDocument24 pagesCH 5 - Adjustmentsmuhamad elmiNo ratings yet

- Gabriele G S Suder - International Business Under Adversity - A Role in Corporate Responsibility, Conflict Prevention and Peace-Edward ElgDocument214 pagesGabriele G S Suder - International Business Under Adversity - A Role in Corporate Responsibility, Conflict Prevention and Peace-Edward ElgAlberto QpertNo ratings yet

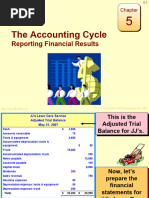

- The Accounting Cycle:: Reporting Financial ResultsDocument22 pagesThe Accounting Cycle:: Reporting Financial Resultsali goharNo ratings yet

- Chapter 05 - (The Accounting Cycle. Reporting Financial Results)Document22 pagesChapter 05 - (The Accounting Cycle. Reporting Financial Results)Hafiz SherazNo ratings yet

- The Accounting Cycle: Reporting Financial Results: Mcgraw-Hill/IrwinDocument23 pagesThe Accounting Cycle: Reporting Financial Results: Mcgraw-Hill/IrwinDuae ZahraNo ratings yet

- The Accounting Cycle: Reporting Financial Results: Mcgraw-Hill/IrwinDocument28 pagesThe Accounting Cycle: Reporting Financial Results: Mcgraw-Hill/Irwinazee inmixNo ratings yet

- Chapter 5Document25 pagesChapter 5wasilqureshi2004No ratings yet

- Chap 05Document25 pagesChap 05Joseph IbrahimNo ratings yet

- Chapter05 Closing Entries 22022023 034830pmDocument19 pagesChapter05 Closing Entries 22022023 034830pmsualehfaisal50No ratings yet

- Ch-10 Accountancy Class XI Part-2Document65 pagesCh-10 Accountancy Class XI Part-2rakesh_nandaniNo ratings yet

- Whbc05 FinalDocument33 pagesWhbc05 Finalfa22-bcs-095No ratings yet

- Whbc05 FinalDocument33 pagesWhbc05 Finalmunnicod64No ratings yet

- Fma 03 (Iii)Document23 pagesFma 03 (Iii)eyobirhanu1992No ratings yet

- Chapter 03 - (The Accounting Cycle. Capturing Economic Events)Document43 pagesChapter 03 - (The Accounting Cycle. Capturing Economic Events)Hafiz Sheraz100% (1)

- ACC501_ Assignment No.1Document4 pagesACC501_ Assignment No.1ahsan sajjadNo ratings yet

- The Accounting Cycle:: Capturing Economic EventsDocument43 pagesThe Accounting Cycle:: Capturing Economic Eventsali goharNo ratings yet

- The Accounting Cycle: Capturing Economic Events: Mcgraw-Hill/IrwinDocument45 pagesThe Accounting Cycle: Capturing Economic Events: Mcgraw-Hill/IrwinSobia NasreenNo ratings yet

- Chap005 2022Document20 pagesChap005 2022mustafaNo ratings yet

- Spring 2024 - ACC501 - 1Document3 pagesSpring 2024 - ACC501 - 1freebutterfly121No ratings yet

- Financial Ratios-Hamna RizwanDocument5 pagesFinancial Ratios-Hamna RizwanHamna RizwanNo ratings yet

- Financial Statement AnalysisDocument82 pagesFinancial Statement AnalysisHeisen LukeNo ratings yet

- Rinconada - ProjectDocument29 pagesRinconada - ProjectRINCONADA ReynalynNo ratings yet

- Completing The Accounting CycleDocument27 pagesCompleting The Accounting Cycleadillawa100% (1)

- Basic Accounting IDocument24 pagesBasic Accounting IAlpha HoNo ratings yet

- Accounting and Finance: Fundamentals of Corporate FinanceDocument21 pagesAccounting and Finance: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- 6 Incomplete RecordsDocument16 pages6 Incomplete Recordssana.ibrahimNo ratings yet

- The Role of Working Capital: SalesDocument25 pagesThe Role of Working Capital: SalesMT NoowinNo ratings yet

- Chap 002Document17 pagesChap 002soso900No ratings yet

- Lec 4Document42 pagesLec 4Nidus PhrykeNo ratings yet

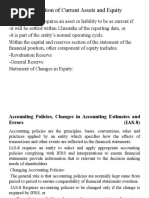

- Recognition of Current Assets and EquityDocument8 pagesRecognition of Current Assets and EquityMd. N UraminNo ratings yet

- Chap 002 NotesDocument43 pagesChap 002 NotessamiullahaslamNo ratings yet

- Short-Term Financial Planning: Fundamentals of Corporate FinanceDocument26 pagesShort-Term Financial Planning: Fundamentals of Corporate FinanceruriNo ratings yet

- Accounting Principles & Practices An Overview DefinitionDocument23 pagesAccounting Principles & Practices An Overview DefinitionAmanuel TesfayeNo ratings yet

- 6 Incomplete RecordsDocument16 pages6 Incomplete Recordssana.ibrahimNo ratings yet

- Adjusting EntriesDocument24 pagesAdjusting EntriesALLIA LOPEZNo ratings yet

- Accounts TrainingDocument16 pagesAccounts TraininghitnandawaniNo ratings yet

- 6 Incomplete RecordsDocument17 pages6 Incomplete Recordssana.ibrahimNo ratings yet

- Financial ReportingDocument36 pagesFinancial ReportingM RNo ratings yet

- 1 - Acc 311 Exam II Spring 2015Document9 pages1 - Acc 311 Exam II Spring 2015MUHAMMAD AZAMNo ratings yet

- Basic Financial StatementsDocument38 pagesBasic Financial Statementshimani rathoreNo ratings yet

- Chapter 2Document49 pagesChapter 2haiderasim1212No ratings yet

- Axia College Material: Journalizing, Posting, and Preparing A Trial BalanceDocument12 pagesAxia College Material: Journalizing, Posting, and Preparing A Trial BalanceyaneemaNo ratings yet

- Chapter 04 - (The Accounting Cycle. Accruals and Deferrals)Document41 pagesChapter 04 - (The Accounting Cycle. Accruals and Deferrals)Hafiz SherazNo ratings yet

- BV 123Document12 pagesBV 123Bala VigneshNo ratings yet

- Measuring Cash Flows & Financial Planning: Dr. C. Bulent AybarDocument47 pagesMeasuring Cash Flows & Financial Planning: Dr. C. Bulent AybarKenneth PimentelNo ratings yet

- Chapter 1-4Document20 pagesChapter 1-4BookDownNo ratings yet

- CH 2 - Incomplete Records & Non Profit OrganisationDocument56 pagesCH 2 - Incomplete Records & Non Profit OrganisationFaris IzzatNo ratings yet

- Mcgraw-Hill/Irwin Corporate Finance, 7/E: © 2005 The Mcgraw-Hill Companies, Inc. All Rights ReservedDocument26 pagesMcgraw-Hill/Irwin Corporate Finance, 7/E: © 2005 The Mcgraw-Hill Companies, Inc. All Rights ReservedMohammad Ilham FawwazNo ratings yet

- FABM 2 (Module 5)Document12 pagesFABM 2 (Module 5)Reyman Andrade LosanoNo ratings yet

- Financial and Managerial Accounting PDFDocument1 pageFinancial and Managerial Accounting PDFcons theNo ratings yet

- FA I Chap2 & NotesDocument42 pagesFA I Chap2 & NotesMuneeb AliNo ratings yet

- Basic Financial Statements: Mcgraw-Hill/IrwinDocument43 pagesBasic Financial Statements: Mcgraw-Hill/IrwinDuae ZahraNo ratings yet

- Basic Financial Statements: Stofa, MBM 16 Batch, BIBMDocument43 pagesBasic Financial Statements: Stofa, MBM 16 Batch, BIBMMorshed Chowdhury ZishanNo ratings yet

- Topic: Financial Management: Juan CerónDocument25 pagesTopic: Financial Management: Juan CerónJUAN ANTONIO CERON CRUZNo ratings yet

- Financial Statements and Cash Flow: Solutions To Questions and ProblemsDocument10 pagesFinancial Statements and Cash Flow: Solutions To Questions and ProblemsTing-An KuoNo ratings yet

- Unit 4Document33 pagesUnit 4b21ai008No ratings yet

- CH 2Document64 pagesCH 2husnain murtazaNo ratings yet

- Block 12ce PPT Ch03 FinalDocument33 pagesBlock 12ce PPT Ch03 FinalnimugiritshaNo ratings yet

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersNo ratings yet

- J Management Studies - 2018 - Ozalp - Disruption in Platform Based EcosystemsDocument39 pagesJ Management Studies - 2018 - Ozalp - Disruption in Platform Based EcosystemsShujat AliNo ratings yet

- Financial Model - Customize ItDocument46 pagesFinancial Model - Customize ItShujat AliNo ratings yet

- TERM PAPER - Marketing ManagementDocument18 pagesTERM PAPER - Marketing ManagementShujat AliNo ratings yet

- Electrical Engineering Subject Test - 1Document1 pageElectrical Engineering Subject Test - 1Shujat AliNo ratings yet

- Revenue Models - FutureDocument3 pagesRevenue Models - FutureShujat AliNo ratings yet

- Art Infusion: Ideal Conditions For STEAMDocument7 pagesArt Infusion: Ideal Conditions For STEAMShujat AliNo ratings yet

- Digital Mindsets Recognizing and Leveraging Individual Beliefs For Digital TransformationDocument20 pagesDigital Mindsets Recognizing and Leveraging Individual Beliefs For Digital TransformationShujat AliNo ratings yet

- Agility As The Discovery of Slowness: ManagementDocument24 pagesAgility As The Discovery of Slowness: ManagementShujat AliNo ratings yet

- UntitledDocument17 pagesUntitledShujat AliNo ratings yet

- Lean CanvasDocument2 pagesLean CanvasShujat AliNo ratings yet

- UntitledDocument3 pagesUntitledShujat AliNo ratings yet

- Categories of Entrepreneurial OpportunityDocument7 pagesCategories of Entrepreneurial OpportunityShujat AliNo ratings yet

- Shujat Ali Khan - Assignment # 2Document7 pagesShujat Ali Khan - Assignment # 2Shujat AliNo ratings yet

- Paper 17Document15 pagesPaper 17Shujat AliNo ratings yet

- Leading Team Building, Managing Group Dynamics and DiversityDocument46 pagesLeading Team Building, Managing Group Dynamics and DiversityShujat AliNo ratings yet

- FICS PresentationDocument13 pagesFICS PresentationShujat AliNo ratings yet

- Schumpeterian Entrepreneurship in EuropeDocument32 pagesSchumpeterian Entrepreneurship in EuropeShujat AliNo ratings yet

- Week 2 Leadership CompetenciesDocument20 pagesWeek 2 Leadership CompetenciesShujat AliNo ratings yet

- Assignment # 1 - PPIDocument8 pagesAssignment # 1 - PPIShujat AliNo ratings yet

- Virtual Reality in Pakistan's Gaming IndustryDocument4 pagesVirtual Reality in Pakistan's Gaming IndustryShujat AliNo ratings yet

- Black and Green Gradient Virtual Reality PresentationDocument10 pagesBlack and Green Gradient Virtual Reality PresentationShujat AliNo ratings yet

- Assignment 1 - Operations ManagementDocument2 pagesAssignment 1 - Operations ManagementShujat AliNo ratings yet

- Joining Instructions and Schedule of NBS PGDocument6 pagesJoining Instructions and Schedule of NBS PGShujat AliNo ratings yet

- Reflection - Seminar 5Document4 pagesReflection - Seminar 5Shujat AliNo ratings yet

- MBBS Online Paper - NUMSDocument8 pagesMBBS Online Paper - NUMSShujat AliNo ratings yet

- Virtual Reality in Pakistan's Gaming IndustryDocument5 pagesVirtual Reality in Pakistan's Gaming IndustryShujat AliNo ratings yet

- Kodak Misses Its Moment PDFDocument15 pagesKodak Misses Its Moment PDFShujat AliNo ratings yet

- Ivey Publishing Submission GuidelinesDocument2 pagesIvey Publishing Submission GuidelinesShujat AliNo ratings yet

- Fedore Cooperative Effective Conflict Resolution and Decision MakingDocument12 pagesFedore Cooperative Effective Conflict Resolution and Decision MakingShujat AliNo ratings yet

- Evaluation of Architectures For Mobile RoboticsDocument17 pagesEvaluation of Architectures For Mobile RoboticsShujat AliNo ratings yet

- Et Ref TestpatternsDocument338 pagesEt Ref Testpatternspravallika vysyarajuNo ratings yet

- Instruction: Show Your Solution. No Solution Incorrect AnswerDocument1 pageInstruction: Show Your Solution. No Solution Incorrect AnswerRian ChiseiNo ratings yet

- The State of Fashion: TechnologyDocument33 pagesThe State of Fashion: TechnologyHuang MaxNo ratings yet

- XA1002 Catalogo Paderno 2022 WEB VLR 892103Document580 pagesXA1002 Catalogo Paderno 2022 WEB VLR 892103geezeer.manalansanNo ratings yet

- HDPE Plastic PIPE FUSION WELDING WORK METHOD STATEMENT 01 PDFDocument11 pagesHDPE Plastic PIPE FUSION WELDING WORK METHOD STATEMENT 01 PDFSuryakant Suraj100% (2)

- Chapter 1 - Partnership Formation PDFDocument33 pagesChapter 1 - Partnership Formation PDFAldrin ZolinaNo ratings yet

- Appendix C Architectural Exterior Finishes RequirmentsDocument2 pagesAppendix C Architectural Exterior Finishes RequirmentsEr Bishwonath ShahNo ratings yet

- Employee HandbookDocument19 pagesEmployee HandbookBabu ShanojNo ratings yet

- AMIT 135 - Lesson 5 Crushing - Mining Mill Operator TrainingDocument27 pagesAMIT 135 - Lesson 5 Crushing - Mining Mill Operator TrainingFery CahyonoNo ratings yet

- The Advantages and Disadvantages of TelecommutingDocument9 pagesThe Advantages and Disadvantages of Telecommuting王诗笛No ratings yet

- Terms and Conditions CAIEDocument3 pagesTerms and Conditions CAIEMariam BurhanNo ratings yet

- Arnold v. Willets and Patterson, LTD., 44 Phil. 634 (1923)Document10 pagesArnold v. Willets and Patterson, LTD., 44 Phil. 634 (1923)inno KalNo ratings yet

- Tendernotice_1 - 2024-10-28T085655.700Document7 pagesTendernotice_1 - 2024-10-28T085655.700Sabah KohliNo ratings yet

- Food Traceability PPT 01Document25 pagesFood Traceability PPT 01Muddasir Ahmad Akhoon100% (4)

- Ruth Getachew MBA, Week-End 2020Document69 pagesRuth Getachew MBA, Week-End 2020Kifle GizawNo ratings yet

- Master Thesis Topics Corporate FinanceDocument7 pagesMaster Thesis Topics Corporate Financemarialackarlington100% (2)

- UGO Impact of Corporate Social Responsibility On Customer Loyalty and Satisfaction in The UK SupermarketDocument58 pagesUGO Impact of Corporate Social Responsibility On Customer Loyalty and Satisfaction in The UK SupermarketAimal ShahrukhNo ratings yet

- INVOICEDocument1 pageINVOICENamario EtienneNo ratings yet

- Past SSCDocument62 pagesPast SSCtortilearningwebcoddingNo ratings yet

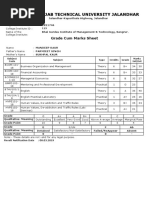

- I.K.Gujral Punjab Technical University Jalandhar: Grade Cum Marks SheetDocument1 pageI.K.Gujral Punjab Technical University Jalandhar: Grade Cum Marks SheetMandeep KaurNo ratings yet

- Transaction Processing: I. The Data Processing CycleDocument6 pagesTransaction Processing: I. The Data Processing Cyclejudel ArielNo ratings yet

- 7-1: Price, Growth & Return: SolutionDocument5 pages7-1: Price, Growth & Return: SolutionPuneet MeenaNo ratings yet

- Comilla University Department of Management StudiesDocument2 pagesComilla University Department of Management StudiesMd. Siddikur RahmanNo ratings yet

- Us Work From Home JobsDocument4 pagesUs Work From Home JobsNazakat AliNo ratings yet

- PGT-Economics+final Manual 81-165Document85 pagesPGT-Economics+final Manual 81-165Amir HussainNo ratings yet

- Chapter 2Document9 pagesChapter 2Mary Joy AlbandiaNo ratings yet

- Project UddyamDocument5 pagesProject Uddyamrutvi.khatri.20No ratings yet