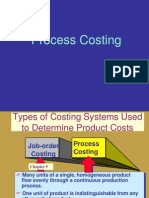

Process Costing

Process Costing

Download as ppt, pdf, or txt

You might also like

- Click File - Download - The Corporate Finance Cheat Sheet - Oana Labes, MBA, CPADocument9 pagesClick File - Download - The Corporate Finance Cheat Sheet - Oana Labes, MBA, CPAMessias MorettoNo ratings yet

- Process Costing ProblemsDocument9 pagesProcess Costing ProblemsAries Bautista67% (3)

- Process Costing Problems 1Document9 pagesProcess Costing Problems 1RoMaNo ratings yet

- Tutorial - 1 - 2 - (06.10.2022, 13.10.22) TOPIC: Basic Cost Terms and Concepts, Cost Classification Ex. 1Document3 pagesTutorial - 1 - 2 - (06.10.2022, 13.10.22) TOPIC: Basic Cost Terms and Concepts, Cost Classification Ex. 1Tomas SanzNo ratings yet

- Chapter 4-Exercises-Managerial AccountingDocument3 pagesChapter 4-Exercises-Managerial AccountingSheila Mae LiraNo ratings yet

- Test-Bank-2 CostDocument8 pagesTest-Bank-2 CostRaneNo ratings yet

- Chapter 4 Homework QuestionsDocument4 pagesChapter 4 Homework Questionsanon_665127674100% (4)

- Exercise 4-2 Group WorkDocument6 pagesExercise 4-2 Group Worksesegar_nailofar100% (4)

- 120-Practice-Material Process StandardVariances ABCDocument36 pages120-Practice-Material Process StandardVariances ABCNovie Mea Balbes50% (2)

- Chapter 6 Quiz and AssignmentDocument25 pagesChapter 6 Quiz and AssignmentSaeym SegoviaNo ratings yet

- Practical Earned Value Analysis: 25 Project Indicators from 5 MeasurementsFrom EverandPractical Earned Value Analysis: 25 Project Indicators from 5 MeasurementsNo ratings yet

- Chapter 04 WorksheetDocument13 pagesChapter 04 WorksheetqpelinsubcNo ratings yet

- Sesi 9 Process CostDocument76 pagesSesi 9 Process CostAnggrainiNo ratings yet

- CH 06 Process CostingDocument67 pagesCH 06 Process CostingShannon Bánañas100% (2)

- 6-35 Seacrest Company - 2Document14 pages6-35 Seacrest Company - 2Anji GoyNo ratings yet

- Universidad Interamericana de Puerto Rico Recinto de San Germán Departamento de Ciencias EmpresarialesDocument5 pagesUniversidad Interamericana de Puerto Rico Recinto de San Germán Departamento de Ciencias EmpresarialesAqib LatifNo ratings yet

- Chapter 4Document26 pagesChapter 4ReineNo ratings yet

- MeklitDocument7 pagesMeklitdhugaaman7No ratings yet

- CostaccDocument4 pagesCostaccjaringanlimagNo ratings yet

- MANACC Class Handout - Process Costing-1Document6 pagesMANACC Class Handout - Process Costing-1Ritwik MahajanNo ratings yet

- 6e ch06Document53 pages6e ch06Cholifah Husti LailaNo ratings yet

- Assignment Question AccDocument5 pagesAssignment Question AccruqayyahqaisaraNo ratings yet

- Compute The Equivalent Units of ProductionDocument1 pageCompute The Equivalent Units of Productionsb73_817No ratings yet

- Mymie B. Maandig MBA-1 Dr. Marco Ilano Problem 4-13A RequiredDocument9 pagesMymie B. Maandig MBA-1 Dr. Marco Ilano Problem 4-13A RequiredMymie MaandigNo ratings yet

- Process CostingDocument16 pagesProcess CostingDiane PascualNo ratings yet

- Acc 2Document5 pagesAcc 2nma.work173No ratings yet

- Week 2 - BUS 5431 - HomeworkDocument4 pagesWeek 2 - BUS 5431 - HomeworkSue Ming Fei100% (1)

- 8- Cost Accounting (1)- Chapter (2) - Process Costing- Part 3Document6 pages8- Cost Accounting (1)- Chapter (2) - Process Costing- Part 3com01156499073No ratings yet

- Midterm No. One Review: The Equivalent Units of Production For Conversion Costs WereDocument5 pagesMidterm No. One Review: The Equivalent Units of Production For Conversion Costs WereEric AgudeloNo ratings yet

- Acct1 8 (1Document9 pagesAcct1 8 (1Thu V A NguyenNo ratings yet

- Cost Accounting AssignmentDocument5 pagesCost Accounting AssignmentAli PuriNo ratings yet

- Cost Accounting Quiz 2 PDFDocument10 pagesCost Accounting Quiz 2 PDFangel hello-helloNo ratings yet

- Lec3 ProcesscostingDocument25 pagesLec3 Processcostinghello1928No ratings yet

- Process Costing - Summer 2012Document51 pagesProcess Costing - Summer 2012isha_sNo ratings yet

- Product - Midterm ACC C203-205A: SolutionDocument5 pagesProduct - Midterm ACC C203-205A: SolutionMarkJoven BergantinNo ratings yet

- Chapter 4 Solutions-1Document7 pagesChapter 4 Solutions-1mackkshellNo ratings yet

- Seminar 4 Tutor - ACC203Document38 pagesSeminar 4 Tutor - ACC203Regina KwokNo ratings yet

- Exercise Managerial Accounting 1 Chapter 4Document13 pagesExercise Managerial Accounting 1 Chapter 434Hoàng ThơNo ratings yet

- Management Accounting Set 3Document11 pagesManagement Accounting Set 3Julia ŚwierczyńskaNo ratings yet

- Chapter 6 Practice QuestionsDocument9 pagesChapter 6 Practice QuestionsAbdul Wajid Nazeer CheemaNo ratings yet

- Solutions MA Chapter 3 Book Version (AutoRecovered)Document3 pagesSolutions MA Chapter 3 Book Version (AutoRecovered)achhpilia.muskan.psNo ratings yet

- HorngrenIMA14eSM ch14Document40 pagesHorngrenIMA14eSM ch14Piyal Hossain100% (1)

- True FalseDocument3 pagesTrue FalseCarlo Paras100% (1)

- Cornerstone Exercise 6Document8 pagesCornerstone Exercise 6NiropamNo ratings yet

- Baking DepartmentDocument6 pagesBaking DepartmentkmarisseeNo ratings yet

- Chapter 6 - Process CostingDocument53 pagesChapter 6 - Process CostingHARYATI SETYORININo ratings yet

- GNB 12e Practice Exam - Chapter 4Document4 pagesGNB 12e Practice Exam - Chapter 4Holli Boyd-WhiteNo ratings yet

- Chapter 3 ExamplesDocument2 pagesChapter 3 ExamplesAli Gökay BozokNo ratings yet

- Analisis Biaya: Semester Gasal TA 2016 - 2017 Process CostingDocument48 pagesAnalisis Biaya: Semester Gasal TA 2016 - 2017 Process CostingMaulana HasanNo ratings yet

- ACC60181H619 Managerial AccountingDocument9 pagesACC60181H619 Managerial AccountingaksNo ratings yet

- Willow Corp Uses A Process Costing SystemDocument4 pagesWillow Corp Uses A Process Costing SystemKarlyta Garcia GodoyNo ratings yet

- Cost of Production ReportDocument10 pagesCost of Production ReportNo NotreallyNo ratings yet

- Managerial Accounting Final ExamDocument14 pagesManagerial Accounting Final ExamatifNo ratings yet

- QUIZZERDocument4 pagesQUIZZERchowchow123No ratings yet

- Short Problem#1: No Lost Units, Pure EUPDocument3 pagesShort Problem#1: No Lost Units, Pure EUPDerick FigueroaNo ratings yet

- Acg 4361 Chapter 17 Study Probes SolutionDocument18 pagesAcg 4361 Chapter 17 Study Probes SolutionPatDabzNo ratings yet

- Process Costing Tutorial SheetDocument3 pagesProcess Costing Tutorial Sheets_camika7534No ratings yet

- RCA Solutions Mod3 PDFDocument13 pagesRCA Solutions Mod3 PDFdiane camansagNo ratings yet

- Seatwork Process Costing ProbDocument6 pagesSeatwork Process Costing ProbAllyzzaBuhainNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Developing A Strategy 17 TH February 2015Document27 pagesDeveloping A Strategy 17 TH February 2015arshad mNo ratings yet

- Direct Material Price VarianceDocument2 pagesDirect Material Price Variancearshad mNo ratings yet

- Varince AnalysisDocument79 pagesVarince Analysisarshad mNo ratings yet

- Lesson10 enDocument32 pagesLesson10 enarshad mNo ratings yet

- The Corporate Form of Business Organization: Accounting For Stockholders' EquityDocument20 pagesThe Corporate Form of Business Organization: Accounting For Stockholders' Equityarshad mNo ratings yet

- Chapter 1 - Strategic Cost Management: MidtermDocument19 pagesChapter 1 - Strategic Cost Management: MidtermAndrea Nicole De LeonNo ratings yet

- A Survey On E-CommerceDocument16 pagesA Survey On E-CommerceSupriya RamNo ratings yet

- Rachid El Hidoudi Resume EngDocument2 pagesRachid El Hidoudi Resume Engrachid.elhidoudi1No ratings yet

- Group 2 Cost Volume Profit AnalysisDocument43 pagesGroup 2 Cost Volume Profit AnalysisTricia Marie TumandaNo ratings yet

- Luxury Brand Goods Repurchase Intentions Brand-Self CongruityDocument17 pagesLuxury Brand Goods Repurchase Intentions Brand-Self CongruityMahasiswa BiasaNo ratings yet

- 4 IMM-Logistics Records and ReportsDocument73 pages4 IMM-Logistics Records and ReportsAgustin OrioqueNo ratings yet

- Steps To Business Growth Mastery EbookDocument13 pagesSteps To Business Growth Mastery EbookNarendarraj BNo ratings yet

- Module 10Document7 pagesModule 10isabel payupayNo ratings yet

- ACC101-Mid-Term Test - ACC101-Mid-Term TestDocument14 pagesACC101-Mid-Term Test - ACC101-Mid-Term Testtuyennt.ce191205No ratings yet

- Laura and John Arnold Foundation 2022 Tax Forms, Obtained by Gabe KaminskyDocument144 pagesLaura and John Arnold Foundation 2022 Tax Forms, Obtained by Gabe KaminskyGabe KaminskyNo ratings yet

- Blue Book Summary PresentationDocument13 pagesBlue Book Summary Presentationx-starNo ratings yet

- Business Studies Sample Papers 4 With SolutionDocument10 pagesBusiness Studies Sample Papers 4 With SolutionRiya JainNo ratings yet

- 25226-Article Text-83873-1-2-20230627Document44 pages25226-Article Text-83873-1-2-20230627ainnafshNo ratings yet

- Statistic - Id1343785 - Most Well Known Outdoor Fashion Brands in The United States 2023Document8 pagesStatistic - Id1343785 - Most Well Known Outdoor Fashion Brands in The United States 2023Dana MichelleNo ratings yet

- Point and Figure Charts PDFDocument5 pagesPoint and Figure Charts PDFCarlos Daniel Rodrigo CNo ratings yet

- Topic 3 - Stock ValuationDocument50 pagesTopic 3 - Stock ValuationBaby KhorNo ratings yet

- Agamata Chapter 6Document18 pagesAgamata Chapter 6Abigail Faye Roxas100% (1)

- Rewards of Going Into Business or EntrepreneurshipDocument22 pagesRewards of Going Into Business or Entrepreneurshipjoshuabarrera1999No ratings yet

- HO Model NotesDocument7 pagesHO Model NotesecsNo ratings yet

- SEC Subpoena MGT Capital September 2016Document14 pagesSEC Subpoena MGT Capital September 2016Teri Buhl100% (1)

- Administration PlanDocument11 pagesAdministration PlanAneesa JalilNo ratings yet

- ECONOMICS1Document3 pagesECONOMICS1MASINDENo ratings yet

- Audit UNIT 1Document9 pagesAudit UNIT 1Nigussie BerhanuNo ratings yet

- BTap-TCDN 2Document22 pagesBTap-TCDN 2baonguyen.31211022084No ratings yet

- Sales Promotion ToolsDocument22 pagesSales Promotion Toolstony_njNo ratings yet

- Workbook CH 6Document72 pagesWorkbook CH 6grayNo ratings yet

- Chapter 2 Dolce PatataDocument5 pagesChapter 2 Dolce PatataRochelle BaticaNo ratings yet

- BAV Model v4.7Document27 pagesBAV Model v4.7Missouri Soufiane100% (2)