Featured Survey Analysis

Microbusinesses Performed $6.1 Billion of R&D in the United States in 2021

October 30, 2023

Product ID: NSF 24-302

The ABS is the primary source of information on research and development among for-profit businesses operating in the United States with one to nine employees. The ABS also collects data on innovation, technology, intellectual property, and financing from U.S.-based companies of all sizes.

The ABS collects data on research and development (for businesses with one to nine employees), innovation, technology, intellectual property, and business owner characteristics, with additional rotating content that changes from year to year.

The ABS is cosponsored by the National Center for Science and Engineering Statistics and the Census Bureau.

| Status | Active |

|---|---|

| Frequency | Annual |

| Reference Period | Calendar year 2021 |

| Next Release Date | October 2025 |

The Annual Business Survey (ABS) is the primary source of information on research and development (R&D) expenditures for nonfarm, for-profit, businesses operating in the United States with one to nine employees. The ABS also collects data on innovation-related data, globalization, and business owner characteristics from nonfarm, for-profit, businesses operating in the United States with at least one employee.

Modules were added on Goods, Services, and Business Processes and Technology; Design and Intellectual Property; and Domestic and Foreign Transactions (Globalization). Five new questions were added, and one question was removed in the Coronavirus Pandemic Impact on R&D and Business Activities module. Questions on capital expenditures were added to the R&D module. A question was added on owner disability in the owner demographics module.

Annual.

Calendar year 2017; for innovation, the reference period was 2015–17.

Calendar year 2021; for innovation, the reference period was 2019–21.

Nonfarm businesses in the United States.

Sample survey of for-profit companies with a U.S. presence engaged in the mining, utilities, construction, manufacturing, wholesale trade, retail trade, or services industries.

Approximately 4,900,000 employer businesses.

Approximately 300,000 employer businesses.

Key variables of interest are listed below.

The target population consists of all for-profit nonfarm companies that are physically located in the United States, that have at least one establishment classified as being an in-scope sector based on the North American Industry Classification System (NAICS), and that was in business during the survey reference year and data collection period.

The Business Register, maintained by the Census Bureau, is the source used to create the sampling frame for the ABS.

The ABS has a systematic stratified sampling design that uses simple random sampling within strata. Stratification is based on the NAICS industry code. Companies were selected with certainty if they are known R&D performers with one to nine employees, 500 or more employees, or meet sampling stratum-specific cutoffs for receipts and payroll.

The ABS collects data electronically.

All data submitted by respondent companies are reviewed to ensure that data fields are complete and that data are internally consistent. Survey responses often include errors that require correction or unusual patterns that require validation. Automated edit checks are applied to improve the efficiency of data review and correction. Edit checks are designed to catch arithmetic errors and logically inconsistent responses (balance edits). The remaining automated edit checks are designed to flag outliers for further review (analytical edits). If additional information or data corrections are needed, respondents may be contacted to clarify or correct data. If additional information or corrected data cannot be obtained from respondents, data are imputed.

Estimates are produced from sums of weighted data (reported or imputed). Exceptions are described in detail in the tables containing relative standard errors and imputed rates (available upon request from the Survey Manager).

Estimates of sampling errors associated with the ABS data tables are available from the Survey Manager upon request.

There can be both undercoverage error, where units are not included in the frame, and overcoverage error, where units included in the frame are actually out of scope for the population of interest. The ABS uses the prior-year Business Register to construct the frame, so any changes in businesses that would change the inclusion or exclusion of the business to the survey scope could be sources of coverage error. Prior to tabulation, survey units’ information is updated with the most recently available Business Register data to mitigate this source of error.

Unit nonresponse will be done by adjusting weighted reported and imputed data by multiplying each company's sampling weight by a nonresponse adjustment factor. Detailed descriptions of the adjustments for nonresponse will be available in the ABS data tables (https://ncses.nsf.gov/surveys/annual-business-survey/).

Expected sources of measurement error include differences in respondent interpretations of the definitions of R&D activities and differences in how companies count and report numbers of employees in various categories, including whether they work on R&D full time or part time. Error can also occur when respondents do not report dollar amounts correctly. Although quantitative metrics of measurement error are not available, there are ongoing efforts to minimize measurement error, including questionnaire pretesting, improvement of questionnaire wording and format, inclusion of more cues and examples in the questionnaire instructions, in-person and telephone interviews and consultations with respondents, and post-survey evaluations.

Data produced from the ABS will be available at https://ncses.nsf.gov/surveys/annual-business-survey/.

The ABS is a cross-sectional survey designed to produce annual estimates of R&D performance and related statistics. Some estimates from the ABS may not be directly comparable to prior ABS results due to changes in survey methodology. Sources of possible incomparability include changes to questionnaire wording and instructions, changes to data editing and tabulation, and changes to imputation and nonresponse adjustments.

ABS data will be published in NCSES InfoBriefs and data table reports in the Business and Industry R&D series (https://www.nsf.gov/statistics/industry/).

Results from this survey are available on the NCSES website at https://ncses.nsf.gov/. The ABS contains confidential data that are protected under Title 13 and Title 26 of the U.S. Code. Restricted microdata will be available at any of the 15 secure Research Data Centers administered by the Center for Economic Studies (CES) at the Census Bureau. Researchers interested in accessing microdata can apply for a restricted-use license by submitting a proposal to the CES, which evaluates proposals based on their benefit to the Census Bureau, scientific merit, feasibility, and risk of disclosure. To learn more about the Research Data Centers and how to apply, please visit the CES page on research opportunities https://www.census.gov/programs-surveys/ces.html. For additional information about the application process, including how to initiate a project, please contact the administrator at the primary site where the research will be conducted. Per the Federal Cybersecurity Enhancement Act of 2015, the data are protected from cybersecurity risks through screening of the systems that transmit the data.

Purpose. The Annual Business Survey (ABS) provides information on selected economic and demographic characteristics for businesses and business owners by sex, ethnicity, race, and veteran status. Further, the survey measures research and development (R&D) for microbusinesses, business topics such as innovation and technology, and other business characteristics. The ABS is conducted jointly by the Census Bureau and the National Center for Science and Engineering Statistics (NCSES) within the National Science Foundation (NSF). The ABS replaces the quinquennial Survey of Business Owners for employer businesses, the Annual Survey of Entrepreneurs, the Business R&D and Innovation for Microbusinesses Survey, and the Innovation section of the Business R&D and Innovation Survey.

The ABS is designed to incorporate new content each survey year based on topics of relevance. For the 2022 ABS, content includes company information, owner characteristics, research activities at nonprofit organizations, R&D, technology, innovation, financing, and management practices. R&D data are collected on the ABS for businesses with a W-2 employment range between one and nine employees.

Data collection authority. Title 13, U.S. Code, Sections 8(b), 131, and 182; Title 42, U.S. Code, Sections 1861–76 (NSF Act of 1950, as amended); and Section 505 within the America COMPETES Reauthorization Act of 2010, authorize this collection. Sections 224 and 225 of Title 13 require mandatory response. Office of Management and Budget (OMB) No. 0607-1004.

Survey sponsor. NCSES within NSF.

Survey collection and tabulation agent. The survey is conducted annually by the Census Bureau in accordance with an interagency agreement with NCSES within NSF.

Frequency. Annual.

Initial survey year. Calendar year 2017; for innovation, the reference period was 2015–17.

Reference period. Calendar year 2021; for innovation, the reference period was 2019–21.

Response unit. Nonfarm businesses in the United States.

Sample or census. Sample.

Population size. A total of 4.9 million employer firms; approximately 505,000 firms with one to nine employees and in North American Industry Classification System (NAICS) industries 31–33 (manufacturing), 42 (wholesale trade), 51 (information), 5413 (architectural, engineering, and related services), 5415 (computer systems design and related services), or 5417 (scientific research and development services) were in scope for the R&D module.

Sample size. 300,000 employer businesses.

Target population. Included are all nonfarm businesses filing Internal Revenue Service (IRS) tax forms as individual proprietorships, partnerships, or any type of corporation and with receipts of $1,000 or more. The target population included only companies that had paid employees according to the IRS Form 941 that covered 12 March 2022, are classified in an in-scope NAICS industry, were physically located in the United States, and were in business at the end of calendar year 2022. The ABS covers firms with paid employees only. The ABS is conducted on a company or firm basis rather than an establishment basis.

Sampling frame. The sampling universe was constructed from the final 2020 Business Register. The Business Register is the Census Bureau’s comprehensive database of U.S. businesses. Business Register data are compiled from a combination of business tax returns, data collected from the economic census, and data from other Census Bureau surveys. The Business Register includes sole proprietorships, partnerships, and corporations reporting business activity to the IRS on any one of the following IRS tax forms: 1040 (Schedule C), “Profit or Loss from Business” (Sole Proprietorship); 1065, “U.S. Return of Partnership Income”; 941, “Employer’s Quarterly Federal Tax Return”; 944, “Employer’s Annual Federal Tax Return”; or any one of the 1120 corporate tax forms.

The Business Register contains establishments that are out of scope for the ABS sample. These establishments are removed from the sampling universe. They include the following:

Information on industry classification, receipts, payroll, and employment was extracted from the Business Register during the frame construction.

The sample is also designed to estimate demographic characteristics of the business owners. To efficiently sample for demographic characteristics, a variety of sources of information are used to estimate the likelihood that a business is a woman- or minority-owned business. Administrative sources include the Decennial Census, the American Community Survey (ACS), and the Numident file, which is the Social Security Administration’s comprehensive database of information from Social Security applications. Individual business owners are identified through IRS K-1 filings for partnerships and corporations and from the Business Register for sole proprietorships. The owners are matched to the 2000 and 2010 Decennial Censuses to get race, sex, and ethnicity data; to the 2000–20 ACS; and to the Numident file (in that order) through a Protected Identification Key. Country of birth is also identified through the linkages to the ACS or Numident data. Each firm is then placed in one of the following eight strata describing characteristics of business owners for sampling: American Indian or Alaska Native, Asian, Black or African American, Hispanic, non-Hispanic White men, Native Hawaiian and Other Pacific Islander, publicly owned, and women owned. Businesses are assigned to one and only one stratum, with priority given to the less common race or ethnicity groups.

Sample design. The ABS frame is stratified by state, expected owner race or ethnicity, and industry and is systematically sampled within each stratum. A standard type of estimation for stratified systematic sampling is used. Large companies were selected with certainty based on volume of sales, payroll, or number of paid employees. Certainty cases have a selection probability of 1, a sampling weight of 1, and represent only themselves. Specifically for the 2022 ABS, firms were selected with certainty based on the following criteria:

The certainty cutoffs vary by sampling stratum, and each stratum is sampled at varying rates, depending on the number and size of firms in a particular stratum.

The remaining frame is subjected to stratified systematic random sampling. Sampling rates vary by strata and are determined by the following calculations. Note that a systematic sample uses take rate to sample, and the sampling rate is 1/take rate.

The ABS sample consisted of 300,000 businesses. There were 46,000 selected with certainty. The certainty portion of the sample consisted of

The remaining 254,000 noncertainty cases were selected using the systematic stratified random sample selection. The maximum sample weight was 40.

Data collection. Prior to mailing the survey, certain businesses selected were determined to be out of scope and were not contacted. The survey was mailed to 300,000 employer businesses in July 2022. Businesses were sent a letter informing them of their requirement to report. The letter also provided instructions on how to access the survey and submit online. There were three mail follow-ups conducted to increase response. Additionally, the Census Bureau conducted e-mail follow-ups to respondents who entered the electronic system but did not submit the questionnaire. The collection period closed in January 2023.

Mode. The 2022 ABS was collected using a Web-based survey instrument.

Check-in rate. The check-in rate is defined as the unweighted number of surveys that were submitted online by in-scope companies, divided by the unweighted total number of all in-scope companies in the sample. Response to individual questions did not factor into this metric. At the close of the collection period in January 2023, there were 184,000 responses submitted (62% of the sample).

There were an additional 1,900 businesses that contacted the Census Bureau to indicate that the business was no longer in operation or had been sold for the reference year via the call center.

Businesses selected to report R&D represented 39% of those mailed. Of the businesses mailed and selected to report R&D, 71,000 businesses (or 65%) submitted responses.

Unit response rate (URR). The URR is the unweighted number of responding companies for the survey. For the ABS, response is defined as a company providing the number of owners, number of paid owners, and number of employees or a company responding that it ceased operations prior to 2021.

For the ABS, the URR was 67.0%. The URR for businesses eligible to report the R&D module was 70.3%.

Item response rates (IRR). The 2022 ABS collected data on approximately 650 variables, and the distribution of values reported by sample companies is highly skewed. Thus, rather than report unweighted item response rates, total quantity response rates are calculated, which are based on weighted data. The survey skip patterns vary for respondents; therefore, it can be impossible to know an exact denominator for item response calculations.

Total quantity response rate (TQRR). For a given published estimate other than count or ratio estimates, TQRR is the percentage of the weighted estimate based on data that were reported by units in the sample or on data that were obtained from other sources and were determined to be equivalent in quality to reported data and weighted only by sampling but not nonresponse weights. The TQRR for total sales in the United States in 2020 was 72.6%.

Total quantity nonresponse rate (TQNR). For a given published estimate, TQNR, defined as 100% minus TQRR, is calculated for each tabulation cell from the ABS, except for cells that contain count or ratio estimates. TQNR measures the combined effect of the procedures used to handle unit and item nonresponse on the weighted ABS estimate. Detailed imputation rates are available on request.

Data editing. Prior to tabulating the data, response data were reviewed and edited to correct reporting errors. R&D data were tabulated for records reporting $50,000 or more in R&D expenditures.

Additionally, R&D data were only tabbed for records classified in the following NAICS industries:

Survey analysts reviewed the R&D reported by the survey respondents. Research was done by evaluating the reported business descriptions, reported R&D-to-sales ratio, and company website information. The majority of corrections involved false-positive reports or data reported using incorrect units (such as whole dollars instead of thousands of dollars). For NAICS industries 5415 and 5417, it is difficult to differentiate R&D from other technical work based solely on company website information. Due to this difficulty and the large number of companies sampled in these industries, it was not feasible to review each case individually; thus, relatively few corrections were made for false-positive reports. All cases were reviewed in these industries that had greater than $50,000 in R&D expenses.

Additional data errors were detected and corrected through mass corrections and an automated data edit system designed to review the data for reasonableness and consistency. The editing process interactively performed corrections by using standard procedures to fix detectable errors. Quality control techniques were used to verify that operating procedures were carried out as specified.

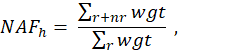

Unit nonresponse. Unit nonresponse is handled by adjusting weighted reported data as follows. Each company’s sampling weight is multiplied by a nonresponse adjustment factor. To calculate the adjustment factors, each company in the sample that is eligible for tabulation is assigned to one (and only one) adjustment cell. The adjustment cells are based on employment size and NAICS sector. For employment size, there are five categories: 1–4 employees, 5–9 employees, 10–49 employees, 50–249 employees, and 250 or more employees. For a given adjustment cell, the nonresponse adjustment factor is the ratio of the sum of the sampling weights for all companies in the cell to the sum of the sampling weights for all companies in the cell with reported data. The nonresponse adjustment factor for adjustment cell h was calculated as follows:

where

r is the respondents (partial and complete),

nr is the nonrespondents,

wgt is the original sampling weight value,

h is the nonresponse adjustment cell, and

NAFh is the nonresponse adjust factor for cell h.

For the nonresponse adjustment, a business is considered a respondent if it provided the number of owners, number of paid owners, and number of employees. Businesses that responded they ceased operations prior to 2021 are excluded from nonresponse adjustments as out of scope.

Tabulation. Although as many firms as possible were identified as out of scope during sampling, additional out-of-scope firms were identified with either response or updated administrative data not available at the time of sampling. These 33,000 firms were removed for tabulations and include

Industry classification. The industry classifications of firms are based on the 2017 NAICS (https://www.census.gov/naics/). Firms with more than one domestic establishment are assigned a single industry classification using a hierarchal system based on the largest payroll sector, largest payroll 3-digit NAICS (within the largest sector), largest payroll 4-digit NAICS (within the largest 3-digit), and largest payroll 6-digit NAICS (within the largest 4-digit). For tabulation, industry classification was based on administrative data for 2017.

Geography. Firms with establishments operating in more than one state are tabulated as unclassified geography and counted only once in state and national totals.

Variance estimation. The ABS uses the delete-a-group jackknife variance estimator. Note that certainty cases do not contribute to the sampling variance. The delete-a-group jackknife variance estimator requires that every sampling stratum contains at least two sampled firms. Sampling strata that do not meet this requirement are collapsed as needed to create a new set of variance estimation strata that satisfies this requirement.

Data tables showing relative standard errors are available on request from the Survey Manager.

The estimates produced from the ABS are subject to both sampling and nonsampling errors.

Sampling error. The sampling error is described above in the variance estimation section.

Coverage error. Coverage error occurs when the frame fails to completely enumerate the population of interest. There can be both undercoverage error, where units are not included in the frame, and overcoverage error, where units included in the frame are actually out of scope for the population of interest. The ABS uses the prior-year Business Register to construct the frame, so any changes in businesses that would change the inclusion or exclusion of the business to the survey scope could be sources of coverage error. Prior to tabulation, survey units’ information is updated with the most recently available Business Register data to mitigate this source of error.

Nonsampling error. All surveys and censuses have nonsampling errors. Nonsampling errors are attributable to various sources, such as the inability to obtain information for all cases in the universe, imputation for missing data, data errors and biases, mistakes in recording or keying data, errors in collection or processing, and coverage problems.

Although explicit measures of the effects of these nonsampling errors are not available, adjustments are made to the published relative standard errors to account for errors associated with imputation of missing data. It is believed that most of the important operational and data errors were detected and corrected through an automated data edit designed to review the data for reasonableness and consistency. Quality control techniques were used to verify that operating procedures were carried out as specified.

Measurement error. The most common source of measurement error was reporting in different units (e.g., reporting whole dollars rather than thousands of dollars). Variations in respondent interpretations of the definitions of R&D activities are of particular concern, and error can occur when respondents do not report dollar amounts correctly. Little public information exists for most of the small businesses surveyed by the ABS, so it is difficult to determine whether companies are reporting R&D that satisfies the survey's definitions, particularly where the development of software and Internet applications are concerned. Although no metric of measurement error is produced, ongoing efforts to minimize measurement error include questionnaire pretesting, improvement of questionnaire wording and format, inclusion of more cues and examples in the questionnaire instructions, telephone interviews and consultations with respondents, and post-survey evaluations.

Some estimates from the 2022 ABS may not be directly comparable to prior ABS results due to changes in survey methodology. Sources of possible incomparability include changes to questionnaire wording and instructions, changes to data editing and tabulation, and changes to imputation and nonresponse adjustments.

Changes in survey coverage and population. There were no changes to survey coverage and population for reference year 2021 (ABS 2022).

Changes to questionnaire wording and instructions. The survey section that collected information on R&D from businesses (section D) had nearly identical question wording and instructions for both the ABS 2021 and the ABS 2020 questionnaires. The 2022 ABS collected additional detail from businesses on the location of R&D performance and explicitly highlighted the concept of “domestic R&D performance.” For the 2022 ABS detailed questions about R&D expenditures (types of costs, funding sources, and R&D categories) were tied to domestic R&D performance (a subset of total R&D costs), whereas previous ABS questionnaires asked similar questions tied to total R&D costs.

The following are survey changes in the questionnaire from ABS 2021 to ABS 2022; question number references are in reference to the ABS 2022:

Changes in reporting procedures or classification. There were no changes to reporting procedures or classification for data year 2021.

Changes to data editing and tabulation. For data collected in the R&D section of the ABS, every response with $50,000 or more in R&D costs was reviewed for reasonableness. All positive R&D cases were reviewed in industries with high rates of false-positive reports. Outside of the review for potential false-positive R&D cases, the editing of R&D data was performed similarly in 2020 and 2021. There have been no major changes to the edits from year to year.

Data collected in the innovation section of the ABS were edited similarly in 2018 and 2019, but the estimates for product innovation were tabulated differently. For 2017, a business must have responded positively to both the product innovation question and the subsequent business product innovation question (new to market or new to business) to be considered a product innovator. For 2021 and 2022, only a positive response to the question regarding new or improved goods or services was required to be tabulated as a product innovator.

Changes in imputation methods. In 2019, a change was made in how item nonresponse is treated in the ABS. Item nonresponse occurs when a company responds to the survey but leaves some items blank. In 2018, item nonresponse was treated using a combination of mode and donor imputation. For 2019 and future years (including 2021), no imputation was performed to treat item nonresponse, and missing items were included as no or zero in the estimates. For most of the estimates in 2019 (91%), this change in methods did not yield a change in the estimates. For an additional 9% of estimates, there was a difference in the estimate; the difference, however, was not statistically significant. In 2021, the imputation method was updated to exclude out-of-scope firms as donors and recipients. In previous ABS years, all sampled firms were included in imputation and out-of-scope firms were later removed.

Changes in collection methods. During the 2022 ABS collection period, a single letter was mailed to respondents using U.S. Postal Service Priority Mail. For the 2022 ABS, the third follow-up used First Class Mail.

Recommended data tables

This report provides data from the 2022 Annual Business Survey (ABS) (data year 2021). The ABS is the primary source of data on research and development of for-profit, nonfarm businesses with one to nine employees operating in the 50 U.S. states and the District of Columbia. The ABS also collects data on innovation, technology, intellectual property, and business owner characteristics of business of all sizes. The ABS is designed to incorporate new content each survey year based on topics of relevance. The 2022 ABS is the fifth year of the ABS. The survey is conducted annually by the Census Bureau for the National Center for Science and Engineering Statistics within the National Science Foundation.

The Census Bureau has reviewed this data product to ensure appropriate access, use, and disclosure avoidance protection of the confidential source data (Project No. P-7504866, Disclosure Review Board (DRB) approval number: CBDRB-FY23-0394).

This report is initially published with a selection of tables containing the core data of the survey. The report will be updated with additional tables as more detailed data become available. In some instances, the initial selection of tables may also be updated from a preliminary version to add further data.

The first set of tables in this report, 1–30, released in October 2023.

The second set of tables in this report, 31–85, released in June 2024.

The third and final set of tables in this report, CET-1–CET-64, released in August 2024.

Audrey E. Kindlon of the National Center for Science and Engineering Statistics (NCSES) developed and coordinated this report under the guidance of Amber Levanon Seligson, NCSES Program Director, and under the leadership of Emilda B. Rivers, NCSES Director; Christina Freyman, NCSES Deputy Director; and John Finamore, NCSES Chief Statistician. In partnership with NCSES, the Census Bureau conducted the survey and prepared the tables. NCSES staff members who made significant contributions include Gary Anderson, Jock Black, and Timothy Wojan.

The Census Bureau, under National Science Foundation interagency agreement number NCSE-1748418, collected, processed, evaluated, and tabulated the data for this report. The Annual Business Survey is conducted within the Economic Directorate of the Census Bureau under the direction of Nick Orsini, Associate Director for Economic Programs, and Stephanie Studds, Assistant Director for Economic Programs.

The data were prepared in the Economic Reimbursable Surveys Division under the direction of Kevin Deardorff, Division Chief, and Aneta Erdie, Assistant Division Chief. This work was performed under the supervision of Patrice Hall, assisted by John Clark, Lakitquana Leal, and Gail White, with staff assistance from Concepcion Arenas Alvarez, Ahmad Bakhshi, Elaine Emanuel, Mary Frauenfelder, Aaron Finkle, Samantha Hernandez, James Jarzabkowski, Jessica Welch, and Tesfay Weldu. Additional support, including table creation and subject matter expertise, was provided by Brandon Shackelford.

Mathematical and statistical techniques were provided by the Economic Statistical Methods Division under the direction of James Hunt, Assistant Division Chief. This work was performed under the supervision of Roberta Kurec, assisted by Sandra Peterson, and Dhanapati Khatiwoda, with staff support from Taylor Beebe, Alexandra Abzún Cadenas, Charles Champion, and Daniel Cordes.

Data collection procedures and operations were provided by the Economic Management Division under the direction of Lisa Donaldson, Division Chief, and Michelle Karlsson, Assistant Division Chief. The staff of the National Processing Center performed mailout preparation, respondent assistance, and correspondence processing. Project management support was provided by Laura Hardesty and Aja Madison.

Development and coordination of the computer processing system was provided by the Economic Application Division under the direction of Sumit Khaneja, Division Chief and Olajumoke Oyewole, Assistant Division Chief. This work was performed by Marilyn Balogh, Michael Feldman, David Gonzalez, Chakravarthy Sharad, and Joseph Talbot.

National Center for Science and Engineering Statistics (NCSES). 2024. Annual Business Survey: 2022 (Data Year 2021). NSF 24-303. Alexandria, VA: National Science Foundation. Available at https://ncses.nsf.gov/surveys/annual-business-survey/2022.

For additional information about this survey or the methodology, contact