P2 41 2 42 Solutions

P2 41 2 42 Solutions

Download as pdf or txt

At a glance

Powered by AI

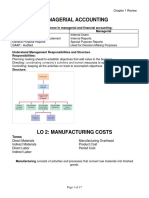

The document discusses cost accounting concepts including the income statement, schedule of cost of goods manufactured, prime costs, conversion costs, inventoriable costs and period costs.

Prime costs include direct materials and direct manufacturing labor. Conversion costs include indirect manufacturing costs. They are calculated based on costs incurred for direct materials, direct manufacturing labor, and indirect manufacturing costs.

Inventoriable costs include costs that are included in inventory valuation and become part of the cost of goods sold. Period costs are expenses recognized immediately on the income statement for the period incurred and do not enter into inventory valuation.

You might also like

- Basic Pension WorksheetDocument1 pageBasic Pension WorksheetIbnu GamingNo ratings yet

- Jawaban BE15 - AKMDocument3 pagesJawaban BE15 - AKMMazz BadruezNo ratings yet

- Working 3Document6 pagesWorking 3Hà Lê DuyNo ratings yet

- P2 41 2 42 SolutionsDocument3 pagesP2 41 2 42 SolutionsMarjorie PalmaNo ratings yet

- Chapter 2Document34 pagesChapter 2Marjorie PalmaNo ratings yet

- Chapter 2 Homework4 PDFDocument3 pagesChapter 2 Homework4 PDFMarjorie PalmaNo ratings yet

- Technology and Livelihood Education: Quarter 2, Wk.5-6 - Module 9Document17 pagesTechnology and Livelihood Education: Quarter 2, Wk.5-6 - Module 9Marjorie PalmaNo ratings yet

- E7-39 Comparing ABC and Plantwide Overhead Cost Assigments: Setup Hours Oven HoursDocument3 pagesE7-39 Comparing ABC and Plantwide Overhead Cost Assigments: Setup Hours Oven HoursDhiva Rianitha Manurung100% (1)

- Chapter 17 HWDocument40 pagesChapter 17 HWEejay MagatNo ratings yet

- Kunci Jawaban Semua BabDocument46 pagesKunci Jawaban Semua BabMuhammad RifqiNo ratings yet

- Chapter 7. KeyDocument8 pagesChapter 7. KeyHuy Hoàng PhanNo ratings yet

- Cost Accounting Chapter 2 Assignment #3Document5 pagesCost Accounting Chapter 2 Assignment #3Tawan VihokratanaNo ratings yet

- Modern China EssayDocument5 pagesModern China Essayapi-358096422No ratings yet

- Coca Cola HistoryDocument12 pagesCoca Cola HistorylaquemecuelgaNo ratings yet

- Evan and Brett Are Students at Berkeley CollegeDocument3 pagesEvan and Brett Are Students at Berkeley CollegeElliot RichardNo ratings yet

- Kelompok 4-SOAL STANDAR COSTINGDocument3 pagesKelompok 4-SOAL STANDAR COSTINGAndriana Butera0% (1)

- Forum 6Document1 pageForum 6cecillia lissawatiNo ratings yet

- Jawaban TugasDocument7 pagesJawaban TugasRani AdhirasariNo ratings yet

- BAB 16 v2Document10 pagesBAB 16 v2rahmat lubisNo ratings yet

- Yohanes Bosko Arya B - 041711333195 - AKM E23.11, P23.4Document3 pagesYohanes Bosko Arya B - 041711333195 - AKM E23.11, P23.4ulil alfarisyNo ratings yet

- Exercise 6Document4 pagesExercise 6Tania MaharaniNo ratings yet

- Soal Ch. 15Document6 pagesSoal Ch. 15Kyle KuroNo ratings yet

- ACY4001 Individual Assignment 2 SolutionsDocument7 pagesACY4001 Individual Assignment 2 SolutionsMorris LoNo ratings yet

- Equity SoalDocument2 pagesEquity SoalVinna ZhuangNo ratings yet

- E22-6 (LO 2) Accounting Changes-DepreciationDocument6 pagesE22-6 (LO 2) Accounting Changes-DepreciationRiana DeztianiNo ratings yet

- Exercise - Dilutive Securities - AdillaikhsaniDocument4 pagesExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsanNo ratings yet

- Tugas Minggu 3Document9 pagesTugas Minggu 3Elsha FitriNo ratings yet

- Tugas 1 AklDocument3 pagesTugas 1 Akledit andraeNo ratings yet

- Putri Amalia Fillah - AKL II - Assignment 3Document2 pagesPutri Amalia Fillah - AKL II - Assignment 3Amalia FillahNo ratings yet

- The Statement of Financial Position of Stancia Sa at DecemberDocument1 pageThe Statement of Financial Position of Stancia Sa at DecemberCharlotte100% (1)

- Chapter 1 Beams 13ed RevisedDocument32 pagesChapter 1 Beams 13ed RevisedEvan AnwariNo ratings yet

- Tugas AKL P1-3Document14 pagesTugas AKL P1-3bagong kusset100% (1)

- Chap 008Document66 pagesChap 008dsementsova100% (1)

- Spoilage, Rework, and ScrapDocument35 pagesSpoilage, Rework, and ScrapMohammed S. ZughoulNo ratings yet

- CH 08Document10 pagesCH 08Antonios FahedNo ratings yet

- Tugas Managerial Accounting Sesi 4Document3 pagesTugas Managerial Accounting Sesi 4Breneta TanNo ratings yet

- E10 16Document1 pageE10 16september manisNo ratings yet

- Wahyudi Syaputra - Assignment Week 13Document11 pagesWahyudi Syaputra - Assignment Week 13Wahyudi Syaputra100% (1)

- Latihan 3Document3 pagesLatihan 3Radit Ramdan NopriantoNo ratings yet

- Tugas 2 AklDocument3 pagesTugas 2 Akledit andraeNo ratings yet

- E22 3Document2 pagesE22 3bella0% (1)

- Essence Company Blends and Sells Designer FragrancesDocument2 pagesEssence Company Blends and Sells Designer FragrancesElliot Richard100% (1)

- Uas AKMDocument14 pagesUas AKMThorieq Mulya MiladyNo ratings yet

- Jawaban Soal Latihan Ch.11Document2 pagesJawaban Soal Latihan Ch.11Wira DinataNo ratings yet

- Akmen Soal Review Uas PDFDocument8 pagesAkmen Soal Review Uas PDFvionaNo ratings yet

- Consolidated Financial Statement Excercise 3-3Document2 pagesConsolidated Financial Statement Excercise 3-3Winnie TanNo ratings yet

- FIX ASSET&INTANGIBLE ASSET Kel. 1 AKM 1 PDFDocument6 pagesFIX ASSET&INTANGIBLE ASSET Kel. 1 AKM 1 PDFAdindaNo ratings yet

- Tugas Pertemuan 4Document6 pagesTugas Pertemuan 4Nisrina ChairunnisaNo ratings yet

- ACCT550 Homework Week 1Document6 pagesACCT550 Homework Week 1Natasha DeclanNo ratings yet

- Nama: Nurahma Amalia NIM: 20200070042 Kelas: AK20ADocument4 pagesNama: Nurahma Amalia NIM: 20200070042 Kelas: AK20Aedit andraeNo ratings yet

- ACCT 3125 Chapter 5 SolutionsDocument7 pagesACCT 3125 Chapter 5 SolutionskayNo ratings yet

- Latihan Soal Segment and Interim ReportingDocument5 pagesLatihan Soal Segment and Interim ReportingNebula JrNo ratings yet

- Comprehensive Problems Solution Answer Key Mid TermDocument5 pagesComprehensive Problems Solution Answer Key Mid TermGabriel Aaron DionneNo ratings yet

- Tugas Akmen Fadhliya Fauziah CH 8Document18 pagesTugas Akmen Fadhliya Fauziah CH 8FadhliyaFNo ratings yet

- Chapter 4 CourseDocument15 pagesChapter 4 CourseMagdy KamelNo ratings yet

- Journal Entry at The Step of TransactionDocument4 pagesJournal Entry at The Step of Transactionadmin finishyourtaskNo ratings yet

- Soal Ab1 (Tm-1) Cost ConceptDocument5 pagesSoal Ab1 (Tm-1) Cost ConceptAntonius Sugi SuhartonoNo ratings yet

- ANSWER - Cost Accounting Session 1Document5 pagesANSWER - Cost Accounting Session 1Vincenttio le Cloud0% (1)

- Homework For Week 11Document4 pagesHomework For Week 11Andika PratamaNo ratings yet

- Chapter 1 ReviewDocument17 pagesChapter 1 Reviewmahedre100% (1)

- CA Tutorial - Week 2 - QuestionsDocument3 pagesCA Tutorial - Week 2 - QuestionsAndhika YogaraksaNo ratings yet

- Peterson Company Beginning of End of 2017 2017Document7 pagesPeterson Company Beginning of End of 2017 2017Daniel YebraNo ratings yet

- Cost Accounting Part 1Document21 pagesCost Accounting Part 1Mostafa ElgendyNo ratings yet

- Pengelompokan BiayaDocument17 pagesPengelompokan BiayaMaya BangunNo ratings yet

- An Introduction To Cost Terms and Purposes Homework 2-42, 46 2-42 Income Statement and Schedule of Cost of Goods Manufactured. Chan's ManufacturingDocument3 pagesAn Introduction To Cost Terms and Purposes Homework 2-42, 46 2-42 Income Statement and Schedule of Cost of Goods Manufactured. Chan's ManufacturingCheuk Wai YEUNGNo ratings yet

- Cost Accounting Prelims Practice Solving 1 50 1Document24 pagesCost Accounting Prelims Practice Solving 1 50 1Marjorie PalmaNo ratings yet

- Examples 2-1 Computing and Interpreting Manufacturing Unit CostsDocument10 pagesExamples 2-1 Computing and Interpreting Manufacturing Unit CostsMarjorie PalmaNo ratings yet

- Accounting/Actg Misc Valix Chapter 1-Chapter 6-Joy: Click Here For AnswersDocument22 pagesAccounting/Actg Misc Valix Chapter 1-Chapter 6-Joy: Click Here For AnswersMarjorie PalmaNo ratings yet

- Instruction: Encircle The Letter of The Correct Answer in Each of The Given QuestionDocument6 pagesInstruction: Encircle The Letter of The Correct Answer in Each of The Given QuestionMarjorie PalmaNo ratings yet

- Test 1 Chapter 1 2 3Document11 pagesTest 1 Chapter 1 2 3Marjorie PalmaNo ratings yet

- Cost Accounting and Cost Management 1: Chapter 1 - Review of The Non-Cost SystemDocument5 pagesCost Accounting and Cost Management 1: Chapter 1 - Review of The Non-Cost SystemMarjorie PalmaNo ratings yet

- Finance Zutter CH 1 4 REVIEWDocument112 pagesFinance Zutter CH 1 4 REVIEWMarjorie PalmaNo ratings yet

- Rice Company Was Incorporated On January 1Document6 pagesRice Company Was Incorporated On January 1Marjorie PalmaNo ratings yet

- Soln SSP S1Document12 pagesSoln SSP S1Marjorie PalmaNo ratings yet

- HW 1accountingDocument2 pagesHW 1accountingMarjorie PalmaNo ratings yet

- Mapeh 10 Module (Week 4) QTR 2Document12 pagesMapeh 10 Module (Week 4) QTR 2Marjorie Palma0% (1)

- Steven Cardona Assessment 1 1 5Document6 pagesSteven Cardona Assessment 1 1 5Marjorie PalmaNo ratings yet

- Balance Sheet and Statement of Cash Flows: True-FalseDocument45 pagesBalance Sheet and Statement of Cash Flows: True-FalseMarjorie PalmaNo ratings yet

- Chapter 15 Chi Square ApplicationsDocument23 pagesChapter 15 Chi Square ApplicationsMarjorie PalmaNo ratings yet

- Impairment Revaluation and Intangibles Acctg 3 Intermediate Accounting IDocument47 pagesImpairment Revaluation and Intangibles Acctg 3 Intermediate Accounting IMarjorie PalmaNo ratings yet

- Mapeh 10 Module (Week 8) QTR 2Document12 pagesMapeh 10 Module (Week 8) QTR 2Marjorie PalmaNo ratings yet

- Chapter 3 Valix Vol 3Document17 pagesChapter 3 Valix Vol 3Marjorie PalmaNo ratings yet

- Pre Week MaterialsDocument44 pagesPre Week MaterialsMarjorie PalmaNo ratings yet

- Revaluation ModelDocument36 pagesRevaluation ModelMarjorie PalmaNo ratings yet

- 1st Sem 2021 2022 Final Examination Schedule v4Document3 pages1st Sem 2021 2022 Final Examination Schedule v4Marjorie PalmaNo ratings yet

- InventoriesDocument64 pagesInventoriesMarjorie PalmaNo ratings yet

- Press Release: Philippine Rural Development Project Regional Project Coordination Office 13Document2 pagesPress Release: Philippine Rural Development Project Regional Project Coordination Office 13Zee AwingNo ratings yet

- Biography of DR - Veghese Kurien: Kajal IsraniDocument15 pagesBiography of DR - Veghese Kurien: Kajal IsraniDhavalNo ratings yet

- Forward Rate and Future Spot Rate RelationshipDocument20 pagesForward Rate and Future Spot Rate Relationshipveronica100% (1)

- SLW CLASS X Sectors of Indian Economy 2024Document6 pagesSLW CLASS X Sectors of Indian Economy 2024anushka.sinha965No ratings yet

- Notes1 & 2Document17 pagesNotes1 & 2wingkuen107No ratings yet

- MicroDocument3 pagesMicroYashNo ratings yet

- Project Work AmcDocument26 pagesProject Work AmcUday KiranNo ratings yet

- India Japan RelationsDocument9 pagesIndia Japan RelationskanishkamanickasundaramNo ratings yet

- Macro and Micro EconomicsDocument24 pagesMacro and Micro EconomicspriyaNo ratings yet

- NAILTA Amicus BriefDocument24 pagesNAILTA Amicus BriefOAITANo ratings yet

- B Com 80 20 Pattern Mar 2022Document4 pagesB Com 80 20 Pattern Mar 2022Nishant ChaudhariNo ratings yet

- Fruit Juice SampleDocument22 pagesFruit Juice SampleVishnu SreekanthanNo ratings yet

- Business Plan 2024-2025Document16 pagesBusiness Plan 2024-2025lioneltran1289No ratings yet

- Reseller ProposalDocument4 pagesReseller ProposalnjthakkarNo ratings yet

- Impact of GST On Economy and BusinessesDocument11 pagesImpact of GST On Economy and BusinessesMaryam MujawarNo ratings yet

- Kal 3Document2 pagesKal 3mdnathNo ratings yet

- Structure Final Test-CompleteDocument6 pagesStructure Final Test-CompleteYuniarso Adi NugrohoNo ratings yet

- Marketing Management Dant KantiDocument4 pagesMarketing Management Dant KantiKaran FrancisNo ratings yet

- 1089 V K Textiles IndustriesDocument1 page1089 V K Textiles IndustriesEglNo ratings yet

- Central Bank of India: Iv Part D - Rental Rates For Safe Deposit Locker Dimensions Volume in Cu - CmsDocument2 pagesCentral Bank of India: Iv Part D - Rental Rates For Safe Deposit Locker Dimensions Volume in Cu - CmsAnkur SharmaNo ratings yet

- Electric VehiclesDocument56 pagesElectric VehiclesNikolic DejanNo ratings yet

- Claim Case FormsDocument22 pagesClaim Case Formsknow_umarNo ratings yet

- Strategy Analysis of AirtelDocument19 pagesStrategy Analysis of AirtelNamit JainNo ratings yet

- Five Unexpected Benefits of Carpooling - How To Reduce Your Carbon FootprintDocument3 pagesFive Unexpected Benefits of Carpooling - How To Reduce Your Carbon FootprintVijaya Ratna MNo ratings yet

- Contract DocumentDocument45 pagesContract DocumentEngineeri TadiyosNo ratings yet

- CRCF Annual Report 2008Document34 pagesCRCF Annual Report 2008nketchumNo ratings yet

- House For Rent in Gikondo-ManualDocument8 pagesHouse For Rent in Gikondo-ManualDebbie CarterNo ratings yet

- Turkey - Oil & Fats Profile PDFDocument3 pagesTurkey - Oil & Fats Profile PDFmrithika25012011No ratings yet