Economic Comparison Between

Conventional and Disposables-Based

Technology for the Production

of Biopharmaceuticals

J. L. Novais, N. J. Titchener-Hooker, M. Hoare

The Advanced Centre for Biochemical Engineering, Department of

Biochemical Engineering, University College London, Torrington Place,

London WC1E 7JE, United Kingdom; telephone: +44 20 7679 3796; fax: +44

20 7383 2348; e-mail: nigelth@ucl.ac.uk

Received 27 December 2000; accepted 30 April 2001

Abstract: Time to market, cost effectiveness, and flexibility are key issues in today’s biopharmaceutical market.

Bioprocessing plants based on fully disposable, presterilized, and prevalidated components appear as an attractive alternative to conventional stainless steel plants, potentially allowing for shorter implementation times,

smaller initial investments, and increased flexibility.

To evaluate the economic case of such an alternative it

was necessary to develop an appropriate costing model

which allows an economic comparison between conventional and disposables-based engineering to be made.

The production of an antibody fragment from an E. coli

fermentation was used to provide a case study for both

routes. The conventional bioprocessing option was

costed through available models, which were then modified to account for the intrinsic differences observed in a

disposables-based option. The outcome of the analysis

indicates that the capital investment required for a disposables-based option is substantially reduced at less

than 60% of that for a conventional option. The disposables-based running costs were evaluated as being 70%

higher than those of the conventional equivalent. Despite

this higher value, the net present value (NPV) of the disposables-based plant is positive and within 25% of that

for the conventional plant.

Sensitivity analysis performed on key variables indicated the robustness of the economic analysis presented. In particular a 9-month reduction in time to market arising from the adoption of a disposables-based approach, results in a NPV which is identical to that of the

conventional option. Finally, the effect of any possible

loss in yield resulting from the use of disposables was

also examined. This had only a limited impact on the

NPV: for example, a 50% lower yield in the disposable

chromatography step results in a 10% reduction of the

disposable NPV. The results provide the necessary

framework for the economic comparison of disposables

and conventional bioprocessing technologies. © 2001

John Wiley & Sons, Inc. Biotechnol Bioeng 75: 143–153, 2001.

Keywords: disposable equipment; bioprocessing; process economics; time to market

Correspondence to: N. J. Titchener-Hooker

Contract grant sponsors: Biotechnology and Biological Sciences Research Council; Millipore; Kvaerner Process; Lonza Biologics; Hyclone;

Biotage; Portuguese Ministry of Science and Technology

© 2001 John Wiley & Sons, Inc.

INTRODUCTION

To be successful in today’s biopharmaceutical market it is

no longer enough to have a good technology portfolio, a

strong intellectual property position, and access to capital

(Gamerman and Mackler, 1994). Flexibility, cost effectiveness, and time to market are becoming the key issues with

which biopharmaceutical companies have to be concerned

(Basu et al., 1998; Burnett et al., 1991; Ernst et al., 1997;

Gamerman and Mackler, 1994; Hamers, 1993).

First, it is essential that biopharmaceutical development

and manufacturing facilities have increased flexibility. This

is dictated both by constant priority changes arising from

the generation of safety and clinical data in the development

phase (Basu et al., 1998) and by the need to allow for future

expansions. As a consequence of priority changes, the capability of multiproduct processing is gaining an increasing

interest although there are still complicated regulatory issues associated with potential crosscontamination (Hamers,

1993). The need to allow for future expansion requires careful decisions during the design of any facility. The problem

is that when such decisions are made early in the development process they are difficult to change later due to regulatory constraints (Basu et al., 1998; Ernst et al, 1997). On

the other hand, the delay of the decision to build brings

construction onto the critical path (Nicholson, 1998). Early

decision-making would be advantageous but will be associated with higher risk because there is less confidence in

the likelihood of success of the product (Burnett et al.,

1991). This is particularly critical for biopharmaceutical

products due to their high failure rates (Struck, 1994).

Second, the industry must operate under growing government- and market-enforced price controls and a need for

cost-benefit justification (Gamerman and Mackler, 1994)

which brings a demand for better cost-effectiveness. Additionally, there is less confidence on the part of the investors

and a lack of available capital which forces companies to

control their capital needs. Finally, it is essential to get into

the market as quickly as possible due to increasing competitiveness (Burnett et al., 1991) and to maximize revenue

�during patent life. To cut healthcare budgets generic drugs

are being favored and newly released drugs no longer command large premiums (Nicholson, 1998). Companies must

therefore move more quickly from discovery to patent, and

then to trials and efficient production. According to Basu et

al. (1998) delays in entering the market translate into millions of dollars of lost revenue.

In this article we explore the use of biopharmaceutical

plants based on disposable components as a means to overcome some of these pressures. In such a re-engineering

stainless steel vessels would be replaced by presterilized

disposable plastic containers requiring virtually no maintenance and incurring minimal cleaning costs. The same concept applies to the connections which can be replaced by

disposable plastic pipes. This option therefore has the advantage of switching capital costs to consumables costs as

required. It also allows for the better management of uncertainty in future process volumes. The disposable concept

can be extended throughout the production process. Separation processes such as cell harvesting and protein clarification and concentration can be achieved by tangential flow

filtration with disposable membranes. The final purification

steps can be accomplished in disposable prepacked chromatography columns or by batch adsorption in disposable plastic bags. Disposable technology also makes use of noninvasive pumps and valves, such as peristaltic pumps and

pinch valves. All the instrumentation is disposable or noninvasive and heat transfer can be achieved by disposable

heat-exchangers (Pearl and Christy, 2000).

The competitiveness of such plants is increased due to

minimization of the resultant cost of down-time for cleaning, sterilization, and corresponding validation procedures

as well as labor and operating costs associated with these

operations. The use of disposable equipment also allows for

quick changeover between products which is invaluable in

the clinical phases of development where often multiple

products are evaluated simultaneously.

A key factor determining the speed to market of disposables-based plants is associated with the decision of when to

build the manufacturing facility. The simpler construction

of disposables-based plants implies that shorter implementation times can be realized which allows for more detailed

process optimization before moving onto construction. Alternatively, these shorter construction times may allow for

earlier entry to market and at a lower risk due to the smaller

investment involved.

To determine the importance and interest of such a technological approach it is necessary to evaluate disposablesbased processes from an economic point of view and to

compare it with traditional bioprocessing methods. This is a

difficult task due to a lack of adequate costing models for

biopharmaceutical facilities. The few models currently

available have been originally developed for conventional

process engineering facilities (Peters and Timmerhaus,

1991; Sinnott, 1991). Some published case studies for bioprocesses do exist and can be used as a basis for costing

(Datar et al., 1993; Ernst et al., 1997). In addition, it is

144

important to consider process development issues such as

scale-up of the disposable option or transfer and scale-up to

a conventional option. Though this is not the subject of this

article it is recognized that in both cases it will be necessary

to carry out process studies using the disposable option in

such a way that product equivalence will be achieved.

In the present work therefore the main concern was to

establish a comparison between the two approaches rather

than to obtain absolute costing figures. The comparison was

made on the basis of the net present value (NPV), which

requires the calculation of the capital investment and of the

annual running costs. This article proposes a methodology

to cost disposables-based plants followed by an application

of this methodology to a particular case study.

METHODOLOGY

The initial methodology developed for the economic evaluation and comparison of the conventional and disposable

approaches to bioprocessing is intended to be as generic as

possible. This methodology was then applied to an E. coli

process, which is presented in the Results section.

For ease of comparison between process costs based on

conventional and disposable equipment, it is initially assumed that the two operate at the same yield throughout,

e.g., same biomass and product concentration in the fermentor or same flux rate in a microfilter. Comparable yields are

not likely to be achieved for a high cell density fermentation

but are probably achievable for mammalian cell culture;

flux rates are likely to be independent of the operating

mode. The costing is based on that for conventional equipment where the majority of information is available. Conversion factors are then used to assign the cost based on

disposable equipment.

Any difference in yield between conventional and disposable options requires an understanding of the total process. Factors affecting the yield in a fermentor will have a

different overall effect on the costing compared with factors

affecting the yield in the recovery and chromatographic

separation stages. For example, in the case of an intracellular product a reduction in fermentor cell density will not

affect the nutrient costs but will affect the fermentor size

and the load on the critical cell harvest step. The remainder

of the process should not be affected.

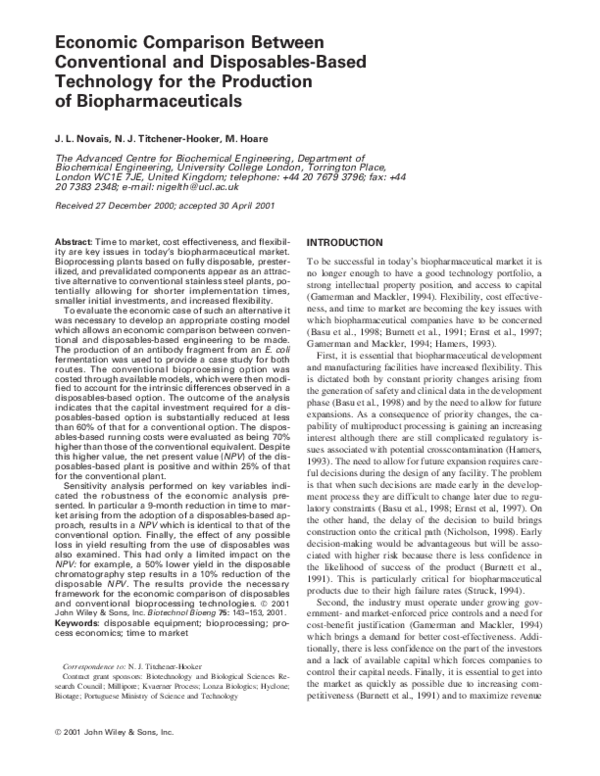

The objective of the following costing analysis is to allow

a comparison between conventional and disposable options

as indicated in Figure 1A and 1B respectively. The following sections will determine the routes towards capital and

operating costs and an overall analysis based on the Net

Present Value (NPV). A full description of the proposed

framework is given in Figure 1 based on the costing analysis

given in the following sections.

Many different scenarios may be possible for the comparison of the costs. In this article it is assumed that:

● A green-field site is used.

BIOTECHNOLOGY AND BIOENGINEERING, VOL. 75, NO. 2, OCTOBER 20, 2001

�used (Peters and Timmerhaus, 1991). The specific value for

such a factor applicable to bioprocessing plants is not easily

available from the literature but can be obtained from the

sum of the individual factors which constitute the fixed

capital investment.

The fixed capital investment for a conventional bioprocessing plant (FCIconv) is therefore given by:

S( D

10

FCIconv = LconvEconv = c

fi

Econv

(1)

i=1

Figure 1. Diagram of the methodology followed for the calculation of the

net present value (NPV) of (A) conventional, and (B) disposables-based

routes of bioprocessing. (A) The costing route is determined by a design

analysis of the bioprocess leading to a sizing of the equipment and specification of process materials’ requirements. This leads to an evaluation of

the equipment and hence, fixed-capital investment and operating costs,

which along with the schedule of project development yield the NPV for

the project. (B) The costing route for the disposable option uses the conventional equivalent initially assuming operation at the same process yields

as the conventional option. The fixed capital investment is determined by

a series of factors relating the conventional and disposable options [Eq.

(2)]. The operating costs are determined as for the conventional option with

appropriate factors that reflect the increased costs due to disposable items.

The effect of a difference of yield between the conventional and disposable

options is accomodated by a resizing of the conventional equivalent followed by a re-evaluation of the fixed capital investment. For operating

costs the effect of a change of yield requires that the conversion factors

associated with the running costs are re-evaluated to take into account the

change in materials’ costs.

● The plant is used throughout the year as a single product

facility.

● In the disposable option all equipment parts that are in

direct contact with the process streams will be disposable

and, where necessary, presterilized (e.g., with g-radiation).

● In the disposable option all media and buffers are purchased preformulated and sterile ready for use.

The time to build, commission, and validate each affect time

to market and are therefore crucial factors in the comparison

between the conventional and disposable options. For the

NPV calculations an identical project schedule for the two

options was considered appropriate (Fig. 1). The additional

competitive advantage of being quicker to market that may

be brought by a disposables-based approach will be discussed later in the article.

Capital Investment

In an approach initially proposed by Lang (1948) for chemical engineering plants, the fixed capital investment (FCI)

can be calculated by multiplying the equipment cost by a

factor, which depends on the type of process plant being

where Lconv is a “Lang” factor for conventional bioprocessing plants and Econv is the cost of the process and utilities

equipment. The factors f1 to f10 relate to Econv to give the

cost of process and utilities equipment (f1, f1 4 1), pipework and installation ( f2), process control ( f3), instrumentation ( f4), electrical power ( f5), building ( f6), detail engineering ( f7), construction and site management ( f8), commissioning ( f9), and validation ( f10). A contingency factor,

c, may also be included.

The fixed capital investment for a bioprocessing plant

based on disposable equipment (FCIdisp) may be estimated

from the cost of the installed equipment and utilities for a

conventional plant as follows:

S( D

10

FCIdisp = LdispEconv = c8

fifi8

Econv

(2)

i=1

where Ldisp is a “Lang” factor for disposable bioprocessing

plants, f 18 to f 810 are factors which translate the cost of the

individual elements which constitute the capital investment

of the conventional plant into the cost of elements for the

disposable option. c8 is the relevant contingency factor.

The factors f 81 to f 10

8 for the conversion from conventional

to disposable can be estimated from the following assumptions:

● Equipment and utilities ( f 18 ): In a plant using disposable process equipment the capital investment costs for

process equipment are decreased. Also, the disposable

option would need reduced or even no clean-in-place and

steam-in-place capabilities. As a consequence, the cost of

utilities equipment is substantially reduced as only features such as cooling water, chilled water, process air,

and vacuum will be required if all of the process can be

turned over to disposable operation.

● Pipework and installation ( f 82): The capital costs associated with pipework are decreased in a disposable option

because the cost of the disposable tubing becomes an

operating cost. Connections to utilities which do not

come into contact with the product stream would normally be considered as nondisposable. Equipment installation costs are also decreased due to the reduction in

fixed equipment.

● Process control ( f 38 ):Process control costs are likely to

remain unchanged although in the disposable case there

may well be a move toward more manual operation in the

interest of speed to market. Conversely, the need for

NOVAIS ET AL.: ECONOMIC EVALUATION OF DISPOSABLES-BASED BIOPROCESSING

145

�●

●

●

●

●

●

●

more noninvasive monitoring may lead to greater costs in

computing for data interpretation for control purposes.

Instrumentation ( f 48 ): Instrumentation capital costs are

reduced because some of the instruments may be disposable (for example, thermocouples) and therefore appear

as a running cost. Alternatively, instrumentation may be

redesigned to be noninvasive (e.g., UV-detectors) and

hence, lead to no change in capital cost. Other instrumentation such as gas mass spectrometers are not in contact

with the process material and also do not lead to a change

in capital cost, as they will be needed for both modes of

operation. Where disposable alternatives to high-cost invasive instrumentation (e.g., pH meters) are not available

then either separate validation for turn around (e.g.,

cleaning and recalibration) must be put in place or recourse is needed to data interpretation from actual available measurements (e.g., cell density by optical window,

exit gas analysis, etc). Again, in such a case it is assumed

the capital cost is not affected.

Electrical power ( f 85): Assuming power consumption

and capital costs are related, it is likely that electrical

power capital costs are probably independent of whether

conventional or disposable equipment is used. Alternative methods of mixing for a disposable process are likely

to have similar power requirements to those for a conventional process. Conversely, a reduction in size of facility could lead to a significant decrease in air conditioning costs because this will be related to the volume of

the facility.

Building ( f 86): The variation of the cost of the building

can be estimated by establishing the layout of a typical

coventional plant and predicting the changes of the floor

area of each section based on the particular needs of a

disposable plant. If a system with wheel-in/wheel-out

equipment is considered, it can be assumed that processing areas can be reduced in size but that larger, low-cost

storage areas will be needed. Also, utilities’ areas will be

smaller and media preparation and equipment wash areas

might disappear. The effect of changes in the function of

the areas and consideration of their differential cost

should lead to a reduction in building costs when using a

process based on disposable equipment.

Detail engineering ( f 78 ): The costs associated with detail

engineering are expected to be reduced for the disposables option due to the less-refined construction needed.

Construction and site management ( f 88 ): Construction

and site management costs should be decreased due to the

smaller building area required for the disposable option.

Commissioning ( f 89): The commissioning costs of the

disposables-based plant are considered to remain unaltered when compared to those of a conventional plant.

Validation ( f 810): The validation of a disposables-based

vs. a conventional process will differ due to process

qualification (PQ):

—Reduced or no cost of validation for the cleaning,

sterilization, and turnaround of process equipment

when using disposable equipment. This argument is

146

already used in the qualification of use of disposable

containers. The challenge and hence costs of cleaning

validation for more complex equipment such as membranes also bears on this factor.

—The cost of validation of linkages between equipment (sterile welding vs. conventional sealed pipe

joints) is likely to remain the same.

With estimates for the conventional plant equipment costs

(Econv) and for the factors fi and f 8i it is possible to calculate

Lconv, Ldisp, FCIconv, and FCIdisp. We use estimates of factors f 81 to f 810 to demonstrate how the translation from a

conventional to a disposable option may be evaluated.

Running Costs

A model based on a bacterial fermentation process was

derived from the breakdown of the running costs observed

by Datar et al. (1993) for their particular case study. The

breakdown was reduced down to five categories (labor, materials, utilities, depreciation, and other costs) and adapted

so as to exclude general expenses such as R&D and sales

expenses from the overall running costs for simplification

purposes. This results in:

5

RCconv = RCconv

(x

i

(3)

i=1

where RCconv is the running cost of the conventional plant,

x1 to x5 are the fractions of the running cost which give the

cost of its individual components: labor (x1), materials (x2),

utilities (x3), depreciation (x4), and other costs (x5). Other

costs include patents and royalties, waste treatment, and

indirect manufacturing expenses.

The costs of the disposable option can be predicted from

considerations on how each category of costs varies when

compared to the equivalent conventional option. It is expected that materials (raw materials including disposable

equipment) will increase significantly and that utilities costs

and depreciation costs will be reduced, the latter due to the

lower capital investment involved. Hence, Eq. (3) becomes:

5

RCdisp = RCconv

(xy

i i

(4)

i=1

where RCdisp is the running cost of the conventional plant

and y1 to y5 are factors which convert the individual conventional running cost fractions into disposables-based

ones.

The factors y1 to y5 for the conversion from conventional

to disposable can be estimated from the following assumptions:

● Labor (y1): Costs associated with cleaning and sterilization will be decreased but there will be increased costs

due to the need for assembling/disassembling of components, as well as the operation of sterile welding systems.

BIOTECHNOLOGY AND BIOENGINEERING, VOL. 75, NO. 2, OCTOBER 20, 2001

�●

●

●

●

Labor costs associated with in-house media and buffer

preparation will be decreased.

Materials (y2): Costs associated with raw materials will

be increased, as these will be bought as preformulated

media and buffers. These cost items are higher so as to

include the expense of the containers and the operating

costs incurred by the supplier for the preparation and

sterilization of the media and buffers. The cost of disposable items (e.g., membranes, vessels, chromatographic

media, pipework, etc) will become a major factor.

Utilities (y3): Costs associated with steam and cleaning

requirements should be reduced.

Depreciation (y4): This cost should be reduced as it is

only associated with the process plant capital investment,

which is reduced in a disposables’ option.

Other (patents, royalties, waste treatment, etc) (y5):

This cost is possibly unaffected—with, for example, the

high effluent treatment costs for cleaning agents associated with the conventional option being offset by the

increased costs for solid-waste treatment of the disposable option.

Net Present Value

The net present value (or net present worth) gives an indication of the profitability of a project. The generic equation

for its calculation is (adapted from Peters and Timmerhaus,

1991):

m+t

NPV =

(

n=0

CFn − FCIn

~1 + r!n

Sn − RCn − FCIn

m+t

=

(

~1 + r!n

n=0

m−1

(

n=0

−RCn − FCIn

~1 + r!

n

m+t

+

(

n=m

Sn − RCn − FCIn

~1 + r!n

Effect of Process Performance

Although the disposables-based process is intended to be

identical in performance and characteristics to its conventional counterpart, it may well be that some unit operations

have to be altered to be operated in a fully disposable fashion. Such changes may affect negatively the yield of these

particular steps and consequently either more time has to be

spent in process development or the fermentation volumes

may have to be increased so that the final product mass is

the same as in the conventional alternative. This will also

impact the design specifications of subsequent operations.

For example, the membrane area needed for cell harvesting

has to be increased to cope with a higher fermentation volume. The ultimate effect of such differences is a lowered

NPV for the disposable plant, which has to be quantified and

compared to that of the conventional plant. This is done

according to the procedure detailed in Figure 1B. As discussed earlier, the evaluation of the impact of a change of

yield on the overall process is a complex one with each

stage having a different impact on the overall process according to product location and subsequent recovery and

purification stages. Hence, the impact of the performance of

different stages has to be assessed specifically for that stage.

RESULTS

(5)

Case Study

where NPV is the net present value of the project, r is the

discount rate (or annual interest rate of return), CFn is the

net cash flow in year n, FCIn is the fixed capital investment

in year n, t is the life of the project (in years), m is the year

of entry to market, Sn is the value of sales in year n and RCn

is the value of the running costs in year n. For n < m, i.e.,

before entry to market, Sn will be zero and Eq. (5) becomes:

NPV =

linear least squares and interpolation can be used to deal

with fractions of years gained in time to market.

(6)

with the first part of the equation dealing with the period

before manufacture commences and the second part with

the period thereafter.

Effect of Time to Market

Considering that opting for a disposables-based process

may allow for earlier entry to market it is interesting to

evaluate the impact this may have on the NPV. This is

achieved using Eq. (6) but considering that the start of

manufacture and sales occurs earlier than year m. (This does

assume that the life-span of the project (t) is unchanged,

which will result in an underestimate of the benefits.) Non-

The case study presents a comparison between a conventional bioprocessing plant and its disposable equivalent and

is based upon the production of an antibody fragment using

a recombinant E. coli at a 300-L working-volume fermentation scale of operation with the antibody expressed in the

periplasmic space. Given that bioprocessing bags are currently available up to 1000-L scale (HyClone Europe catalogue), operation at 300 L should not pose any additional

major obstacle. The cells are to be harvested, lysed for

protein release, followed by removal of cell debris/empty

cells and a first chromatographic or adsorption/desorption

separation stage either for product capture (preferably) or

for contaminant capture. A detailed process diagram and a

complete mass balance were developed and used as the

basis for equipment sizing. The process scheme is shown in

Figure 2A using conventional equipment and in Figure 2B

using equipment configured for use in a disposable fashion.

The resulting equipment list was used to establish the capital investment for each option [Eqs. (1) and (2)]. From the

mass balance it was also possible to estimate raw materials

and disposable equipment consumption which were used in

the calculation of the running costs.

It was assumed that the disposables-based plant had an

identical process sequence and the same yield per unit op-

NOVAIS ET AL.: ECONOMIC EVALUATION OF DISPOSABLES-BASED BIOPROCESSING

147

�Figure 2. Process diagram of the case study process: E. coli production of an antibody fragment. (A) conventional route, and (B) disposables-based route.

In the latter case, the process vessels are disposable bioprocessing containers and the fermentation is achieved with a plunging-jet design.

eration as the conventional plant. Both conventional and

disposables-based options were assumed to operate 48

batches/year for a project life of 8 years. Hence, no account

was taken of the potential for some rapid turnaround of a

process batch when using the disposables option. It was

assumed that the decision to build the conventional manufacturing plant has to be taken by Phase III clinical trials,

that is approximately 3 years before entry to market. A

similar constraint was applied for the disposables option.

This assumption may result in an underestimate of the benefits of disposables option which, through having a reduced

capital expenditure, may enable such financially risky decisions (failure rates being as high as 1 in 3 at early clinical

stages; Struck, 1994) to be made somewhat earlier.

Capital Investment

Based on bioprocessing plant data (A. Sinclair, Biopharm

Services, Amersham, Bucks, UK; D. Doyle, Kvaerner Pro148

cess, Portsmouth, UK, personal communication) it is possible to assign values to the fixed capital investment factors

( f1 to f10) in Eq. (1). It is also possible to estimate values for

the factors in Eq. (2) that translate conventional into disposables ( f81 to f 810) from the assumptions described in the

methodology section. The factor f81 was calculated considering that utilities account for approximately half of the total

equipment costs and that they are reduced by a factor of

60% because there is no need for clean steam production,

etc. (This factor also assumes that all the process equipment

is disposable.) The values for the conventional and disposable factors are summarized in Table I and enable the calculation of the two “Lang” factors. The “Lang” factor for

the conventional plant, Lconv, evaluated at 8.1 is close to the

range commonly observed for biopharmaceutical plants (6

to 8, D.Doyle, Kvaerner Process, Portsmouth, UK, personal

communication). A “Lang” factor is obtained for the disposable plant, Ldisp 4 4.7 based on the equipment cost for

a conventional option.

BIOTECHNOLOGY AND BIOENGINEERING, VOL. 75, NO. 2, OCTOBER 20, 2001

�Table I. Capital investment factors for conventional ( fi) and disposablesbased ( fi f 8i ) bioprocessing plants and corresponding “Lang” factors.

Description

1

2

3

4

5

6

7

8

9

10

Equipment

(incl. utilities)

Pipework

and installation

Process control

Instrumentation

Electrical power

Building works

Detail Engineering

Construction

and site management

Commissioning

Validation

Contingency factor (c)

“Lang” Factor

Conventional

fi

Disposable

f8i

1

0.2

0.9

0.33

0.37

0.6

0.24

1.66

0.77

0.4

1

0.66

1

0.8

0.5

0.75

0.07

1.06

1

0.5

1.15

1.15

Lconv 4 8.13

Ldisp 4 4.73

Note: The conventional plant factors ( fi) are derived from standard

figures for conventional bioprocessing plants (A. Sinclar, Biopharm Services, Amersham, Bucks, UK; D. Doyle, Kvaerner Process, Portsmouth,

UK, personal communication). The factors for the disposable translation

( f i8) are based on assumptions derived from the definition of disposable

manufacture (presented in the Methodology). The Lang factors are defined

10

10

as: Lconv = c(i=1

fi and Ldisp = c(i=1

fi f 8i .

The values of capital investment for both options were

obtained from Eqs. (1) and (2) with the conventional equipment costs based on the case study process and from the

values of Lconv and Ldisp shown in Table I. Hence, the conventional capital investment was evaluated at $19.2M as

opposed to $11.2M for the disposable option.

Running Costs

Table II shows the materials costs calculated for both options based on the process requirements. The cost of the raw

materials in the conventional plant was estimated from laboratory supplies catalogs (i.e., Sigma Biochemicals and Reagents for Life Science Research, 1998; BDH Laboratory

Supplies Catalogue, 1998) costs for the largest available

quantities to which a discount factor of 3 was applied. For

Table II. Annual materials’ costs estimates for both conventional and

disposables-based routes.

Materials Costs ($k/year)

Conventional

Disposable

Raw materials

Membranes

Matrices (IEX)

Other disposable equipment

Total

36

58

16

0

110

138

1166

319

191

1814

Note: The cost of each item was obtained from a mass balance to the

process and from the process flowsheet. The item “Other disposable equipment” includes bioprocessing containers and flexible pipes. It can be noted

that the total cost of materials requirements of a disposables-based plant is

approximately 16-fold higher than that of an equivalent conventional bioprocessing plant.

the disposable plant it was assumed that the media and the

buffers are bought preprepared supplied in sterile containers

and cost on average $4/L (range of costs suggested by HyClone Europe). The running costs of the membranes and

matrices in the conventional plant were calculated from

membranes and chromatography manufacturers catalogs

[Millipore (UK) Ltd. and Amersham Pharmacia Biotech]

taking a conservative estimate that these are used 20 times

before being replaced. In a disposable plant both membranes and ion-exchange matrices are disposed of after each

batch. The item “other disposable equipment” includes all

other equipment not specified above, such as bioprocessing

containers and flexible pipes (HyClone Europe Price List).

This item is close to zero in a conventional plant. It was

assumed that a disposable plant makes use of containers of

the same volume as the stainless steel containers in the

conventional plant and that it needs approximately 10 m of

flexible tubing for each unit operation.

The factors x1 to x5 [Eq. (3), Table III] were calculated

from the cost breakdown presented by Datar et al. (1993).

The cost of depreciation is estimated using the capital investment (FCIconv) and a working life of 8 years for the

plant. From there it is possible to calculate the cost of the

other individual items of the running costs of the conventional plant through Eq. (3). The running costs of the disposables-based option were estimated through Eq. (4). As a

first approach it was assumed that the disposables-based

plant has the same staff requirements as its conventional

equivalent (y1 4 1). From Table II it can be noted that there

is a 16-fold increase in the running costs associated with all

materials and consumables in a disposables-based approach,

hence y24 16. In a disposable plant the utilities running

cost is expected to be halved due to the absence of operations such as clean-in-place (CIP) and steam-in-place (SIP)

(y3 4 0.5). Depreciation costs are reduced as a result of the

lower capital investment involved as shown in Table I, that

is y4 4 0.6 and other costs are likely to remain unchanged

(y5 4 1). The resultant comparison for the running costs for

conventional as opposed to disposable operation is given in

Figure 3, the running costs of a disposable biopharmaceuTable III. Running costs factors derived from a cost distribution presented by Datar et al. (1993) for bacterial process.

1

2

3

4

5

Item

xi

yi

Labor costs

Materials

Utilities

Depreciation

Other

0.14

0.06

0.14

0.19

0.47

1

16

0.5

0.6

1

Note: The conventional factors (xi) were obtained from the percentages

presented by Datar et al. (1993) for their case study after excluding general

expenses from the overall running costs. the item “Other” includes costs

such as patents and royalties, waste, indirect manufacturing expenses, etc.

The disposable factors (yi) were predicted considering that staff costs remain the same, raw materials including disposable equipment increase

16-fold (based on the calculations in Table II), utilities costs are reduced by

half, and other costs remain unchanged. Depreciation costs are reduced as

a direct result of the lower capital investment involved.

NOVAIS ET AL.: ECONOMIC EVALUATION OF DISPOSABLES-BASED BIOPROCESSING

149

�Table IV.

Economic analysis results summary.

Option

Convention

Disposable

FCI ($M)

RC ($M/year)

NPV ($M)

19.2

12.8

102.6

11.2

22.0

75.8

Note: The fixed capital investment was obtained from the total cost of

conventional equipment and from the “Lang” factors in Table I. The running costs are as presented in Figure 3 and the fixed capital investment

(FCI). The net present value (NPV) was calculated according to Eq. (7)

assuming annual sales of the Fab8 antibody fragment to be 5 times the

conventional running costs (Coopers and Lybrand, 1997. Pharmaceuticals:

Creating value by transforming the cost base, company publication).

Figure 3. Breakdown of the running costs of the conventional and disposable processes. The conventional breakdown was based on a cost distribution presented by Datar et al. (1993) for a bacterial process and the

disposable individual running costs were calculated with the use of the

factors presented in Table III and from the conventional capital investment

value presented in Table IV. The item “Other” includes costs such as

patents and royalties, waste, indirect manufacturing expenses, etc.

tical plant being 1.7 times higher than the equivalent conventional costs.

A second model originally developed for conventional

engineering processes (Sinnott, 1991) was also used for the

calculation of the running costs (analysis not presented).

According to this model the overall running costs associated

with a disposables option would differ by a factor of 0.9 to

those of a conventional option compared with a factor of 1.7

given above. This is because the second model places more

emphasis on costs such as depreciation and utilities, which

are reduced in a disposables approach, rather than on raw

materials and consumables.

Net Present Value

To compare the disposables-based approach with the conventional one the respective NPV was calculated according

to Eq. (6). In this equation it was considered that the investment was completed in year zero for both approaches.

Both plants were considered to start operating at half capacity in year 1 (RC1 4 1/2 RC), achieving full capacity in

year 2. Sales commence in year 3 (m 4 3, S1 4 S2 4 0).

Taking the project life span as 8 years (t 4 8) as specified

in the description of the case study and the discount rate as

r 4 0.2, Eq. (6) becomes:

2

NPV = FCI +

(

n=1

− RCn

+

~1 + 0.2!n

10

Sn − RCn

( ~1 + 0.2!

n=3

n

To evaluate the reliability of the disposable cost models,

sensitivity analysis was carried out for relevant variables in

the disposables approach. The parameter chosen for the

comparison was the ratio of disposable NPV over conventional NPV, which is >1 when the disposables-based option

is financially the most attractive.

The variables studied included capital investment (and

consequently also the “Lang” factor for disposable bioprocessing plants, Ldisp), staff costs and materials costs with the

aim of evaluating whether the assumptions made for the

definition of the disposable cost models affect the final

comparison. Figure 4 shows the impact on the NPV ratio of

a variation of −25% made to each of these disposable plant

variables. (Note when the capital investment is varied, the

depreciation costs are also affected as they are, by definition, directly related to the capital investment.) It can be

seen that these three variables have only a slight impact on

the NPV ratio.

A further effect that may influence the way the two processing options compare is the resulting time to market

achievable. Figure 4 also shows how a reduction of 9

months in entry to market with the disposables-based approach can affect significantly the NPV ratio. For example,

(7)

The net present value was obtained having set the annual

sales for each case as 5 times the running costs of the

conventional plant (Coopers and Lybrand, 1997. Pharmaceuticals: Creating value by transforming the cost base,

company publication). The results are summarized in Table IV.

150

Sensitivity Analysis

Figure 4. Sensitivity analysis showing the effect on the NPV of a 25%

reduction on crucial cost variables. The results are presented as a ratio

(NPVdisp/NPVconv) and were obtained by altering the following variables in

the disposable case, leaving the conventional case fixed: fixed capital

investment, staff costs, materials costs and time to market.

BIOTECHNOLOGY AND BIOENGINEERING, VOL. 75, NO. 2, OCTOBER 20, 2001

�the NPV ratio is 0.74 when the time to market is the same

but increases to 1.00 if disposables allows for a 9 months

earlier entry to market.

Another important aspect that cannot be overlooked is

whether a disposables-based approach may affect the overall yield of the process. The unit operations that may be

affected by a switch to disposables operation are the fermentation, where a stirred tank has to be replaced by a

plunging jet (Zaidi et al., 1991) or an airlift reactor, and the

chromatography step, where the column may be replaced by

a column prepacked with cheaper media or by multiple

batch adsorption/desorption steps. The microfiltration, and

periplasmic release steps are not expected to be affected as

they remain intrinsically the same as in the conventional

process.

The performance of a disposable fermentor may be lower

when compared to a conventional fermentor as a result of

different factors such as oxygen-transfer difficulties. Work

carried out in this research group (Baker et al., to be published) with a disposable fermentation plunging-jet design

indicated that oxygen transfer might be a factor affecting the

yield. The yield loss may be due to achieving a lower level

of biomass or through the cells being intrinsically less productive (lower expression levels). Additionally, in the particular case of a periplasmically expressed product some

material may be released into the fermentation broth during

the operation of a disposable fermentation as is observed in

stirred-tank fermentors (Gill et al., 1998). The effect on the

disposable plant NPV of a reduction of 25% in the yield of

antibody fragment was studied. It was considered that this

reduction in yield could be effected in two different ways:

(a) as a 25% reduction in the biomass, and (b) as a 25% fall

in the expression level of the cells, but with an overall

identical biomass concentration (Fig. 5). Alternative “b”

also considers the case where there is a reduction of the

amount of product found in the periplasmic space with an

equivalent increase in that found in the extracellular me-

dium. The NPV of each alternative was calculated as described in the methodology section considering that the final

product mass obtained was the same as in the base case. A

25% yield loss in terms of biomass results in a slight drop

in the achievable NPV to 91% of that of the base case, while

a 25% lower expression level has a higher impact on the

NPV, decreasing it to 83% of that of the base case (Fig. 5).

Each of these effects may also be examined more closely.

Sensitivity analysis was carried out for a range of fermentation yields of 50% to 100% of the conventional base case,

combined with sensitivity analysis for the cost of the materials (raw materials and disposable equipment) and is

shown in Figure 6A and 6B. Figure 6A illustrates the case

where the yield loss is associated with less biomass while

Figure 6B analyzes the consequences of yield loss due to

less product being produced by the cells. A 50% drop in

biomass yield results in a 30% drop in the NPV. This is

more accentuated in the case where the yield loss arises

from a lower expression level, resulting in a 60% decrease

of the NPV. The cost of the materials was examined as it is

Figure 5. Impact of lower fermentation performance effects on the NPV

of the disposable option. It was considered that the reduction in yield could

be effected in two different ways: as a 25% reduction in the biomass (lower

biomass) or as a 25% fall in the expression level of the cells, but with an

overall same biomass concentration (lower expression). The results are

presented as % of the NPV of the base case, that is a disposables-based

plant with same yield as a conventional plant.

Figure 6. Combined sensitivity analysis on the disposable plant NPV for

fermentation yield and cost of materials. The fermentation yield was varied

from 50% to 100% of the yield obtainable with the conventional plant. The

reduction in the fermentation yield was considered to be a result of (a)

lower biomass obtainable, and (b) lower expression level of the cells. A

reduction in the cost of the materials from 0 to 50% allowed the impact on

the NPV of the disposable plant to be investigated.

NOVAIS ET AL.: ECONOMIC EVALUATION OF DISPOSABLES-BASED BIOPROCESSING

151

�expected that it will be decreased once a market for disposable equipment has been established. In both cases, a 50%

saving in materials costs compensates for the loss in yield,

bringing the NPV up to 112% (Fig. 6A) and 96% (Fig. 6B)

of that of the base case. The final source of process yield

variation considered in this study was that due to a lower

yield in the disposables chromatography format. This may

be thought to arise as a consequence of less-specific binding

resulting in product loss in the wash step. Alternatively, a

reduced yield might also be due to a lower capacity of the

matrix for the product. The first case requires the use overall

of larger process volumes, while the second case results in

the need for higher volumes of matrix and of chromatography buffers. The second scenario was analyzed here. Figure

7 shows the results of a sensitivity analysis performed for a

reduction in the chromatography yield in combination with

a reduction in the cost of the materials. This is a very likely

case because a choice of a matrix with a lower capacity

would most certainly be driven only by economic considerations. The NPV decrease is small at only 10% when the

chromatography yield is 50% lower and this can be compensated for by a 25% saving in materials costs, for which

case the NPV would be 107% of that of the base case.

DISCUSSION AND CONCLUSIONS

The objective of this work was the economic modeling of a

fully disposable bioprocessing plant. This was achieved using conventional models and assumptions derived from the

definition of disposables-based bioprocessing.

Although the NPV values indicate the conventional option to be the most attractive ($76M for disposables and

$103M for conventional), the difference at only 25% is

probably sufficiently close to make disposables a viable

alternative, especially when considering the other advantages of disposable plants outlined in the Introduction.

Figure 7. Combined sensitivity analysis on the disposable plant NPV for

chromatography yield and cost of materials. The yield of the chromatography step was varied from 50% to 100% of the yield obtainable with a

conventional chromatography column. Reduction in yield was considered

to be a result of a lower capacity of the disposable matrix for the product.

A reduction in the cost of the materials from 0 to 50% allowed the impact

on the NPV of the disposable plant to be investigated.

152

It has to be noted, however, that the use of a conventional

process engineering model for the calculation of the running

costs (analysis not shown) indicated disposable plants as the

more attractive option, with a higher NPV. This result is

contrary to what could be intuitively predicted from the

definition of a disposables-based plant where the increase of

the variable associated to disposable equipment would be

expected to have a higher impact on the NPV. For this

reason, we considered the model presented in this article for

estimating conventional-based process costs as more appropriate to describe a biochemical engineering process. This

does, however, show how critical it is to identify an appropriate running costs model, which is a common problem

found in biotech costing studies.

It was also crucial to perform sensitivity analysis on the

assumptions made to develop the disposable models to

evaluate how much impact they would have on the overall

model if they were invalid. The sensitivity analysis done for

the case study (Fig. 4) shows that the overall disposable

model is not very sensitive to the critical variables. This

means that the estimation of these disposable values will not

affect crucially the conclusions of any economic comparison.

Turning now to consider the differences between the two

modes of processing, it is clear that staff costs have a small

effect on the way the conventional and the disposable options compare. This means that even if the staff requirements of a disposable plant are less than those of a conventional plant that would only result in a slight increase of the

NPV ratio. A decrease of 25% in the capital investment

would result in a variation of less than 5% on the NPV ratio,

showing insensitivity to this variable. This finding provides

more confidence in the “Lang” factor used for the disposables-based option (Ldisp). Materials’ costs are shown to be

more influential but their impact on the NPV ratio is still

less than 10% achieved by a 25% reduction in materials

costs. It can be concluded from Figure 4 that the costing

model is not strongly dependent on the assumptions made

for the disposables plant and that it is consequently reliable

to cost this bioprocessing option.

The disposable “Lang” factor (Ldisp) developed in this

article is perceived as a useful variable for the future economic evaluation of disposable bioprocessing plants. Its

value (60% of Lconv) shows the strong reduction in the capital investment achievable by a disposable approach. This

results in increased flexibility for the disposable plants because changes in the process or the product result in less

financial loss, which is of great interest for start-up companies. It also allows for an earlier decision to build which

may result in earlier entry to market. This effect benefits

strongly the disposables option because a reduction in time

to market has a high impact on the NPV ratio, as shown in

the results of the sensitivity analysis and depicted in Figure

4. The increased flexibility also arises from the concept of

“pay as you need,” due to the transfer of capital costs onto

running costs, making it less damaging when a product fails

BIOTECHNOLOGY AND BIOENGINEERING, VOL. 75, NO. 2, OCTOBER 20, 2001

�in clinical trials and advantageous given the current industry

trend of ever shorter project lives.

A final difficulty encountered in the analysis of disposable bioprocessing is to establish the degree of similarity

between disposables-based plants and conventional designs.

The fermentation step is an example of how the different

engineering features of a disposable plant can have a detrimental impact on product yield. Although the impact on

yield may happen in different ways, an analysis of the sensitivity in Figure 5 shows that this affects the obtainable

NPV by less than 20%.

Figures 6A and 7 show that the reduction in the achievable yield given by a disposables-based option and associated with lower levels of biomass production in the fermentation and with reduced chromatographic performance has

only a limited impact on the NPV that is realized. By contrast the loss of yield due to less-productive cells has a

dramatic impact on the NPV (Fig. 6B). This is, however, a

less likely scenario.

The analysis shows that any fall in NPV can easily be

overcome when disposable equipment producers start responding with higher production scales and hence, lower

prices to an increasing demand for their products. Effectively, a 50% reduction in the yield of the fermentation can

be compensated for by a 50% reduction in the cost of the

materials (Figs. 6A and 6B). This is even more striking in

the case of the chromatography (Fig. 7) where even a 50%

loss in yield can be overcome by a saving of 25% in the

materials costs, a margin that appears highly probable as the

disposables approach starts to gain acceptance.

Other questions that could be asked include: Can the

number of batches achieved per year in a disposable plant

be improved because there is no downtime for CIP and SIP?

Does a disposables-based process effectively allow for

quicker entry to market? These questions will be addressed

in a future article.

In conclusion, a disposables-based plant with the same features as its conventional equivalent is economically and conceptually attractive as it may be of easier and quicker implementation with a comparable overall investment required.

This work is part of an Innovative Manufacturing Initiative (IMI)

project entitled “Bioprocessing With Disposables To Cut costs

and Increase Process Efficiency for Biopharmaceuticals” funded

by the Biotechnology and Biological Sciences Research Council.

The support of Millipore, Kvaerner Process, Lonza Biologics,

Hyclone and Biotage is gratefully acknowledged. Joana L.

Novais is supported through the Praxis XXI programme of the

Portuguese Ministry of Science and Technology.

NOMENCLATURE

c

CF

Econv

contingency factor

annual cash flow, in $

equipment costs (conventional plant), in $

fi

f i8

FCI

L

m

n

NPV

r

RC

S

t

xi

yi

conventional plant factors for calculation of individual FCI

items

factors which translate conventional plant FCI items into disposable ones

fixed capital investment, in $

“Lang” factor

year of entry to market

project year

net present value, in $

discount rate

running costs, in $

value of annual sales, in $

project life, in years

fractions of conventional running cost

conversion factors for calculation of fractions of disposables

running cost

Subscripts

conv

disp

n

refers to the conventional plant

refers to the disposable plant

refers to year n

References

Basu PK, Quaadgras J, Mack RA, Noren AR. 1998. Achieve the right

balance in pharmaceutical pilot plants. Chem Eng Prog 94:67–74.

Burnett MB, Santamarina VG, Omstead DR. 1991. Design of a multipurpose biotech pilot and production facility. Ann NY Acad Sci 646:

357–366.

Datar RV, Cartwright T, Rosen C-G. 1993. Process economics of animal

cell and bacterial fermentations: A case study of tissue plasminogen

activator. Bio/technology 11:349–357.

Ernst S, Garro OA, Winkler S, Venkataraman G, Langer R, Cooney CL,

Sasisekharan R. 1997. Process simulation for recombinant protein production: Cost estimation and sensitivity analysis for Heparinase I expressed in Escherichia coli. Biotechnol Bioeng 53:575–582.

Gamerman GE, Mackler BF. 1994. Winning in today’s biopharmaceutical

marketplace. Chem Tech 24:37–41.

Gill A, Bracewell DG, Maule CH, Lowe PA, Hoare M. 1998. Bioprocess

monitoring: An optical biosensor for rapid bioproduct analysis. J Biotechnol 65:69–80.

Hamers MN. 1993. Multiuse biopharmaceutical manufacturing. Bio/

technology 11:561–570.

Lang HJ. 1948. Simplified approach to preliminary cost estimates. Chem

Engng 55:112–113.

Nicholson I. 1998. Outsourcing manufacturing: A strategic rationale. Paper

presented at the Biopharm Europe Symposium, October, 1998.

Pearl SR, Christy CD. 2000. Heat exchange apparatus. U.S. Patent

6,131,649.

Peters MS, Timmerhaus KD. 1991. Plant design and economics for chemical engineers. New York: McGraw Hill. 910 p.

Sinnott RK. 1991. Chemical engineering, Volume 6: An introduction to

chemical engineering design. Coulson JM, Richardson JF, editors.

Oxford: Pergamon Press. 838 p.

Struck MM. 1994. Biopharmaceutical R&D success rates and development

times. Bio/technology 12:674–677.

Zaidi A, Ghosh P, Schumpe A, Deckwer WD. 1991. Xanthan production

in a plunging jet reactor. Appl Microbiol Biotechnol 35:330–333.

NOVAIS ET AL.: ECONOMIC EVALUATION OF DISPOSABLES-BASED BIOPROCESSING

153

�

Nigel Titchener-hooker

Nigel Titchener-hooker