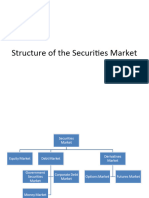

Secondary Market

Secondary Market

Download as ppt, pdf, or txt

You might also like

- Trading StrategyDocument2 pagesTrading StrategyAzizalindaNo ratings yet

- Rural Marketing - Unit 3 (Targeting, Segmenting and Positioning)Document33 pagesRural Marketing - Unit 3 (Targeting, Segmenting and Positioning)Vamshi NCNo ratings yet

- 16 Operating Costing 1 (ASIDJKHDutosaved)Document20 pages16 Operating Costing 1 (ASIDJKHDutosaved)Deepak R GoradNo ratings yet

- On Banking Sector For PresentationDocument23 pagesOn Banking Sector For Presentationvaishali haritNo ratings yet

- Session 12 CVP AnalysisDocument52 pagesSession 12 CVP Analysismuskan mittalNo ratings yet

- The Primary Market in IndiaDocument34 pagesThe Primary Market in IndiaPINAL100% (1)

- Chapter 1 Banking and OperationsDocument15 pagesChapter 1 Banking and OperationsManavAgarwal0% (1)

- Capital and Revenue TransactionsDocument23 pagesCapital and Revenue TransactionsRajib Deb100% (1)

- Merchant BankingDocument10 pagesMerchant BankingSejal ChavanNo ratings yet

- CH 2 Indian Financial SystemDocument46 pagesCH 2 Indian Financial SystemAkshay AhirNo ratings yet

- Indian Money Market and Capital MarketDocument17 pagesIndian Money Market and Capital MarketMerakizz100% (1)

- 7 TariffDocument22 pages7 TariffParvathy SureshNo ratings yet

- Business EnvironmentDocument1 pageBusiness Environmentnani66215487No ratings yet

- Overview of Financial SystemDocument50 pagesOverview of Financial SystemshahyashrNo ratings yet

- FEIA 2&5m Question With AnswerDocument5 pagesFEIA 2&5m Question With Answerprashanthuddar6No ratings yet

- TariffDocument21 pagesTariffNiranjan Taware100% (1)

- Commercial Banks in IndiaDocument29 pagesCommercial Banks in IndiaVarsha SinghNo ratings yet

- Mgnrega PPT CRM OrientationDocument77 pagesMgnrega PPT CRM Orientationmkshri_in0% (1)

- Monte Carlo My Presentation PDFDocument11 pagesMonte Carlo My Presentation PDFRASHMINo ratings yet

- Departmental Accounts: by Dr. Pranabananda Rath Consultant & Visiting FacultyDocument16 pagesDepartmental Accounts: by Dr. Pranabananda Rath Consultant & Visiting FacultyAnamika VatsaNo ratings yet

- 1 5Document14 pages1 5kunjaNo ratings yet

- Managerial Economics - A Decision Science andDocument5 pagesManagerial Economics - A Decision Science andSam NietNo ratings yet

- Stock Market I. What Are Stocks?Document9 pagesStock Market I. What Are Stocks?JehannahBaratNo ratings yet

- Mba Anna University PPT Material For MBFS 2012Document39 pagesMba Anna University PPT Material For MBFS 2012mail2nsathish67% (3)

- BCom I-Unit III - Notes On Working Capital ManagementDocument9 pagesBCom I-Unit III - Notes On Working Capital ManagementRohit Patel100% (3)

- Electricity TariffDocument34 pagesElectricity Tariffdks12No ratings yet

- Small Scale IndustryDocument14 pagesSmall Scale IndustryNandiniBharatNo ratings yet

- RBI Classification of MoneyDocument10 pagesRBI Classification of Moneyprof_akvchary60% (5)

- Balance of Payment: Meaning and ComponentsDocument6 pagesBalance of Payment: Meaning and ComponentsForum DaghaNo ratings yet

- A Study About Investment & Transition in Indian Derivative Markets.Document79 pagesA Study About Investment & Transition in Indian Derivative Markets.SurajKashidNo ratings yet

- NCDCDocument14 pagesNCDCsudadhich100% (1)

- Efficient Market TheoryDocument3 pagesEfficient Market TheoryVinay KushwahaaNo ratings yet

- Stock Market IndicesDocument15 pagesStock Market Indicesarco1234No ratings yet

- Calculation Methof of KSE-100 IndexDocument23 pagesCalculation Methof of KSE-100 Indexamina_rabia100% (2)

- Indian Financial SystemDocument16 pagesIndian Financial SystemParth UpadhyayNo ratings yet

- Chapter 1 PDFDocument20 pagesChapter 1 PDFANILNo ratings yet

- Monetary PolicyDocument32 pagesMonetary PolicyAbhi JainNo ratings yet

- Types of Market StructuresDocument25 pagesTypes of Market StructuresAngelo Mark Pacis100% (1)

- Neft and RtgsDocument15 pagesNeft and Rtgssandhya22No ratings yet

- Bagedari SectorDocument32 pagesBagedari SectorswathiNo ratings yet

- Assessment of Various EntitiesDocument31 pagesAssessment of Various Entitiesinsathi0% (1)

- A Comparative Study On BSE and NSEDocument30 pagesA Comparative Study On BSE and NSEShailja ManyaNo ratings yet

- Indian Accounting Standard 5Document12 pagesIndian Accounting Standard 5Rattan Preet SinghNo ratings yet

- Cost Function NotesDocument7 pagesCost Function Noteschandanpalai91100% (1)

- Production FunctionDocument6 pagesProduction Functionshrey100% (1)

- Airtel - 4psDocument42 pagesAirtel - 4psPraveen SangwanNo ratings yet

- Participants in OTCEI MarketDocument7 pagesParticipants in OTCEI MarketAshu158No ratings yet

- IIMMDocument24 pagesIIMMarun1974No ratings yet

- RtgsDocument13 pagesRtgsBari Rajnish100% (2)

- Share CapitalDocument76 pagesShare CapitalCollege CollegeNo ratings yet

- 1 Joint Stock Company PPT by ManasDocument10 pages1 Joint Stock Company PPT by ManaspadhnedebcNo ratings yet

- Money Market's InstrumentsDocument20 pagesMoney Market's InstrumentsManmohan Prasad RauniyarNo ratings yet

- IMT 79 Economic Environment of India M2 PDFDocument27 pagesIMT 79 Economic Environment of India M2 PDFDivyangi WaliaNo ratings yet

- Recent Dev in Stock MKT 1Document19 pagesRecent Dev in Stock MKT 1Manikandan N-17No ratings yet

- Origin of Share Markets in IndiaDocument18 pagesOrigin of Share Markets in IndiasrinivasjettyNo ratings yet

- FMO Module 3Document11 pagesFMO Module 3Sonia Dann KuruvillaNo ratings yet

- Capital Market Reforms and FfoDocument10 pagesCapital Market Reforms and FfoVishruti Shah JobanputraNo ratings yet

- Project Report On Stock Market "Working of Stock Exchange & Depositary Services"Document11 pagesProject Report On Stock Market "Working of Stock Exchange & Depositary Services"Kruti NemaNo ratings yet

- Stock Exchanges - A ProfileDocument24 pagesStock Exchanges - A Profilerohitluthra88No ratings yet

- Secondary Markets in IndiaDocument49 pagesSecondary Markets in Indiayashi225100% (1)

- Article Writing - Capital Market - Jyoti Mittal - FBD ChapterDocument5 pagesArticle Writing - Capital Market - Jyoti Mittal - FBD ChapterEsayas ArayaNo ratings yet

- Bba IV Bis Unit 4 NotesDocument12 pagesBba IV Bis Unit 4 NotesHarsh ThakurNo ratings yet

- 850Document21 pages850Harsh ThakurNo ratings yet

- Players in The MarketDocument17 pagesPlayers in The MarketHarsh ThakurNo ratings yet

- Chapter 4Document34 pagesChapter 4Harsh ThakurNo ratings yet

- Money Market Its InstrumentsDocument13 pagesMoney Market Its InstrumentsHarsh ThakurNo ratings yet

- Chapter 1Document16 pagesChapter 1Harsh ThakurNo ratings yet

- School of Managment Sciences, Varanasi (An Autonomous College)Document2 pagesSchool of Managment Sciences, Varanasi (An Autonomous College)Harsh ThakurNo ratings yet

- Fso Unit-3Document7 pagesFso Unit-3Harsh ThakurNo ratings yet

- Chapter 3Document32 pagesChapter 3Harsh ThakurNo ratings yet

- Capital Primary MarketDocument45 pagesCapital Primary MarketHarsh ThakurNo ratings yet

- Mutual Funds 1Document42 pagesMutual Funds 1Harsh ThakurNo ratings yet

- Bba IV Bis Unit 3 NotesDocument18 pagesBba IV Bis Unit 3 NotesHarsh ThakurNo ratings yet

- Significance of Diagrams and GraphsDocument2 pagesSignificance of Diagrams and GraphsHarsh ThakurNo ratings yet

- Bagi Saving AccountsDocument5 pagesBagi Saving Accountstengku nesaNo ratings yet

- 2021 Retake Exam in Corporate FInanceDocument4 pages2021 Retake Exam in Corporate FInanceNikolai PriessNo ratings yet

- Paper1 With Cover Page v2Document18 pagesPaper1 With Cover Page v2Palash WanwaniNo ratings yet

- NISM Series v-A-Mutual Fund Distributors Workbook - 2020Document341 pagesNISM Series v-A-Mutual Fund Distributors Workbook - 2020prachiNo ratings yet

- Dokumen - Pub Options Trading in Bear Mkts 0070152721 9780070152724Document303 pagesDokumen - Pub Options Trading in Bear Mkts 0070152721 9780070152724saktirajNo ratings yet

- Roth IRA Investing Starter KitDocument17 pagesRoth IRA Investing Starter KitHuliaNo ratings yet

- BS ProjectDocument15 pagesBS Projectgoplo singhNo ratings yet

- Rudra TrishatiDocument3 pagesRudra TrishatiAnkurNagpal108No ratings yet

- Comparative Analysis On Selected Public Sector and Private Sector Mutual Funds in India With Special Reference To Growth FundsDocument9 pagesComparative Analysis On Selected Public Sector and Private Sector Mutual Funds in India With Special Reference To Growth Fundsparmeen singhNo ratings yet

- 2024 l1 Topics CombinedDocument27 pages2024 l1 Topics CombinedShaitan Ladka0% (1)

- The Most Effective Stock Trading Strategy in Indonesia Equity MarketDocument8 pagesThe Most Effective Stock Trading Strategy in Indonesia Equity Marketjon doeNo ratings yet

- Fs SP 500 CadDocument7 pagesFs SP 500 Cadalt.sa-33bwuogNo ratings yet

- A Study On Customer's Preference While Investing in Systematic Investment PlanDocument11 pagesA Study On Customer's Preference While Investing in Systematic Investment PlanK C ChandanNo ratings yet

- Overview of The Financial System: QuestionsDocument15 pagesOverview of The Financial System: QuestionsAmbra KoraNo ratings yet

- Bản Sao Của 22040291 - Lê Bảo Linh Đan - English for Finance and Banking Case Study 3Document12 pagesBản Sao Của 22040291 - Lê Bảo Linh Đan - English for Finance and Banking Case Study 3qainparis77No ratings yet

- IAPM AssignmentDocument5 pagesIAPM AssignmentSushant ThombreNo ratings yet

- Factsheet NiftyMidSmallFinancialSevicesDocument2 pagesFactsheet NiftyMidSmallFinancialSevicesKrishna GoyalNo ratings yet

- Passive Equity InvestingDocument2 pagesPassive Equity InvestingkypvikasNo ratings yet

- Kantor Blog Reddit PhenomenonDocument2 pagesKantor Blog Reddit PhenomenonCaptain GurkoNo ratings yet

- IACFMAS-ASSIGN MarjDocument4 pagesIACFMAS-ASSIGN MarjMarjorie PagsinuhinNo ratings yet

- Finmar - Chapter 12 - 14Document24 pagesFinmar - Chapter 12 - 14AlexanNo ratings yet

- AQR Alternative Thinking 3Q17Document20 pagesAQR Alternative Thinking 3Q17magNo ratings yet

- MBA 223 Financial Markets InstitutionsDocument15 pagesMBA 223 Financial Markets InstitutionsDragon BankNo ratings yet

- Role of Financial Markets and InstitutionsDocument35 pagesRole of Financial Markets and InstitutionsThảo Linh TrầnNo ratings yet

- 1.3. EP13.NHLT1107 - Monetary and Financial Theories 2023 RevisedDocument24 pages1.3. EP13.NHLT1107 - Monetary and Financial Theories 2023 RevisedNgọc LươngNo ratings yet

- Discussion Problems InvestmentsDocument2 pagesDiscussion Problems InvestmentsSamantha Nicole ValdezNo ratings yet

- Second Updated Research ProposalDocument45 pagesSecond Updated Research ProposalNebiyu KebedeNo ratings yet

- HSC SP Q.6. Justify PDFDocument4 pagesHSC SP Q.6. Justify PDFTanya SinghNo ratings yet

- Question Bank Nism Equity DerivativeDocument13 pagesQuestion Bank Nism Equity Derivativedev12_lokeshNo ratings yet