Chapter 009 TS Budgeting

Chapter 009 TS Budgeting

Download as ppt, pdf, or txt

You might also like

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersFrom EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNo ratings yet

- School Operational Work Plan WordDocument7 pagesSchool Operational Work Plan Wordkiptewit girls100% (2)

- Earned Value Management: Fast Start Guide: The Most Important Methods and Tools for an Effective Project ControlFrom EverandEarned Value Management: Fast Start Guide: The Most Important Methods and Tools for an Effective Project ControlRating: 5 out of 5 stars5/5 (2)

- Budgetary Planning and Control: 7.1 Nature and Purposes of BudgetsDocument18 pagesBudgetary Planning and Control: 7.1 Nature and Purposes of Budgetsserge folegweNo ratings yet

- Management Accounting Chapter 9Document57 pagesManagement Accounting Chapter 9Shaili SharmaNo ratings yet

- Cockney Dialect and SlangDocument28 pagesCockney Dialect and SlangPaula Perez100% (1)

- Slide MCS CH 8Document48 pagesSlide MCS CH 8Rizky Ramdhona PutraNo ratings yet

- Profit Planning, Activity-Based Budgeting and E-BudgetingDocument78 pagesProfit Planning, Activity-Based Budgeting and E-BudgetingAshesh DasNo ratings yet

- Profit Planning, Activity-Based Budgeting and E-BudgetingDocument78 pagesProfit Planning, Activity-Based Budgeting and E-BudgetingAshesh DasNo ratings yet

- Supplementary Lecture 2 Slides - Types of Budgets-Topic 2Document67 pagesSupplementary Lecture 2 Slides - Types of Budgets-Topic 2Prashant KumarNo ratings yet

- IPPTChap 009Document50 pagesIPPTChap 009Khaled BarakatNo ratings yet

- Profit Planning and Activity Based BudgetingDocument50 pagesProfit Planning and Activity Based BudgetingShaiannah Veylaine Recinto Apostol100% (1)

- Financial Planning and Analysis: The Master BudgetDocument37 pagesFinancial Planning and Analysis: The Master BudgetWailNo ratings yet

- Hilton 11e Chap009PPTDocument51 pagesHilton 11e Chap009PPTNgọc ĐỗNo ratings yet

- Rencana Pembelajaran 11: Budgeting & Beyond BudgetingDocument16 pagesRencana Pembelajaran 11: Budgeting & Beyond BudgetingbroniNo ratings yet

- Financial Planning and Analysis: The Master Budget: Mcgraw-Hill/IrwinDocument52 pagesFinancial Planning and Analysis: The Master Budget: Mcgraw-Hill/IrwinAmirah ZNo ratings yet

- Profit Planning and Activity-Based BudgetingDocument22 pagesProfit Planning and Activity-Based BudgetingaraiynNo ratings yet

- Hilton 11e Chap009PPTDocument52 pagesHilton 11e Chap009PPTNgô Khánh HòaNo ratings yet

- Master Budgeting and Responsibility AccountingDocument8 pagesMaster Budgeting and Responsibility AccountingAbdur RahmanNo ratings yet

- TM03 04 - Akman - Planningctrl Budgeting GJL 23 24Document91 pagesTM03 04 - Akman - Planningctrl Budgeting GJL 23 24Ramdonidoni doniNo ratings yet

- Mepl CostingDocument303 pagesMepl CostingVinay KumarNo ratings yet

- Chapter 9 Lecture - Student VersionDocument51 pagesChapter 9 Lecture - Student VersionIsaac SpoonNo ratings yet

- Profit Planning and Activity Based BudgetingDocument50 pagesProfit Planning and Activity Based BudgetingcahyatiNo ratings yet

- Chap 009 AccDocument50 pagesChap 009 AccIvanaNo ratings yet

- Master Budget: Sales ForecastDocument61 pagesMaster Budget: Sales ForecastLay TekchhayNo ratings yet

- Chapter 4 - BudgetingDocument9 pagesChapter 4 - BudgetingVuong PhamNo ratings yet

- Hilton 11e Chap009PPTDocument61 pagesHilton 11e Chap009PPTMinh Tâm TrầnNo ratings yet

- Session 3 - Lecture SlidesDocument14 pagesSession 3 - Lecture Slideshaddaoui zahraNo ratings yet

- ACCT 102 Management Accounting Master Budget and Responsibility AccountingDocument67 pagesACCT 102 Management Accounting Master Budget and Responsibility Accountingnishikant13No ratings yet

- Budgetary ControlDocument11 pagesBudgetary ControlrscjatNo ratings yet

- Financial Budget: Reporter: Katherine MiclatDocument57 pagesFinancial Budget: Reporter: Katherine MiclatMavis LunaNo ratings yet

- Budgeting: Basics and Beyond: Continuing Professional Development ModuleDocument46 pagesBudgeting: Basics and Beyond: Continuing Professional Development ModuleNarissa Mae QuijanoNo ratings yet

- SSIP H June 2022Document5 pagesSSIP H June 2022Rudy AquinoNo ratings yet

- Chapter 12Document27 pagesChapter 12Nazar NazriNo ratings yet

- Budgeting Basics and Beyond Ver. 4.0Document46 pagesBudgeting Basics and Beyond Ver. 4.0Ana Mae Tayoan Castro100% (1)

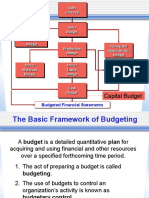

- Master Budgeting Master Budgeting: The Basic Framework of BudgetingDocument9 pagesMaster Budgeting Master Budgeting: The Basic Framework of BudgetingArisha KhanNo ratings yet

- BudgetingDocument22 pagesBudgetingAashikkhan50% (2)

- Budgeting & Budgetary ControlDocument28 pagesBudgeting & Budgetary ControlIeymarh FatimahNo ratings yet

- City Budget Office 1071Document2 pagesCity Budget Office 1071Charles D. FloresNo ratings yet

- Master Budgeting and Responsibility AccountingDocument17 pagesMaster Budgeting and Responsibility AccountingMahmozNo ratings yet

- Hilton Platt 12e SM Chap09Document58 pagesHilton Platt 12e SM Chap09Khaled BarakatNo ratings yet

- Notes - MAS - ManAcc (Budgeting)Document2 pagesNotes - MAS - ManAcc (Budgeting)ElaineJrV-IgotNo ratings yet

- Plan Cost Management Estimate Costs Create Work Breakdown StructureDocument3 pagesPlan Cost Management Estimate Costs Create Work Breakdown StructureAnifahchannie PacalnaNo ratings yet

- Chapter 7 - The Master Budget and Flexible Budgeting Flashcards - QuizletDocument5 pagesChapter 7 - The Master Budget and Flexible Budgeting Flashcards - QuizletBisag AsaNo ratings yet

- Budgetary ControlDocument31 pagesBudgetary ControlspectarNo ratings yet

- MS 06-04 BudgetingDocument3 pagesMS 06-04 BudgetingxernathanNo ratings yet

- Topic 7Document35 pagesTopic 7guloro2001No ratings yet

- MFP8 - Budgeting Financial PlanningDocument27 pagesMFP8 - Budgeting Financial PlanningKaren ClaudineNo ratings yet

- ACT4105 - Class 05 06 07 (Printing)Document24 pagesACT4105 - Class 05 06 07 (Printing)Wong Siu CheongNo ratings yet

- Ch. 8 Master Budgeting Flashcards - QuizletDocument5 pagesCh. 8 Master Budgeting Flashcards - QuizletBisag AsaNo ratings yet

- Budgets and Variance: Main TopicsDocument26 pagesBudgets and Variance: Main Topicschandana1992629No ratings yet

- IWB Chapter 6 - BudgetingDocument38 pagesIWB Chapter 6 - Budgetingjulioruiz891No ratings yet

- Ch09 PDFDocument37 pagesCh09 PDFAsh1No ratings yet

- Materi Kuliah Minggu Ke 13Document37 pagesMateri Kuliah Minggu Ke 13Binsar JosuaNo ratings yet

- MAS-42E (Budgeting With Probability Analysis)Document10 pagesMAS-42E (Budgeting With Probability Analysis)Fella GultianoNo ratings yet

- MAS 06 Budgeting With Probability AnalysisDocument10 pagesMAS 06 Budgeting With Probability AnalysisJericho G. Bariring100% (1)

- FP & B (PPT Lecture)Document38 pagesFP & B (PPT Lecture)Dyan LacanlaleNo ratings yet

- Financial Planning and Analysis The Master BudgetDocument57 pagesFinancial Planning and Analysis The Master BudgetBlackBunny103100% (1)

- L14 - Operational BudgetingDocument10 pagesL14 - Operational Budgetingluo jamesNo ratings yet

- Introduction to Project Management: The Quick Reference HandbookFrom EverandIntroduction to Project Management: The Quick Reference HandbookNo ratings yet

- Guide To Managing Data Breaches 2-0Document39 pagesGuide To Managing Data Breaches 2-0Longyin WangNo ratings yet

- Blockchain: Disrupting Data Protection?Document5 pagesBlockchain: Disrupting Data Protection?Longyin WangNo ratings yet

- Chapter 008 TS Variable & Absorption CostingDocument41 pagesChapter 008 TS Variable & Absorption CostingLongyin WangNo ratings yet

- Process Costing BJ Electronics Inc CaseDocument1 pageProcess Costing BJ Electronics Inc CaseLongyin Wang0% (1)

- Chapter 005 TS ABCDocument30 pagesChapter 005 TS ABCLongyin WangNo ratings yet

- Mba-Ai Speech Technologies: Prof. Brian MakDocument56 pagesMba-Ai Speech Technologies: Prof. Brian MakLongyin WangNo ratings yet

- Mba-Ai Speech and Natural Language Processing (NLP) TechnologiesDocument21 pagesMba-Ai Speech and Natural Language Processing (NLP) TechnologiesLongyin WangNo ratings yet

- Solutions To Practice ProblemsDocument3 pagesSolutions To Practice ProblemsLongyin WangNo ratings yet

- Practice Problems For The Final Exam of ISOM 5700: 1. Short Answer QuestionsDocument5 pagesPractice Problems For The Final Exam of ISOM 5700: 1. Short Answer QuestionsLongyin WangNo ratings yet

- Talk MBA AI XAI 2 PDFDocument76 pagesTalk MBA AI XAI 2 PDFLongyin WangNo ratings yet

- Talk MBA AI XAI 1 PDFDocument90 pagesTalk MBA AI XAI 1 PDFLongyin WangNo ratings yet

- Talk MBA AI XAI 3 PDFDocument81 pagesTalk MBA AI XAI 3 PDFLongyin WangNo ratings yet

- Artifical Intelligence-Final ProjectDocument13 pagesArtifical Intelligence-Final ProjectLongyin WangNo ratings yet

- Business Plan Report-Auto-Acoustic IncDocument10 pagesBusiness Plan Report-Auto-Acoustic IncLongyin WangNo ratings yet

- Koretz, Daniel. Measuring UpDocument4 pagesKoretz, Daniel. Measuring UprafadrimarquesNo ratings yet

- Unit 13 Family: 1. Nuclear FamiliesDocument3 pagesUnit 13 Family: 1. Nuclear FamiliesPhoom limsakounNo ratings yet

- A Toolkit For Integrating GENDER EQUALITY SOCIAL INCLUSIONDocument105 pagesA Toolkit For Integrating GENDER EQUALITY SOCIAL INCLUSIONAnnNo ratings yet

- Economía Política Syllabus I JuradoDocument9 pagesEconomía Política Syllabus I JuradoFELIPENo ratings yet

- XK AccessoriesDocument24 pagesXK AccessoriesAnonymous GKqp4Hn100% (1)

- Microeconomics CH 2ADocument5 pagesMicroeconomics CH 2Adeepak.5718.7bNo ratings yet

- Industry Analysis - Porters Five ForcesDocument18 pagesIndustry Analysis - Porters Five ForcesIjlal AshrafNo ratings yet

- ISO Clause 7Document4 pagesISO Clause 7Shailesh GuptaNo ratings yet

- Ex - No.3 (A) Open Circuit Characteristics of DC Shunt GeneratorDocument3 pagesEx - No.3 (A) Open Circuit Characteristics of DC Shunt GeneratorTapobroto ChatterjeeNo ratings yet

- Ges New Jhs Syllabus Computing CCP Curriculum b7 b10 Draft ZeroDocument106 pagesGes New Jhs Syllabus Computing CCP Curriculum b7 b10 Draft ZeroBenjamin MacFinn50% (2)

- TV080WXM NL0 LenovoDocument41 pagesTV080WXM NL0 Lenovozaur.bNo ratings yet

- 42 When Cultures Collide: Cultural Types: Color Coding Linear-Active, Multi-Active Reactive VariationsDocument1 page42 When Cultures Collide: Cultural Types: Color Coding Linear-Active, Multi-Active Reactive Variationsapi-19977019No ratings yet

- ფილოსოფიურ-თეოლოგიური მიმომხილველი #3 2013Document279 pagesფილოსოფიურ-თეოლოგიური მიმომხილველი #3 2013Giorgi KharibegashviliNo ratings yet

- Steiner, Rudolf PDFDocument17 pagesSteiner, Rudolf PDFAnonymous WvtWXOZUBo100% (1)

- Buckling of ColumnsDocument10 pagesBuckling of ColumnsM036No ratings yet

- 011 Nota Grafik Bab 2Document2 pages011 Nota Grafik Bab 2wan durahNo ratings yet

- Business Law Week 1 ModuleDocument4 pagesBusiness Law Week 1 ModuleJui ProvidoNo ratings yet

- How To Configure The Belkin Wireless Print ServerDocument16 pagesHow To Configure The Belkin Wireless Print ServerreckfaceNo ratings yet

- Vendredi Ou La Vie SauvageDocument2 pagesVendredi Ou La Vie Sauvagealitougui62No ratings yet

- Science Lesson PlanDocument1 pageScience Lesson Planapi-486845931No ratings yet

- Chord Formulas Charts How Chords Are Built PDF FreeDocument19 pagesChord Formulas Charts How Chords Are Built PDF FreeTaner ÖNGÜN100% (1)

- Web Based Pharmacy Management System For Debremarkos Red Cross SocietyDocument75 pagesWeb Based Pharmacy Management System For Debremarkos Red Cross SocietyMohammad Ganzab100% (9)

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)ISHANNo ratings yet

- Padaung Tribe of MyanmarDocument8 pagesPadaung Tribe of Myanmarnso2m2No ratings yet

- Othello - Brief Notes On Each SceneDocument9 pagesOthello - Brief Notes On Each SceneLouise CortisNo ratings yet

- Islamic Finance Instruments and Markets by Leading Experts in Islamic Finance Qatar Financial Centre (Z-Lib - Org) - DikonversiDocument313 pagesIslamic Finance Instruments and Markets by Leading Experts in Islamic Finance Qatar Financial Centre (Z-Lib - Org) - DikonversiAprilian DhevaNo ratings yet

- General Journal Description Date 2019 AprilDocument20 pagesGeneral Journal Description Date 2019 AprilHidalgo, John Christian MunarNo ratings yet

- Malaysia SEMy2030 - Booklet - ENGDocument109 pagesMalaysia SEMy2030 - Booklet - ENGverawahyuni86No ratings yet