Journal of International Management

7 (2001) 295 – 315

Negotiating control and achieving performance in

international joint ventures:

A conceptual model

Aimin Yana,*, Barbara Grayb,1

a

School of Management, Boston University, 595 Commonwealth Avenue, Boston, MA 02215, USA

Department of Management and Organization, 408 Beam Business Administration Building, Pennsylvania State

University, University Park, PA 16802, USA

b

Abstract

Adapting well-established organization theories to international joint ventures (IJVs), this paper

develops an overarching theoretical model of the determinants and effects of parent control of IJVs

from an interpartner bargaining power perspective. Drawing upon power dependence, transaction

costs, and agency theories, we argue that the relative bargaining power between IJV partners serves

as the key determinant of control structure, and that control exerts a direct effect on the venture’s

performance. In addition, government influence and interpartner working relationship are critical

factors that complicate the linkage between control and performance but may help to explain past

conflicting results. Propositions regarding these relationships are formed for future empirical test,

and implications and directions for future research are provided. D 2001 Elsevier Science Inc. All

rights reserved.

Keywords: International joint ventures; Bargaining power; Control structure; Performance

1. Introduction

International joint ventures (IJVs) continue to proliferate as a hybrid form of organizational governance so much so that it has been suggested that we are stepping into an ‘‘age

* Corresponding author. Tel.: +1-617-353-4165; fax: +1-617-353-5244.

E-mail addresses: aimin@bu.edu (A. Yan), b9g@psu.edu (B. Gray).

1

Tel.: + 1-814-865-3822; fax: + 1-814-863-7261.

1075-4253/01/$ – see front matter D 2001 Elsevier Science Inc. All rights reserved.

PII: S 1 0 7 5 - 4 2 5 3 ( 0 1 ) 0 0 0 4 9 - 7

�296

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

of alliance capitalism’’ (Dunning, 1995). However, the literature on IJVs has grown to the

point that multiple perspectives are being advanced and inconsistent empirical results are

accumulating; therefore, theoretical integration and consolidation become necessary (Beamish and Killing, 1996). One of the most critical aspects of IJV management is the exercise

of control by the IJV partners, or the IJV parent firms (Beamish, 1984; Parkhe, 1993a,b). In

1984, Lecraw argued that the determinants and impact of parent control on IJVs was a

subject of considerable controversy. Despite one-and-a-half decades of additional research

(e.g., Geringer and Hebert, 1989; Yan, 1993; Hebert, 1994; Child et al., 1997), this

controversy continues.

This paper offers a theoretical integration of various explanations of management control

in IJVs. Using an interpartner bargaining perspective we develop an overarching model of

management control in IJVs drawing upon well-established organization theories (e.g., power

dependence, agency, transaction cost, and trust theories). We adapt these theories to the

context of international business partnerships. By focusing on both competitive and

cooperative dynamics between the IJV partners, we develop a theory to explain both the

determinants of control and how control and interpartner relationships interact to impact the

IJV’s ability to achieve the founding objectives of both its parent firms. The term ‘‘parent’’

refers to the multinational corporation (MNC) and the host country organization that have

invested in the joint venture. For the purposes of our discussion, however, we will use the

terms ‘‘parents’’ and ‘‘IJV partners’’ interchangeably, although it is possible that some

partners (such as government agencies who invest in IJVs) are technically not ‘‘parents.’’

Below, we review previous research and establish the need for a theoretical explanation of

control in IJVs. Then, we develop a theoretical model and offer a set of propositions to guide

future empirical investigation. Finally, we discuss the implications of the model for future

research on joint ventures that span international boundaries.

2. Previous research on control in IJVs

2.1. The nature of control

Generally, management control refers to the process by which an organization influences

its subunits to achieve its objectives (Flamholtz et al., 1985). Control in IJVs is ‘‘the most

common variable discussed in conjunction with performance’’ (Beamish, 1984, p. 45), and it

has been studied primarily in international, rather than the domestic, joint ventures. Early

research on control (e.g., Tomlinson, 1970; Franko, 1971; Stopford and Wells, 1972)

extended the concept from wholly owned international subsidiaries to the context of IJVs,

and adopted a strategic perspective that focused on the relationship between the international

strategy of the MNC, the strategy of the other partner, and IJV control. In this work particular

attention was paid to the MNC’s desire to control, rather than the actual exercise of control

(Geringer and Hebert, 1989).

A second approach to control that focuses on the control structure itself was offered by

Killing (1983). His milestone study proposed that control is inherently a relative phenom-

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

297

enon. Killing not only sharpened the conceptualization, but also shifted the unit of analysis

from the MNC parent to the IJV as an interfirm arrangement. This work has since been

followed by a stream of inquiry on control in IJVs (e.g., Schaan, 1983; Lecraw, 1984;

Beamish, 1984; Geringer and Hebert, 1989; Blodgett, 1991; Yan, 1993; Yan and Gray, 1994,

2001; Hebert, 1994; Child et al., 1997).

These studies, however, do not share a single, consistent notion of control. For example,

Geringer and Hebert (1989), building on earlier work by Schaan (1983), defined control as a

multidimensional construct comprised of the scope, the extent, and the mechanisms of

influence that the IJV parents exercise. Hebert and Beamish (1994) defined control as the

process by which behavior and output of the venture are influenced by an IJV partner.

Additionally, Child et al. (1997) largely relied on Killing’s (1983) construct.

We base our definition of control on Killing’s (1983) original one: the amount of decision

power each parent exercises in the venture’s daily operation. However, we believe that

focusing only on operational control is too limited since Yan and Gray (1994) found that IJV

parents exert management control in three different ways: (1) making strategic decisions, (2)

managing the venture’s routine operations, and (3) designing the IJV’s corporate structure and

operating procedures. Therefore, we define control as the extent of influence exercised by

each partner over these three dimensions of control: strategic, operational, and structural.

Future reference to ‘‘management control’’ in this manuscript includes all three dimensions.

Thus, ‘‘strategic control,’’ ‘‘operational control,’’ and ‘‘structural control’’ will be used to

indicate these specific types of management control. Because of the relational character of

control (Galaskiewicz, 1985; Killing, 1983), we pay special attention to the relative division

of control among the IJV’s partners across these dimensions. Thus, control is, necessarily, a

multidimensional construct and a relative one.

In addition to the structure or relative division of control among the parents, previous

research also addressed the mechanisms of control. This view stresses the parent firms’

intentions to control and argues that an IJV partner can most effectively exercise control by

integrating the IJV with this parent firm’s overall strategy and human resource practices (e.g.,

by nominating the venture’s key personnel) (Schaan, 1983; Geringer and Hebert, 1989).2 Yan

and Gray’s (1994) in-depth case studies concur that nomination of executives offers a critical

means of control at the strategic and the operational levels. Thus, a model of control should

reflect both the intention to control and the means by which control is implemented.

2.2. The determinants and effects of control

Of critical importance to the management of IJVs is how control is acquired and

maintained by the partners and whether exercise of that control produces desired outcomes.

Early research on these issues was dominated by a perspective of ‘‘intention to control,’’ first

introduced by Tomlinson (1970). Essentially, from this perspective, a partner gains and

2

It is important to note that there is a discrepancy between the conceptualization (e.g., Geringer and Hebert,

1989; Schaan, 1983; Tomlinson, 1970) and empirical operationalizations of this perspective that have typically

relied on data from the MNC partner only (e.g., Killing, 1983; Hebert and Beamish, 1994; Hebert, 1996).

�298

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

maintains control over the venture by creating and maintaining a fit between its strategy and

the IJV’s control structure (Franko, 1971; Geringer and Hebert, 1989). Franko (1971)

suggested that an MNC should tighten control over its IJVs or decrease the IJVs’ autonomy

when the parent firm attempts to standardize or centralize its international marketing policies

or consolidate production facilities. Blodgett (1991) argued that increased control over an IJV

is necessary for the parent who transfers critical strategic resources (e.g., proprietary

technologies) to the venture. In order to curb opportunism by its partners and prevent

unauthorized technology leakage, an IJV parent has to increase its control over its strategic

resources. Often, when an IJV becomes strategically important to one of the parents, this

parent firm will seek to convert the venture from a partnership to a wholly owned or

dominantly controlled entity (Killing, 1983; Hennart, 1988).

The effect of control and, particularly, the performance implications of control in IJVs have

been an extremely appealing topic for scholars and practitioners alike. However, previous

research generated inconsistent results (see Geringer and Hebert, 1989 for a review of early

research on the subject). Recent empirical efforts have consistently shown that management

control over an IJV’s daily operations exerts a strong effect on IJV performance (Yan, 1993;

Hebert and Beamish, 1994; Child et al., 1997; Mjoen and Tallman, 1997; Yan and Gray,

2001). These studies also suggest that the control–performance linkage is nonlinear and may

be moderated by other variables. Theoretical explanations of these relationships remain

underdeveloped, however.

In summary, previous studies have laid a rich conceptual foundation on which research on

control in IJVs has advanced. While the view of intention to control (Tomlinson, 1970)

suggested that the partners’ corporate strategies would influence their desire for control of an

IJV, it offered an insufficient explanation for what occurs when two or more partners’

strategies motivate them all to seek influence and control of the IJV. We argue that in IJVs the

parents must negotiate their respective strategic intention to control and reach some

accommodation about who will exercise control and how. What is needed is a theoretical

model that accounts for these negotiated relationships among the partners at the IJV’s

inception. While intention to control may serve as a critical input to these negotiations, we

focus on exercised, rather than intended, control, and argue that the structure of control

eventually adopted by the IJV depends on the partners’ relative bargaining power. Additionally, implementation of the control structure (or exercised control) occurs through dynamic

interactions among the partners. Below we build a theoretical model of the determinants of

exercised management control and its outcomes in IJVs.

3. A model of the determinants of control and its effect on performance

3.1. Bargaining power as a determinant of control

We argue that any explanation for how control is achieved must consider the relative

bargaining power of each parent. A central argument of this view is that management control,

at the time of the IJV’s founding and subsequently, is determined by the parents’ relative

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

299

bargaining power. The initial distribution of control is the result of negotiations among the

partners and the host country government, and ultimately rests on the relative bargaining

power of these parties. Once a particular control structure is established, however, changes in

relative bargaining power, such as those that occur in the obsolescing bargain (Vernon, 1977;

Hamel, 1991; Inkpen and Beamish, 1997), can precipitate its subsequent realignment.

The notion of bargaining power is rooted in power-dependence theory (Emerson, 1962),

which posits that one actor’s power is derived from another’s dependency. More specifically,

Actor A’s dependence on Actor B is ‘‘directly proportional to A’s motivational investment in

goals mediated by B, and inversely proportional to the availability of those goals to A outside

of the A–B relation’’ (Emerson, 1962, p. 32). An actor involved in an exchange transaction

can gain bargaining power by decreasing its dependence on its partner, increasing the number

and quality of alternatives that it can substitute for its relationship with this partner, cultivating

the dependence of the partner on the focal actor, or reducing the partner’s viable alternatives

(Cook, 1977; Bacharach and Lawler, 1984). From this perspective, bargaining power is

defined as the capability of the bargainers to favorably reframe or change the bargaining

relationships (Lax and Sebenius, 1986), to win accommodations from the other (Dwyer and

Walker, 1981; Tung, 1988), and to influence the outcome of a negotiation (Schelling, 1956)

that, in the case of IJV negotiations, means gaining control over the joint venture.

It is clear that power-dependence theory conceptualizes bargaining power as a relative

phenomenon, which always is assessed through interpartner comparison. ‘‘In the literature on

interorganizational relations, power has always been conceived in relational terms and, more

specifically, within a social exchange framework’’ (Galaskiewicz, 1985, p. 283). Similarly,

parent control in IJVs is also relational, as assessed by the division of control among the partners

(Killing, 1983; Beamish, 1984; Schaan, 1983; Yan and Gray, 1994). Therefore, throughout this

paper, bargaining power and management control are both treated as relational concepts, and

discussed on an interpartner comparative basis. Reference to one partner’s bargaining power or

control is always relative to the other’s. For simplicity, our discussion assumes that an IJV has

two partners. However, we note that in IJVs with more than two partners, coalitions among

partners may complicate the analysis of bargaining power somewhat.

Empirical evidence for the linkage between bargaining power and control has been accruing.

For example, Fagre and Wells (1982) reported that the MNC’s bargaining power in dealing with

a local government had a direct effect on control, as reflected in the MNC’s equity ownership in

the IJV. Similarly, Lecraw (1984) found a direct relationship between the MNC’s bargaining

power as the degree of management control it exercised as well as the ownership level it

achieved. Harrigan (1986) observed that many firms strive for majority ownership in an IJV to

gain bargaining power that leads to control over the venture’s operation. Partners may also

contribute noncapital resources to enhance their bargaining position and control in negotiations

(Harrigan and Newman, 1990; Yan and Gray, 1994; Mjoen and Tallman, 1997).

3.2. Two types of bargaining power

IJV partners can wield two kinds of bargaining power, each derived from a different source

of interdependence among the partners: context-based and resource-based bargaining power.

�300

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

As Yan and Gray (1994) and Mjoen and Tallman (1997) have shown, both kinds of

bargaining power influence the distribution of management control among the partners.

3.2.1. Context-based bargaining power

One derivative of power-dependence theory stresses the context-dependent relationships

between the bargainers. It argues that the relative bargaining power of a party depends upon

the mutual dependence of the partners and, in particular, on the exclusivity of the dependence

(Emerson, 1962; Blau, 1964; Thompson, 1967). Thus, one’s bargaining power is determined

by the alternatives available to it and by the significance of the stakes it has in the current

relationship, and is reflected in the potential outcomes of bargaining (Cook, 1977; Bacharach

and Lawler, 1984). In IJVs, this context-based bargaining power is affected by the viable

alternatives available to each partner and by the strategic importance of the IJV to each of the

partners. The party having more potential partners or alternative modal choices to enter a

market achieves greater bargaining power because it can threaten to walk away from the

current negotiation and to exercise its best alternative to a negotiated agreement (‘‘BATNA’’)

(Fisher and Ury, 1981). Our use of the term ‘‘alternatives’’ here presumes that they are

acceptable, i.e., they meet a minimum threshold of quality. There will be, of course,

variations even among the acceptable alternatives. Therefore, the quality as well as the

number of acceptable alternatives will influence a sponsor’s bargaining power such that a

party who has alternatives will feel less need to make costly concessions during negotiations.

In Propositions 1 and 2 below, we relate the number and quality of alternatives to

management control.

Proposition 1: Within an IJV, the greater the number of acceptable alternatives a partner

has during the negotiations, the greater the management control this partner is able

to achieve.

Proposition 2: Within an IJV, the better the quality of alternatives a partner has during

the negotiations, the greater the management control this partner is able to achieve.

Not all IJV partners deem the partnership to be equally important to their overall strategic

portfolio (Bartlett and Ghoshal, 1986). Firms who do deem the IJV to be of greater strategic

importance will have a greater stake in the venture and may negotiate strongly for control.

However, they are, in essence, exposing themselves to a greater risk that renders them more

dependent on their partner and reduces their bargaining power accordingly. This reduction in

bargaining power, in turn, may result in less control over the venture than they intended

unless, of course, this partner takes additional strategic actions to offset this dependence

(e.g., by making specific resource contributions, as seen below) or bargaining for specific

but limited control of the IJV (Geringer, 1988; Mjoen and Tallman, 1997). This leads to

Proposition 3.

Proposition 3: Ceteris paribus, the more strategically important the IJV is to a partner,

the more dependent this partner is on the other(s), and thus the less the management

control this partner is able to achieve.

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

301

3.2.2. Resource-based bargaining power

The second derivative of the power-dependence theory focuses on the resourcedependent relationships between the parties. Specifically, bargaining power in interorganizational settings derives from the possession or control of critical resources (Aldrich, 1977;

Pfeffer and Nowak, 1976; Pfeffer and Salancik, 1978). According to Pfeffer and Salancik

(1978, p. 27), for each organizational player in an interorganizational arrangement, ‘‘one of

the inducements received for contributing the most critical resources is the ability to control

and direct organizational action.’’ Thus, an IJV partner’s contribution in critical resources

will enhance its bargaining power and, in turn, its management control (Harrigan, 1986;

Root, 1988; Harrigan and Newman, 1990; Blodgett, 1991). Increasing empirical evidence

has also rendered support for this relationship between resource-based bargaining power

and control in IJVs (Lecraw, 1984; Yan and Gray, 1994; Child et al., 1997; Mjoen and

Tallman, 1997).

However, IJV partners contribute a variety of resources to the venture (e.g., financial

capital, technology, market access, and managerial knowledge). As Yan and Gray (1994) and

Mjoen and Tallman (1997) have argued, it is important to differentiate the effects of capital

resources and of noncapital resources on control. Capital resource-based power is derived

from contribution of financial resource or its equivalent in physical or proprietary properties.

In contrast, noncapital-based bargaining power derives from a party’s contribution of critical

tacit resources (Chi, 1994) including know-how, managerial expertise, marketing channels,

and political networks. It has been common practice in the joint venture literature to assume

that the structure of ownership (e.g., capital resource contributions) is a direct proxy for

management control (Fagre and Wells, 1982; Blodgett, 1991). While there is theoretical

evidence to support this contention, we believe it remains an empirical question — i.e., ‘‘Does

putting more money into the IJV always result in more control?’’ We offer two separate

propositions — one for capital resources and one for noncapital resources — because it is

important to determine whether the contribution of noncapital resources can offset the

presumed effect of equity on control.

Proposition 4: Within an IJV, the more capital resources a partner contributes to the

venture, the greater the management control this partner is able to achieve.

Proposition 5: Within an IJV, the more noncapital resources a partner contributes to the

venture, the greater the management control this partner is able to achieve.

3.2.3. The influence of governmental actors

Of special importance in IJVs is an exogenous factor that affects the partner bargaining

power — i.e., the role of local government as one of the major stakeholders in IJV

negotiations (Brouthers and Bamossy, 1997; Mjoen and Tallman, 1997; Pan, 1996). At a

general level, Boddewyn and Brewer (1994) argue that national governments represent ‘‘the

key political actors’’ in international business (p. 124). Even in the world’s most developed

countries, governmental influence on IJV formation can be substantial, as evidenced in the

GM–Toyota venture (NUMMI) (Weiss, 1977). The role of local government is particularly

�302

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

significant for IJVs in developing and transitional economies, in which policy making is as

much politically-as economically-based. Government restrictions on ownership structures,

business sectors or industries to form IJVs, and the venture’s target markets have long been

observed as critical factors in IJVs and foreign investment in general. For example, from the

perspectives of Chinese politics and international political economy, Pearson (1991) explains

why the Chinese government has preferred and promoted equity IJVs as an ideal form for

absorbing foreign capital. Recent case studies of Western European IJVs in Hungary and

Romania (Brouthers and Bamossy, 1997) reported that the local governments in transitional

economies exerted significant influence on the relative bargaining power of the IJV partners

at the prenegotiation, negotiation, and postnegotiation stages.

The role of government influence is quite complex in IJVs. For example, anecdotal

observations suggest that the relative bargaining power of an IJV partner will be enhanced as

a result of the influence of its own government on the IJV negotiations. This does not always

hold true, however. For instance, governments in less developed countries generally push

IJVs to export in order to make much-needed foreign exchange. This type of influence does

not necessarily align with the IJV’s local partner’s interests, and thus does not help the local

partner gain any bargaining power. Sometimes, it may serve as a counterproductive factor for

the local partner, because the MNC partner can always use its effort to satisfy or

accommodate the local government’s policy constraints and requirements as a bargaining

chip against the local partner.

In all events, however, governmental forces, as an exogenous factor, may distort the

endogenous balance in bargaining power between IJV partners, as well as the relationship

between bargaining power and control, thereby moderating in some way the relationship

between these two variables. When strong government intervention is present, uncertainties

will occur in interpartner negotiations; as a result, bargaining power will become less

predictive of the venture’s control structure. Because there are competing predictions about

the direction of the government’s influence on these negotiations, we suggest that the

following research question should guide future research:

Research Question 1: Government influence on the IJV negotiations will moderate the

relationship between bargaining power and control such that the stronger the

government interference, the less predictive of control the relative bargaining power.

We now turn our attention to the effect that the distribution of control in IJVs has on

performance outcomes. For this analysis, we draw on transaction costs and agency theories to

augment the bargaining power perspective.

3.3. The effect of control on performance

How does the exercise of management control affect the performance of an IJV? This

question has been a focus of inquiry among IJV researchers for more than a decade. Its

pursuit, however, has generated ambiguous and perplexing results (Geringer and Hebert,

1989). As some authors point out (cf. Yan and Gray, 1994; Hebert, 1994), a critical factor in

the inconsistency is the lack of a widely accepted definition of performance in IJVs.

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

303

The IJV literature reveals a variety of different conceptualizations of performance. As a

result, considerable controversy exists among scholars and practitioners alike with respect to

from whose perspective performance is evaluated, what appropriate performance measures

are, and how different measures are useful in the different stages of the venture’s evolution

(Yan and Gray, 1995). Following Yan and Gray (1994, 1995) we argue that the objectives of

the IJV’s parents, taken as a whole, provide the best basis for performance conceptualization.

Since joint ventures are formed to pursue each partner’s strategic interests, and each partner

commits critical resources toward these ends, the degree to which these goals are satisfied

constitutes an effective measure of performance. Key to our conceptualization is that

successful performance means that both partners goals are satisfied, not just those of the

MNC. Therefore, we suggest that performance should be understood in interpartner

comparative terms. For example, this could be formulated as the ratio of the extent to which

one partner’s objectives are satisfied relative to the others’ or a weighted average of the

degree of satisfaction of the primary objectives of each partner (cf. Yan and Gray, 2001).

Thus, if a joint venture is unable to meet the key expectations of both or either of its parents

over a considerably long period of time, it would not be considered a high performer. Further,

its ability to survive as constituted may become questionable (Gray and Yan, 1997; Yan and

Luo, 2001).

While many tests of the relationship between control and performance in joint ventures

have been conducted (Geringer and Hebert, 1989; Hebert, 1994; Yan and Gray, 1994; Mjoen

and Tallman, 1997), the empirical results have been conflictual, and we lack a unifying

theoretical rationale for explaining this relationship. We believe that rationale stems from the

fact that IJVs are mixed-motive games in which the partners are simultaneously engaged in

cooperation and competition (Lax and Sebenius, 1986; Hamel et al., 1989). Whereas

symbiotic interdependence (Astley and Fombrun, 1983) drives the partners to collaborate,

competitive interdependence provides incentives for each partner to pursue its own interests.

Therefore, we draw on transaction costs and agency perspectives to explain the competitive

dynamics and theories of trust development to explain the cooperative dynamics. Together,

these theories explain how control and performance are related.

We draw on two concepts from transaction costs theory. The first is the notion of

incomplete contracts and the second is opportunism. According to transaction cost theory,

firms form joint ventures to overcome the uncertainties associated with the incompleteness

of market contracts (Coase, 1937; Alchian and Demsetz, 1972; Crocker and Masten, 1988).

However, a joint venture also represents a kind of incomplete contract in which the

partners have to live with substantial uncertainties down the road (Crocker and Masten,

1988) — i.e., the outcomes of their cooperation will not be apparent until years. In order to

minimize these uncertainties, IJV partners seek management control. In addition, each

partner is vulnerable to opportunism (Williamson, 1975) potentially engaged in by its

counterpart, and it is difficult, if not impossible, for each party to sort out ex ante who will

be an opportunistic partner. Therefore, gaining management control can be considered as

both a defensive and a proactive strategy. Used defensively, control can be exercised by a

partner to overcome opportunism possibly engaged in by other partners (Hansen and

Hoskisson, 1996). Since the partners do not have complete information about each other or

�304

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

about the future of the prospective IJV at its formation (Kogut, 1991; Chi and McGuire,

1996), their initial relationships resemble arm’s-length market transaction in which

competition and prevention of opportunism are the norm (Williamson, 1991). The potential

for opportunism exists until the partners develop a reputation of trustworthiness with each

other (Parkhe, 1993b).

Exercise of management control can also be used as a proactive strategy for IJV partners to

attenuate uncertainty and to achieve their own strategic interests. Because IJVs are not a pure

form of a hierarchical structure like the case of mergers or wholly owned subsidiaries, a

complete elimination of selfish behavior is impossible (Williamson, 1985; Hennart, 1988; Chi

and McGuire, 1996). Especially, as Chi (1996) argues, when a partner’s commitment cannot

be precisely monitored or verified, this partner has an incentive to pursue its own interests at

the expense of the interests of other partners or of the IJV. Newman (1992, p. 78) observed:

‘‘Each potential partner, thinking about its own wants and resources, would like the lion’s

share of the benefits of the cooperative activity. Relative power comes into play.’’ This is

particularly true when the partners have differing strategic interests for forming the IJV, and

these interests are not perfectly compatible.

To summarize, from the transaction costs perspective, exercise of management control by a

partner enables it not only to alleviate the potential opportunism engaged by the IJV’s other

partners, but also to use the IJV’s common stock of resources to pursue its own strategic

interests. As a result, the achievement of this partner’s strategic objectives should be

enhanced. Therefore, according to the transaction cost approach, if one partner has dominant

control, this should affect performance by increasing the achievement of their particular

objectives (over their partners).

Agency theory can also shed light on the relationship between control and performance.

An agency relationship exists when one economic entity (the principal) authorizes the other

(the agent) to act on the principal’s behalf (Fox, 1984; Eisenhardt, 1989). Because of the

inherent conflict between the self-interests of the principal and the agent, agency costs occur

when the agent does not act in the best interest of the principal (Jensen and Meckling, 1976).

At the more general level, agency problems are ‘‘metering problems’’ (Alchian and Demsetz,

1972) that occur when two economic entities, as a team, jointly produce output. Unless

monitoring occurs, each team member will not necessarily pursue the best interests of the

other member or those of the team as a whole, but will act opportunistically to pursue its own

strategic interests (Moe, 1984).

It is arguable that IJVs resemble such a team — ‘‘a team whose members act from selfinterest but realize that their destinies depend to some extent on the survival of the team in its

competition with other teams’’ (Fama, 1980, p. 289). The team, in the case of IJVs, involves

two or more partners jointly producing output (e.g., the joint venture’s products). The agency

problem in IJVs is rooted in the divergent self-interests of the parents and their objectives for

the venture’s operation. This is particularly true for IJVs created between developed and

developing country partners. Each partner has strategic interests and objectives that are not

salient for the other, but still they must rely on the other to achieve them. Therefore, each

partner (the hypothetical principal) gives the other’s management personnel in the IJV

(the hypothetical agents) authority to act on the former’s behalf (Fox, 1984).

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

305

Both transaction costs theory and agency theory predict that the partner with greater

control of the IJV will use the common pool of resources to pursue its own interests (i.e., to

achieve its own objectives) rather than those of its partner or the best interest of the IJV

overall. Therefore, in effect, the management control structure becomes a critical vehicle

through which decisions about whose objectives to pursue are made. As a result, an IJV with

a dominant-control structure (Killing, 1983) would be expected to satisfy more of its

dominant parent’s objectives than those of its nondominant parents. By the same logic, in

shared-control IJVs (Killing, 1983), the extent to which the objectives of both partners are

achieved should be relatively equal. To summarize, we hypothesize a direct, positive

relationship between the degree of a partner’s control and the extent of achievement of its

objectives compared with those of its partner(s).

Proposition 6: The greater management control a parent exercises over the IJV, the more

likely this partner will achieve its own strategic objectives for the joint venture over

those of its partner(s).

3.4. The effect of the interpartner working relationship on performance

So far we have proposed a direct relationship between the IJV’s control structure and the

achievement of the partners’ objectives. However, other factors have also been posited to

have an effect on IJV performance, and, to work in conjunction with control to influence IJV

outcomes. Those scholars who argue that joint ventures are opportunity maximizing

endeavors rather than only opportunism minimizing ones (e.g., Zajac and Olsen, 1993;

Hansen and Hoskisson, 1996) as well as many other scholars have argued that the quality of

the working relationship among IJV partners affects the overall performance (Davidson,

1982; Tung, 1984; Beamish and Banks, 1987; Koenig and van Wijk, 1991; Newman, 1992;

Yan and Gray, 1994; Madhok, 1995; Child, 1997; Hebert, 1996). Two aspects of the partners’

working relationship are deemed important: interpartner trust and consensus or conflict about

goals between the partners.

3.4.1. Trust

Several theorists have argued that transaction costs explanations are insufficient to account

for relational dynamics within joint ventures and that trust is another critical explanatory

variable (Barney and Hansen, 1994; Zaheer and Venkatraman, 1995; Madhok, 1995;

Nooteboom et al., 1997; Das and Teng, 1998). Multiple conceptions of trust have been

considered in the literature. Ring and Van de Ven (1992) distinguish calculative forms of trust

from confidence in another’s goodwill. Lewis and Weigert (1985) distinguish leaps of faith

from trust based on reason and experience. Lewicki and Bunker (1995) identify three types of

trust: calculus-based, knowledge-based, and identification-based trust. Calculative trust

occurs when farsighted parties recognize the potential benefits of their continued interaction

and expect that the other party will behave predictably (Williamson, 1993). In knowledgebased trust, one person relies on another because of direct knowledge about their behavior.

Parties with identification-based trust develop a social bond with each other based on mutual

�306

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

appreciation of each other’s needs. Distinguishing calculative from other forms of trust

appears particularly useful for understanding how trust works in joint ventures.

Development of trust among IJV partners can have a direct positive effect on performance.

For example, if both partners exhibit what Barney and Hansen (1994) refer to as ‘‘strong form

trust,’’ they can reduce the costs of governance mechanisms that would be required for lesser

forms of trust and exploit exchange opportunities afforded by it, thereby gaining competitive

advantage. Strong form trust is exogenous to an alliance’s governance structure and is derived

instead from values, principles, and standards that the partners share. Thus, it is akin to

Lewicki and Bunker’s ‘‘identity-based trust.’’ The presence of such trust should enable the

parties to work out ambiguities in the contract, correct errors, cope with uncertainty, solve

problems better (Crocker and Masten, 1988; Mohr and Spekman, 1994), and work to achieve

integrative outcomes that allow all parties to satisfy their objectives (Pruitt and Lewis, 1977;

Fisher and Ury, 1981; Lax and Sebenius, 1986). Mohr and Spekman (1994) found evidence

of the effects of such trust satisfaction with profit in strategic alliances between automobile

manufacturers and dealers. Similarly, Saxton (1997) demonstrated a positive relationship

between shared decision making (indicative of trust) and performance. Therefore, we offer

Proposition 7.

Proposition 7: The presence of a trusting relationship among IJV partners will have a

direct, positive effect on the IJV’s performance.

Another way that trust can operate in IJVs is via an interaction effect with control. If trust

is present, it can cut transaction costs by reducing the need for formal contracts (Bromiley and

Cummings, 1995; Hansen and Hoskisson, 1996) and serve as an alternative mechanism to

guard against opportunism (Hill, 1990; Barney and Hansen, 1994; Zaheer and Venkatraman,

1995). Both trust and control contribute to partners’ confidence that their counterpart will

‘‘pursue mutually compatible interests in the alliance, rather than act opportunistically’’

(Das and Teng, 1998, p. 491). Consistent with this, Nooteboom et al. (1997) showed that trust

reduced the probability of perceived loss for alliance partners.

It appears, then, that control and trust may interact to affect performance. For example,

in a case study of the Nantong Cellulose Fibers Company, Newman (1992) showed that

trust played a major role in the willingness of the U.S. partner to accept a minority equity

ownership and to transfer responsibility for its IJV’s operations to the Chinese parent. In a

study of Canadian manufacturing IJVs, Hebert (1996) found that trust was positively

related to performance in dominant but not in shared-control IJVs. Additionally, in a study

of North American–Japanese IJVs, trust only had an indirect effect on performance (Inkpen

et al., 1997).

Moreover, trust may influence performance differently under different control conditions.

In shared-control IJVs, where trust is necessarily higher, control may be sufficient to predict

performance. In dominant-control IJVs, however, trust may be a necessary companion of

control, if high levels of performance are desired. This relationship was confirmed by

research that found a positive association between trust and quasi-integration between

independent insurance agencies and insurance companies (Zaheer and Venkatraman, 1995).

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

307

Therefore, we propose that the interaction of trust and control will influence performance as

Proposition 8 states.

Proposition 8: A trusting relationship between the partners will moderate the linkage

between parent control and IJV performance such that the stronger the interpartner trust,

the weaker the effect of control on performance.

It is important to note, however, that trust between the IJV partners can change over time

(Hamel, 1991; Yan and Gray, 1994) and that its relationship to IJV performance may be

reciprocal longitudinally (Killing, 1983; Gulati, 1995; Zaheer and Venkatraman, 1995). We

take up this issue in the discussion of future research below.

3.4.2. Consensus or conflict about goals

One ingredient in a superior working relationship between the partners, and particularly,

between the two groups of managers nominated by the local and foreign partner, respectively,

is similarity in operating philosophies (Narus and Anderson, 1987; Hill and Hellriegel, 1994;

Yan and Gray, 1994). Addressing interfirm relationships, Ring and Van de Ven (1994) note

that it is pivotal for the participating firms to create consensus on the key cultural expectations, purposes, and values that govern the interfirm arrangement. Such consensus,

according to these authors, serves as ‘‘psychological contracts among parties’’ (p. 101) and

increases the partners’ formal commitment to the cooperation. To the extent that the partners

have a consensus on the IJV’s mission, goals, and operating procedures, less coordination

among the partners is needed, opportunism and monitoring costs will decrease, and the

overall chances of IJV success will improve as a result. Das and Teng (1998, p. 506) explain,

Participatory decision making serves the purpose of controlling, because in the process

partners interact among themselves to gain a better understanding of each other. As a result,

collective norms and values of the alliance are developed. Because the goal-setting process

allows partners to form a consensus gradually, their incentive to deviate from agreed-upon

objectives tends to be significantly curbed.

If, on the other hand, partners experience considerable conflict in working together, they

are less likely to reach decisions that they both can support (Mohr and Spekman, 1994).

Conflict between the partners can indicate disagreement over goals, operational and

managerial expectations, send confusing signals to the IJV managers and employees (Lyles

and Salk, 1997), and thereby hamper performance levels (Tillman, 1990; Anderson and

Narus, 1990). While Hebert (1996) found that the level of conflict was negatively related to

performance, the relationship only held for dominant, but not shared-control IJVs. Mohr and

Spekman (1994), on the other hand, found direct positive relationships between conflict

resolution and partner satisfaction. We suspect that conflicts can jeopardize performance in

any joint venture, but that some IJVs may be better able than others to find integrative

resolution to such conflicts. These ideas are reflected in Proposition 9 (a and b):

Proposition 9: Unresolved interpartner conflict over (a) the IJV’s mission and goals and

(b) its operational procedures will be negatively related to performance of the IJV.

�308

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

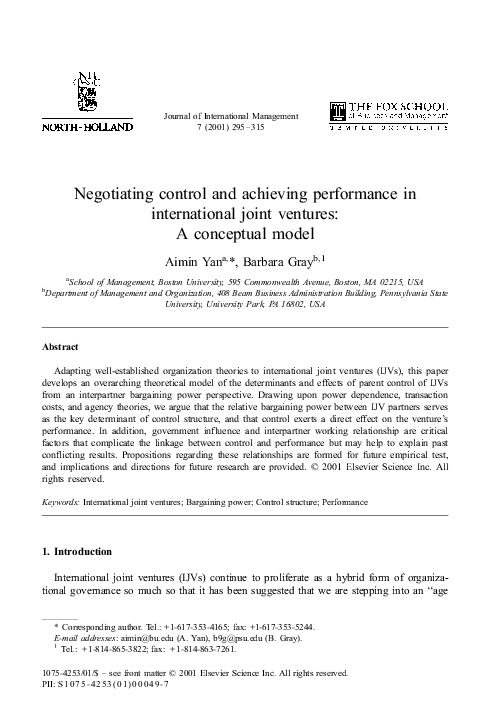

Fig. 1. A conceptual model of parent control in international joint ventures.

It also seems likely that trust and goal consensus or conflict are related. One would expect

that, at least to a point, consensus about goals would lead to increased trust whereas continued

conflict over goals would diminish trust and vice versa. Consensus about goals, however,

may be unrealistic, since one reason that partners form IJVs is to capitalize on their

differences. Still, if the partners reach integrative agreements, trust should increase. The

possible negative and reciprocal relationship between trust and unresolved conflict in IJVs

warrants further research. In Fig. 1 we provide a model to summarize all the relationships

suggested in our propositions and research questions.

4. Implications and future research

4.1. Contributions and implications for understanding IJVs

In this paper we have developed a conceptual model of the determinants and effects of

control in IJVs, which helps to overcome the controversy in the extant literature about how

control is decided, how it is exercised, and how it impacts IJV performance. We posit an

interpartner bargaining power perspective on IJV control that draws upon power dependence,

agency and transaction costs theories, and theories about trust to explain these aspects of

control. While acknowledging that IJV partners may desire to control the IJV, we stress that it

is critical to acknowledge the interests of both partners, as well as the host government, and

how the potentially competing interests of these parties are reconciled. We propose that the

IJV’s partners must negotiate their respective intentions and reach some accommodation

about who will exercise control and how. In addition to the partners’ sheer desires for control,

several factors can influence the outcome of these negotiations including the resources the

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

309

partners contribute to the IJV, the host government’s stipulations, and the alternatives

available to the partners. Our perspective on control respects both partners’ roles in

determining the IJV’s control structure, considers the relative power and control of the

partners, and treats the IJV as an arena in which the partners interact, rather than as solely a

quasi-subsidiary of the MNC parent.

A complete theoretical explanation for the determinants of control in IJVs rests on the

integration of the strategic intention (Tomlinson, 1970) and the bargaining power perspectives. Thus, the division of control among IJV partners is a result of the interaction between

what a partner wants and what it can obtain (Blodgett, 1991; Tallman and Shankar, 1994).

The former corresponds to an IJV parent’s desire for control, whereas the latter depends on its

relative bargaining power vis-à-vis its partner. Thus, a parent’s control in the venture can be

seen as a compromise between its ‘‘wants’’ and its ‘‘ability to get what it wants.’’

Longitudinally, we expect that the two perspectives converge: A partner can increase its

bargaining power to achieve its unmatched strategic intentions over time, whereas the

formulation of new strategic intentions can only be done in the context of the current balance

of bargaining power between the partners.

Our model also raises an alternative explanation for why partners contribute strategic

resources, an issue of both theoretical and practical importance (Chi, 1994). Previous research

on IJVs argues that MNCs tend to minimize their resource contributions to IJVs in order to

maintain maximum appropriability of these resources and to minimize opportunism by the

learning-oriented local partner (Hamel, 1991). Thus, it adopts a conservative and defensive

stance recommending that the MNC only increase its ownership holdings in the IJV in order

to protect its nonequity resources (Blodgett, 1991). Although this approach may enable the

partner to protect its resource contribution, it does not address the partner’s need for

exercising control over the IJV’s strategy or operations. The model we offer in this paper,

on the other hand, adopts an offensive strategy, committing resources necessary to gain a

desirable level of control over the entire operation of the IJV (Harrigan, 1986) or its key

functional areas (Killing, 1983; Hebert, 1994), not just over the protection of resources.

Although an IJV partner can use resources strategically to enhance the negotiations over

control, the negotiated outcome will reflect other contingencies as well, such as government

pressure and context-based bargaining power. The strategy of increasing equity holdings to

protect nonequity resources, for example, is not always possible because the IJV’s

ownership split may be constrained by local government stipulations. The bargaining power

perspective, on the other hand, allows for the possibility of gaining dominant management

control over the IJV’s operation and appropriability of the resources with 50% or less

ownership, an outcome that is especially relevant for MNCs forming IJVs in developing

countries (Beamish, 1988).

Other advantages of the bargaining power model are that it treats IJVs as a truly joint

organizational effort (instead of a quasi-subsidiary of the MNC parent), regards both partners

as equally critical to IJV success, and focuses on the partners’ relative positions and

interactions in the IJV. We deem this shift of focus both theoretically and managerially

important because it fits the trend of the globalized economy in which international

businesses are conducted via multilateral negotiations rather than an imperial practice in

�310

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

which MNCs from the developed world impose control over their exchange partners from

developing countries.

The bargaining power model acknowledges both competitive and cooperative dynamics

that occur simultaneously in IJVs (Hamel et al., 1989; Zajac and Olsen, 1993), allows for the

possibility of integrative as well as distributive outcomes (Lax and Sebenius, 1985), and

acknowledges the potential benefits that accrue from a positive working relationship among

the partners. We suggest that previous, inconsistent results for the relationship between

control and performance may be explained by the interaction between trust and control. In

effect, trust may be a necessary supplement to formal control to ensure high levels of

performance under some circumstances. Trust not only serves as a safeguard against

opportunism, but, coupled with productive conflict resolution, it also enables the partners

to capitalize on synergies and to generate creative opportunities that provide competitive

advantage (Barney and Hansen, 1994; Hansen and Hoskisson, 1996).

4.2. Future research directions

As a key direction for future research, we would like to stress the dynamic nature of

control in IJVs. Although its underlying premises are dynamic (particularly when it is used at

multiple times), the model, as we presented it, remains static and captures only a snapshot

picture (e.g., at the IJV’s founding). Since IJVs are extremely dynamic and notoriously

unstable, calls for research on the dynamic development of IJVs have been made by a number

of scholars (e.g., Wood and Gray, 1991; Parkhe, 1993a; Yan and Gray, 1994; Doz, 1996).

Change in partner bargaining power can result from several factors associated with the

context in which the IJV is operating, the IJV’s performance or the partners themselves. For

example, shifts in context-based power can result when a partner’s strategic stakes in the

venture change, or when potential new alternatives become more attractive than continuing

the IJV. Yan and Gray (1994) observed in one of their case studies that as one partner’s other

business operations suffered severe losses, its interest in a profitable IJV became strategically

more significant. Similarly and obviously, a partner can gain or lose bargaining power as it

increases or decreases its resource contributions to the IJV, respectively. Shifts in bargaining

power can also occur because of interpartner learning (Vernon, 1977; Hamel, 1991; Inkpen

and Beamish, 1997), in which strategic resources and tacit knowledge, in particular, transfer

between the partners or between a particular parent and the venture.

However, an increase or decrease of one partner’s bargaining power may be insufficient to

precipitate a shift in control because the change may be offset by similar changes in the other

partner’s bargaining power over the same period of time (Yan and Gray, 1994). The control

structure will change only when significant shifts occur in relative bargaining power and

partners elect to use this leverage to increase their control over the IJV (Gray and Yan, 1997;

Yan, 1998).

A dynamic theory of IJVs should also consider other factors that can produce change such

as a shift in the IJV’s performance (Killing, 1983; Yan and Gray, 1994; Gray and Yan, 1997),

construction and destruction of trust, changes in government intervention, and the effect of

organizational inertia. As noted earlier, trust may be an outcome, as well as an antecedent of

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

311

superior performance or successful prior experience. As noted by Gulati (1995), trust emerges

from repeated alliances among the same partners.

Since the conceptual model is subject to future empirical tests, here we would like to offer

some suggestions for testing the proposed theoretical model. We specifically consider

methodological issues concerning data collection, operationalization and measurement. Since

IJVs involve at least three individual organizational entities — a foreign parent, a local parent,

and the venture’s management, multisource data collection is necessary. For accurate data on

the context-based and the resource-based components of bargaining power, ideal informants

(interviewees or survey respondents) would be those who personally participated in the

venture’s founding and subsequent negotiations. Measuring management control is a complex

task because it deals with control at different levels (e.g., strategic control, operational

control, structural control, as Yan and Gray, 1994 suggested) and on different dimensions

(scope, extent, mechanisms, and overall control, as Geringer and Hebert, 1984 and Hebert,

1994 proposed). Whatever indicators of control are adopted, it is our strong recommendation

that bargaining power and control be measured on an interpartner comparative basis. As we

stressed in the paper, power and control are necessarily relative concepts. The absolute

amount of power or control a particular partner possesses without considering that of the

other partner is not meaningful. In fact, lack of consistency between conceptualization and

operationalization may be a main factor in the inconsistent previous findings.

With respect to performance, it has been well documented that IJV partners may have

different goals and objectives (Yan and Gray, 1994; 1995; Osland and Cavusgil, 1996), and

each may consider some performance measures as extremely relevant and critical, while other

measures unimportant or irrelevant. We suggest that future empirical studies use multiple

measures that incorporate multiple parties’ perspectives. While it is pivotal to consider the

parent firms’ key interests, it is also critical to incorporate the operational goals and objectives

of the IJV’s management, as a separate organizational entity. Finally, in order to tease out the

temporal effects of the model’s variables, longitudinal studies of IJVs become an imperative.

References

Alchian, A.A., Demsetz, H., 1972. Production, information costs, and economic organization. Am. Econ. Rev. 62,

777 – 795.

Aldrich, H.E., 1977. Visionaries and villains: the politics of designing interorganizational relations. Organ. Adm. 8

(2 and 3), 23 – 40.

Anderson, J.C., Narus, J.A., 1990. A model of distributor firm and manufacturer firm working partnerships.

J. Mark. 54, 42 – 58 (January).

Astley, W.G., Fombrun, C.F., 1983. Collective strategy: social ecology of organizational environments. Acad.

Manage. Rev. 8 (4), 576 – 587.

Bacharach, S.B., Lawler, E.J., 1984. Bargaining: Power, Tactics, and Outcomes. Jossey-Bass, San Francisco, CA.

Barney, J.B., Hansen, M.H., 1994. Trustworthiness as a source of competitive advantage. Strategic Manage. J. 15,

175 – 190.

Bartlett, C.A., Ghoshal, S., 1986. Tap your subsidiaries for global reach. Harv. Bus. Rev. 6, 87 – 94.

Beamish, P.W., 1984. Joint venture performance in developing countries. Unpublished doctoral dissertation,

University of Western Ontario.

�312

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

Beamish, P.W., 1988. Multinational joint ventures in developing countries. Routledge, New York.

Beamish, P., Banks, J.C., 1987. Equity joint ventures and the theory of the multinational enterprise. J. Int. Bus.

Stud. 18 (2), 1 – 16.

Beamish, P.W., Killing, P., 1996. Global perspectives on cooperative strategies. J. Int. Bus. Stud. 27 (5).

Blau, P.M., 1964. Exchange and Power in Social Life. Wiley, New York.

Blodgett, L.L., 1991. Partner contributions as predictors of equity share in international joint ventures. J. Int. Bus.

Stud., First Quarter, 63 – 78.

Boddewyn, J.J., Brewer, T.L., 1994. International-business political behavior: new theoretical directions. Acad.

Manage. Rev. 19 (1), 119 – 143.

Bromiley, P., Cummings, L.L., 1995. Transaction costs in organizations with trust. Res. Negotiation Organ. 5,

219 – 247.

Brouthers, K.D., Bamossy, G.J., 1997. The role of key stakeholders in international joint venture negotiations:

case studies from Eastern Europe. J. Int. Bus. Stud. 28 (2), 285 – 308.

Chi, T., 1994. Trading in strategic resources: necessary conditions, transaction cost problems, and choice of

exchange structure. Strategic Manage. J. 15 (4), 271 – 290.

Chi, T., 1996. Performance verifiability and output sharing in collaborative ventures. Manage. Sci. 42 (1),

93 – 109.

Chi, T., McGuire, D.J., 1996. Collaborative ventures and value of learning: integrating the transaction cost and

strategic option perspectives on the choice of market. J. Int. Bus. Stud. 27 (2), 285 – 307.

Child, J., 1997. Trust and international strategic alliances: the case of Sino – foreign joint ventures. Paper presented

at the Fourth International Conference on Multi-Organizational Partnerships and Co-operative Strategy, Oxford, UK, July.

Child, J., Yan, Y., Lu, Y., 1997. Ownership and control in Sino – foreign joint ventures. In: Beamish, P.W.,

Killing, J.P. (Eds.), Cooperative Strategies: Asian Pacific Perspectives. New Lexington Press, San Francisco,

CA, pp. 181 – 225.

Coase, R.H., 1937. The nature of the firm. Economica 4, 386 – 405.

Cook, K., 1977. Exchange and power in networks of interorganizational relations. Sociol. Q. 18, 62 – 82.

Crocker, K.J., Masten, S.E., 1988. Mitigating contractual hazards: unilateral options and contract length. Rand

J. Econ. 19 (3), 327 – 343.

Das, T.K., Teng, B.-S., 1998. Between trust and control: developing confidence in partner cooperation in alliances.

Acad. Manage. Rev. 23 (3), 491 – 512.

Davidson, W.H., 1982. Global Strategic Management. Wiley, New York.

Doz, Y.L., 1996. The evolution of cooperation in strategic alliances: initial conditions or learning processes?

Strategic Manage. J. 17, 55 – 85 (Summer).

Dunning, J.H., 1995. Reappraising the eclectic paradigm in an age of alliance capitalism. J. Int. Bus. Stud. 26 (3),

461 – 491.

Dwyer, F.R., Walker Jr., O.C., 1981. Bargaining in an asymmetrical power structure. J. Mark. 104 – 115 (Winter).

Eisenhardt, K.M., 1989. Agency theory: an assessment and review. Acad. Manage. Rev. 14 (1), 57 – 74.

Emerson, R., 1962. Power-dependence relations. Am. Sociol. Rev. 27, 31 – 41.

Fagre, N., Wells Jr., L.T., 1982. Bargaining power of multinationals and host governments. J. Int. Bus. Stud. 3,

9 – 23 (Fall).

Fama, E.F., 1980. Agency problems and the theory of the firm. J. Polit. Econ. 88, 288 – 305.

Fisher, R., Ury, W., 1981. Getting to YES: Negotiating Agreement Without Giving In. Penguin Books, New York.

Flamholtz, E.G., Das, T.K., Tsui, A.S., 1985. Toward an integrative framework of organizational control. Account.

Organ. Soc. 10 (1), 35 – 50.

Fox, R., 1984. Agency theory: a new perspective. Manage. Account. 62 (2), 36 – 38.

Franko, L.G., 1971. Joint Venture Survival in Multinational Corporations. Praeger Publishers, New York.

Galaskiewicz, J., 1985. Interorganizational relations. Annu. Rev. Sociol. 11, 281 – 304.

Geringer, J.M., 1988. Joint Venture Partner Selection: Strategies for Developed Countries. Quorum Books,

Westport, CT.

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

313

Geringer, J.M., Hebert, L., 1989. Control and performance of international joint ventures. J. Int. Bus. Stud.,

235 – 254 (Summer).

Gray, B., Yan, A., 1997. The formation and evolution of international joint ventures: examples from U.S. – Chinese

partnerships. In: Beamish, P.W., Killing, J.P. (Eds.), Cooperative Strategies: Asian Perspectives. New Lexington Press, San Francisco, pp. 57 – 88.

Gulati, R., 1995. Does familiarity breed trust? The implications of repeated ties for contractual choice in alliances.

Acad. Manage. Rev. 38 (1), 85 – 112.

Hamel, G., 1991. Competition for competence and inter-partner learning within international strategic alliances.

Strategic Manage. J. 12, 83 – 103.

Hamel, G., Doz, Y., Prahalad, C.K., 1989. Collaborate with your competitors and win. Harv. Bus. Rev.

133 – 139 (January).

Hansen, M.H., Hoskisson, R.E., 1996. Paper submitted to the Management and Organization Theory Division,

Academy of Management, January.

Harrigan, K.R., 1986. Managing for Joint Venture Success. Lexington Books, Lexington, MA.

Harrigan, K.R., Newman, W.H., 1990. Bases of interorganization cooperation: propensity, power, persistence.

J. Manage. Stud. 27 (4), 417 – 434.

Hebert, L., 1994. Division of control, relationship dynamics and joint venture performance. Unpublished PhD

dissertation, the University of Western Ontario.

Hebert, L., 1996. Trust and conflict in international joint ventures: The role of control structures. Paper presented

at the annual meeting of the Academy of Management, Cincinnati.

Hebert, L., Beamish, P.W., 1994. The control – performance relationship in international vs. domestic joint ventures. Paper presented at the annual meeting of the Academy of Management, Dallas.

Hennart, J.-F., 1988. A transaction costs theory of equity joint ventures. Strategic Manage. J. 9 (4), 361 – 374.

Hill, C.W.L., 1990. Cooperation, opportunism, and the invisible hand: implications for transactions cost theory.

Acad. Manage. Rev. 15 (3), 500 – 513.

Hill, R.C., Hellriegel, D., 1994. Critical contingencies in joint venture management. Organ. Sci. 5 (4), 594 – 607.

Inkpen, A.C., Beamish, P.W., 1997. Knowledge, bargaining power and international joint venture instability.

Acad. Manage. Rev. 22 (1), 177 – 202.

Inkpen, A., Currall, S., Hughes, S., 1997. International joint venture trust: an empirical examination. Paper

presented at the Fourth International Conference on Multi-Organizational Partnerships and Co-operative Strategy, Oxford, UK, July.

Jensen, M.C, Meckling, W.H., 1976. Theory of the firm: managerial behavior, agency costs, and ownership

structure. J. Financ. Econ. 3, 305 – 360.

Killing, J.P., 1983. Strategies for Joint Venture Success. Praeger Publishers, New York.

Koenig, C., van Wijk, G., 1991. Interfirm alliances: the role of trust. In: Thietart, R.A., Thepob, J. (Eds.),

Microeconomic Contribution to Strategic Management. North-Holland Elsevier: Advanced Series in Management, pp. 1 – 16 (Chapter 9), North-Holland Elsevier, Amsterdam.

Kogut, B., 1991. Joint ventures and the option to expand and acquire. Manage. Sci. 37 (1), 19 – 33.

Lax, D.A., Sebenius, J.K., 1986. The Manager as Negotiator. Free Press, New York.

Lecraw, D.J., 1984. Bargaining power, ownership, and profitability of transnational corporations in developing

countries. J. Int. Bus. Stud. 27 – 43 (Spring/Summer).

Lewicki, R.J., Bunker, B.B., 1995. Trust in relationships: a model of development and decline. In: Bunker, B.B.,

Rubin, J.Z. et al., (Eds.), Conflict, Cooperation and Justice: Essays Inspired by the Work of Moreton Deutsch.

Jossey-Bass, San Francisco.

Lewis, J.D., Weigert, A., 1985. Trust as a social reality. Soc. Forces, 63, 967 – 985.

Lyles, M.A., Salk, J.E., 1997. Knowledge acquisition from foreign parents in international joint ventures: an

empirical examination in the Hungarian context. J. Int. Bus. Stud. 27 (5), 877 – 903.

Madhok, A., 1995. Revisiting multinational firms’ tolerance for joint ventures: a trust-based approach. J. Int. Bus.

Stud. 26 (1), 117 – 137.

Mjoen, H., Tallman, S., 1997. Control and performance in international joint ventures. Organ. Sci. 8 (3), 257 – 274.

�314

A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

Moe, T.M., 1984. The new economics of organization. Am. J. Polit. Sci. 28, 737 – 777.

Mohr, J., Spekman, R., 1994. Characteristics of partnership success: partnership attributes, communication behavior, and conflict-resolution techniques. Strategic Manage. J. 15, 135 – 152.

Narus, J.A., Anderson, J.C., 1987. Distributor contributions to partnerships with manufacturers. Bus. Horiz. 30,

34 – 42.

Newman, W.H., 1992. Launching a viable joint venture. Calif. Manage. Rev. 68 – 80 (Fall).

Nooteboom, B., Berger, H., Noorderhaven, N.G., 1997. Effects of trust and governance on relational risk. Acad.

Manage. J. 40 (2), 308 – 338.

Osland, G.E., Cavusgil, S.T., 1996. Performance issues in US – China joint ventures. Calif. Manage. Rev. 38 (2),

106 – 130.

Pan, Y., 1996. Influences on foreign equity ownership level in joint ventures in China. J. Int. Bus. Stud. 27 (1),

1 – 26.

Parkhe, A., 1993a. ‘‘Messy’’ research, methodological predispositions, and theory development in international

joint ventures. Acad. Manage. Rev. 18 (2), 227 – 268.

Parkhe, A., 1993b. Strategic alliance structuring: a game theoretic and transaction-cost examination of interfirm

cooperation. Acad. Manage. J. 36 (4), 794 – 829.

Pearson, M.M., 1991. Joint Ventures in the People’s Republic of China: The Control of Foreign Direct Investment

Under Socialism. Princeton Univ. Press, Princeton, NJ.

Pfeffer, J., Nowak, P.P., 1976. Joint ventures and interorganizational interdependence. Adm. Sci. Q. 21,

398 – 418.

Pfeffer, J., Salancik, G.R., 1978. The External Control of Organizations. Harper & Row, New York.

Pruitt, D.G., Lewis, S.A., 1977. The psychology of integrative bargaining. In: Druckman, D. (Ed.), Negotiations:

Social Psychological Perspectives. Sage, Beverly Hills, CA.

Ring, P.S., Van de Ven, A.H., 1992. Structuring cooperative relationships between organizations. Strategic

Manage. J. 13, 483 – 498.

Ring, P.S., Van de Ven, A.H., 1994. Developmental processes of cooperative interorganizational relationships.

Acad. Manage. Rev. 19 (1), 90 – 118.

Root, F.R., 1988. Some taxonomies of international cooperative arrangements. In: Contractor, F.J., Lorange, P.

(Eds.), Cooperative Strategies in International Business. Lexington Books, Lexington, MA, pp. 69 – 80.

Saxton, T., 1997. The affects of partner and relationship characteristics on alliance outcomes. Acad. Manage. J. 40

(2), 443 – 461.

Schaan, J.-L., 1983. Parent control and joint venture success: the case of Mexico. Unpublished doctoral dissertation, University of Western Ontario.

Schelling, T., 1956. An essay on bargaining. Am. Econ. Rev. 46, 281 – 306.

Stopford, J.M., Wells, L.T., 1972. Managing the Multinational Enterprise. Basic Books, New York.

Tallman, S., Shankar, O., 1994. A managerial decision model of international cooperative venture formation.

J. Int. Bus. Stud. 25 (1), 91 – 113.

Thompson, J.D., 1967. Organizations in Action. McGraw-Hill, New York.

Tillman, A.U., 1990. The influence of control and conflict on performance of Japanese – Thai joint ventures.

Unpublished DBA dissertation, Nova University, Ft. Lauderdale, FL.

Tomlinson, J.W.C., 1970. The Joint Venture Process in International Business: India and Pakistan. MIT Press,

Cambridge, MA.

Tung, R.L., 1984. Business Negotiations with the Japanese. Lexington Books, Lexington, MA.

Tung, R.L., 1988. Toward a conceptual paradigm of international business negotiations. Adv. Int. Comp. Manage.

3, 203 – 219.

Vernon, R., 1977. Storm Over Multinationals. Harvard Univ. Press, Cambridge, MA.

Weiss, S.E., 1977. Creating the GM – Toyota joint venture: a case in complex negotiation. Columbia J. World Bus.

57 – 65 (Summer).

Williamson, O.E., 1975. Markets and Hierarchies: Analysis and Anitrust Implications, a Study in the Economics

of Internal Organization. Free Press, New York.

�A. Yan, B. Gray / Journal of International Management 7 (2001) 295–315

315

Williamson, O.E., 1985. The Economic Institutions of Capitalism: Firms, Markets, Relational Contracting. Free

Press, New York.

Williamson, O.E., 1991. Comparative economic organization: the analysis of discrete structural alternatives. Adm.

Sci. Q. 36, 269 – 296.

Williamson, O.E., 1993. Calculativeness, trust and economic organization. J. Law Econ. 30, 131 – 145.

Wood, D.J., Gray, B., 1991. Toward a comprehensive theory of collaboration. J. Appl. Behav. Sci. 27 (2),

139 – 162.

Yan, A., 1993. Bargaining power, management control, and performance in international joint ventures: development and test of a negotiations model. Unpublished doctoral dissertation, The Pennsylvania State University.

Yan, A., 1998. Structural stability and reconfiguration of international joint ventures. J. Int. Bus. Stud. 29 (4),

773 – 796.

Yan, A., Gray, B., 1994. Bargaining power, management control, and performance in US – China joint ventures:

a comparative case study. Acad. Manage. J. 37 (6), 1478 – 1517.

Yan, A., Gray, B., 1995. Reconceptualizing the determinants and measurement of joint venture performance. Adv.

Global High Technol. Manage. 5B, 87 – 113.

Yan, A., Gray, B., 2001. Antecedents and effects of parent control in international joint ventures. J. Manage. Stud.

38 (3), 393 – 416.

Yan, A., Luo, Y., 2001. International Joint Ventures: Theory and Practice. M.E. Sharpe, New York.

Zaheer, A., Venkatraman, N., 1995. Relational governance as an interorganizational strategy: an empirical test of

the role of trust in economic exchange. Strategic Manage. J. 16, 373 – 392.

Zajac, E., Olsen, C.P., 1993. From transaction cost to transactional value analysis: implications for the study of

interorganizational strategies. J. Manage. Stud. 30 (1), 131 – 145.

�

Barbara Gray

Barbara Gray