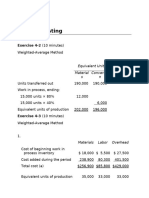

Midterm - Ch. 17

Midterm - Ch. 17

Download as docx, pdf, or txt

You might also like

- Midterm - Ch. 10, 11Document14 pagesMidterm - Ch. 10, 11Cameron BelangerNo ratings yet

- Chapter 8 Assignment AnswersDocument20 pagesChapter 8 Assignment AnswersPattraniteNo ratings yet

- Process Costing ProblemsDocument9 pagesProcess Costing ProblemsAries Bautista67% (3)

- Chapter 4-Exercises-Managerial AccountingDocument3 pagesChapter 4-Exercises-Managerial AccountingSheila Mae LiraNo ratings yet

- Practical Earned Value Analysis: 25 Project Indicators from 5 MeasurementsFrom EverandPractical Earned Value Analysis: 25 Project Indicators from 5 MeasurementsNo ratings yet

- 17-38 Transferred-In Costs, Weighted-Average Method. Bookworm, Inc., Has TwoDocument6 pages17-38 Transferred-In Costs, Weighted-Average Method. Bookworm, Inc., Has TwoMajd MustafaNo ratings yet

- Mock Exam Cost Acct 2023Document6 pagesMock Exam Cost Acct 2023Lam HảiNo ratings yet

- Q & Soln - Process CostingDocument6 pagesQ & Soln - Process CostingAbhay SahuNo ratings yet

- Assignment 3 AnswersDocument4 pagesAssignment 3 AnswersJake ShinNo ratings yet

- CostaccDocument4 pagesCostaccjaringanlimagNo ratings yet

- Class Case For Chapter 17 2015 AdjustedDocument8 pagesClass Case For Chapter 17 2015 Adjustedahmed.alaradi88No ratings yet

- 17-16 (25 Min.) Equivalent Units, Zero Beginning InventoryDocument5 pages17-16 (25 Min.) Equivalent Units, Zero Beginning Inventorymohamet farahNo ratings yet

- Chapter 18 AssignmentDocument2 pagesChapter 18 AssignmentMikasa MikasaNo ratings yet

- UntitledDocument4 pagesUntitledAastha ShettyNo ratings yet

- Solutions MA Chapter 3 Book Version (AutoRecovered)Document3 pagesSolutions MA Chapter 3 Book Version (AutoRecovered)achhpilia.muskan.psNo ratings yet

- Chapter 3Document7 pagesChapter 3worknehNo ratings yet

- Mymie B. Maandig MBA-1 Dr. Marco Ilano Problem 4-13A RequiredDocument9 pagesMymie B. Maandig MBA-1 Dr. Marco Ilano Problem 4-13A RequiredMymie MaandigNo ratings yet

- Module 3 Stracos HW DocsDocument12 pagesModule 3 Stracos HW DocsMALICDEM, CharizNo ratings yet

- 17-19 Page 631 Physical Direct Conversion Units Materials CostsDocument4 pages17-19 Page 631 Physical Direct Conversion Units Materials CostsMisty Dawn BancroftNo ratings yet

- MANACC Class Handout - Process Costing-1Document6 pagesMANACC Class Handout - Process Costing-1Ritwik MahajanNo ratings yet

- Ch17 SolutionsDocument47 pagesCh17 SolutionsJaneNo ratings yet

- Tutorial 3 - MA - Weighted,, FifoDocument9 pagesTutorial 3 - MA - Weighted,, FifoCodreanu AndaNo ratings yet

- Total Costs For October 2017Document4 pagesTotal Costs For October 2017mohitgaba19No ratings yet

- Cost Accounting Chapter 17Document4 pagesCost Accounting Chapter 17Yordan Lawijaya100% (1)

- Universidad Interamericana de Puerto Rico Recinto de San Germán Departamento de Ciencias EmpresarialesDocument5 pagesUniversidad Interamericana de Puerto Rico Recinto de San Germán Departamento de Ciencias EmpresarialesAqib LatifNo ratings yet

- Presentación Capitulo 17 Clase 16 Jueves 26 de MarzoDocument18 pagesPresentación Capitulo 17 Clase 16 Jueves 26 de MarzoBrandon AlejandroNo ratings yet

- 8- Cost Accounting (1)- Chapter (2) - Process Costing- Part 3Document6 pages8- Cost Accounting (1)- Chapter (2) - Process Costing- Part 3com01156499073No ratings yet

- Weekly Discussion 8Document2 pagesWeekly Discussion 8bphamNo ratings yet

- Seminar 4 Tutor - ACC203Document38 pagesSeminar 4 Tutor - ACC203Regina KwokNo ratings yet

- Chapter 04 WorksheetDocument13 pagesChapter 04 WorksheetqpelinsubcNo ratings yet

- Chapter 3 ExamplesDocument2 pagesChapter 3 ExamplesAli Gökay BozokNo ratings yet

- Chapter 4Document26 pagesChapter 4ReineNo ratings yet

- Baking DepartmentDocument6 pagesBaking DepartmentkmarisseeNo ratings yet

- 1843 Question HelpDocument9 pages1843 Question Helpchong chojun balsaNo ratings yet

- Assignment Question AccDocument5 pagesAssignment Question AccruqayyahqaisaraNo ratings yet

- Process CostingDocument66 pagesProcess Costingarshad mNo ratings yet

- Chapter 4 - Process Costing: Click On LinksDocument15 pagesChapter 4 - Process Costing: Click On LinksNiraj PatilNo ratings yet

- Production Cost ReportDocument1 pageProduction Cost ReportRhea Mae CoronelNo ratings yet

- Case 1. Landers CompanyDocument3 pagesCase 1. Landers CompanyMavel DesamparadoNo ratings yet

- ACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsDocument11 pagesACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsJingwen YangNo ratings yet

- Lesson No 5 (Process Costing)Document8 pagesLesson No 5 (Process Costing)Arun kumarNo ratings yet

- Acct1 8Document5 pagesAcct1 8kutipan raraNo ratings yet

- CH 4 and 5 Cost IDocument11 pagesCH 4 and 5 Cost IBēkām BūllōōNo ratings yet

- Unit 6 Cost Accumulation SystemsDocument41 pagesUnit 6 Cost Accumulation Systemsestihdaf استهدافNo ratings yet

- CMA Question 2Document4 pagesCMA Question 2Shifat sjt100% (1)

- Cost Accounting Chapter 4Document18 pagesCost Accounting Chapter 4Matthew cNo ratings yet

- ACTG 360 Cost Accounting Midterm Exam 01Document12 pagesACTG 360 Cost Accounting Midterm Exam 01Nguyễn Thị Thanh ThúyNo ratings yet

- Makalah CH 14 Audit Siklus Penjualan Dan Penagihan Pertemuan 4Document4 pagesMakalah CH 14 Audit Siklus Penjualan Dan Penagihan Pertemuan 4arief kurniawanNo ratings yet

- Chapter 4 Practice Questions SOLUTIONDocument11 pagesChapter 4 Practice Questions SOLUTIONMohamed MostafaNo ratings yet

- Work in Process, Beginning:: Required: Prepare A Production Report For The Department Using The Weighted-Average MethodDocument6 pagesWork in Process, Beginning:: Required: Prepare A Production Report For The Department Using The Weighted-Average MethodJhunorlando DisonoNo ratings yet

- Comprehensive Problem - WAVE Method For Spoilage-2Document2 pagesComprehensive Problem - WAVE Method For Spoilage-2aey de guzmanNo ratings yet

- Cost AssignmentDocument3 pagesCost AssignmentAbrha GidayNo ratings yet

- Quiz 3Document7 pagesQuiz 3pragadeeshwaran100% (1)

- Additional Examples With Solutions 17Document24 pagesAdditional Examples With Solutions 17Dachi ChaduneliNo ratings yet

- Raw Materials InventoryDocument4 pagesRaw Materials InventoryMikias DegwaleNo ratings yet

- Process-Costing Self-Study-Activity With AnswersDocument9 pagesProcess-Costing Self-Study-Activity With AnswersDane PerezNo ratings yet

- Lec3 ProcesscostingDocument25 pagesLec3 Processcostinghello1928No ratings yet

- Acc 2Document5 pagesAcc 2nma.work173No ratings yet

- D. All of The Above Are True.: AMIS 3300 Pop Quiz - Chapter 17Document5 pagesD. All of The Above Are True.: AMIS 3300 Pop Quiz - Chapter 17DIGNA HERNANDEZNo ratings yet

- Product - Midterm ACC C203-205A: SolutionDocument5 pagesProduct - Midterm ACC C203-205A: SolutionMarkJoven BergantinNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Exam Review - Module 3Document7 pagesExam Review - Module 3Cameron BelangerNo ratings yet

- Exam Review - Module 2Document8 pagesExam Review - Module 2Cameron BelangerNo ratings yet

- Midterm - Ch. 4Document15 pagesMidterm - Ch. 4Cameron BelangerNo ratings yet

- Midterm - Ch. 1, 2, 3Document16 pagesMidterm - Ch. 1, 2, 3Cameron BelangerNo ratings yet

- Midterm - Ch. 5Document13 pagesMidterm - Ch. 5Cameron BelangerNo ratings yet

- ADM1301 Final ReviewDocument35 pagesADM1301 Final ReviewCameron BelangerNo ratings yet

- CH 4 - SS ProblemsDocument8 pagesCH 4 - SS ProblemsCameron BelangerNo ratings yet

- A Sunny Valentine v2Document73 pagesA Sunny Valentine v2alex.quispe0305No ratings yet

- 4K Ultra Slim LED TV Powered by Android TV: With Ambilight 2-SidedDocument3 pages4K Ultra Slim LED TV Powered by Android TV: With Ambilight 2-SidedMarjan StojanoskiNo ratings yet

- NDT Eddy CurrentsDocument13 pagesNDT Eddy Currentsyashwant verma100% (1)

- EST3 Zoned Audio AmplifiersDocument4 pagesEST3 Zoned Audio Amplifierstomjakson333No ratings yet

- Python Booklet Semikgroup LQDocument1 pagePython Booklet Semikgroup LQsymasiNo ratings yet

- Applied Soft Computing: Hani Pourvaziri, B. NaderiDocument13 pagesApplied Soft Computing: Hani Pourvaziri, B. Naderiregarcia81No ratings yet

- Improved Syntheses of Peptide Coupling Reagents Bop and Pybop Using TriphosgeneDocument5 pagesImproved Syntheses of Peptide Coupling Reagents Bop and Pybop Using TriphosgeneSulthon Rizki F. AzharNo ratings yet

- Dynamic ErrorDocument7 pagesDynamic ErrorSuvra PattanayakNo ratings yet

- ELEMENT 11 Electricity2Document11 pagesELEMENT 11 Electricity2mano chandranNo ratings yet

- AN - RF Current To Electric Field Strength Extrapolation - V1.0Document5 pagesAN - RF Current To Electric Field Strength Extrapolation - V1.0Michael MayerhoferNo ratings yet

- Service Manual Videocon Ff-Vz330l, 280l, 250lDocument39 pagesService Manual Videocon Ff-Vz330l, 280l, 250ljitendraNo ratings yet

- Afp 20170615 P 805Document1 pageAfp 20170615 P 805Janaina MarquesNo ratings yet

- 19 LaserDocument27 pages19 LaserYash JadhavNo ratings yet

- Direction:: Write The Letter of The Correct Answer. Use CAPITAL LETTERS OnlyDocument7 pagesDirection:: Write The Letter of The Correct Answer. Use CAPITAL LETTERS OnlyDominic Dalton CalingNo ratings yet

- Kaolinite DatabaseDocument4 pagesKaolinite DatabaseErina Rizki NugrahaniNo ratings yet

- Yamaha DSP Ax2600 RX v2600Document155 pagesYamaha DSP Ax2600 RX v2600Winslow-1132No ratings yet

- Module 1 DDCODocument20 pagesModule 1 DDCOarshadahmedkkpNo ratings yet

- Rakesh ProjectDocument41 pagesRakesh ProjectRock RockyNo ratings yet

- Major Activities of Honey BeeDocument18 pagesMajor Activities of Honey Beechirag pandeyNo ratings yet

- 27-Unnatural Death - Patricia CornwellDocument315 pages27-Unnatural Death - Patricia CornwellMarlie ProdehlNo ratings yet

- Perry's Chemical Engineers' Handbook, 8th Edition 242Document1 pagePerry's Chemical Engineers' Handbook, 8th Edition 242Ooi Chia EnNo ratings yet

- DCB 68 Sliding Hinge JointDocument34 pagesDCB 68 Sliding Hinge JointczapatachueNo ratings yet

- Chemistry in Everyday LifeDocument7 pagesChemistry in Everyday LifeDHARANEESH E 11BNo ratings yet

- FBD 562Document56 pagesFBD 5620304201169No ratings yet

- 2011-05-23 King Drive Streetscape Plan FinalDocument57 pages2011-05-23 King Drive Streetscape Plan Finalapi-272667969No ratings yet

- Example: Questions 1-4Document5 pagesExample: Questions 1-4Vitória Rodovalho100% (1)

- Plant Cell - WikipediaDocument32 pagesPlant Cell - WikipediaSherelyn Bernardo100% (1)

- K.Anh - Upgrade 3 UNIT 4Document2 pagesK.Anh - Upgrade 3 UNIT 4HameeyNo ratings yet

- Chakra MeditationDocument4 pagesChakra MeditationChandilyan SNo ratings yet

- Meteorology and ClimatolodyDocument7 pagesMeteorology and ClimatolodySylvia Sinda100% (1)