US Data Show Inflation, Already Low, Slowed Further in July

Download as PPTX, PDF1 like1,870 views

US inflation slowed further in July by almost all measures, and continues to run well below the Fed's 2% target

More Related Content

What's hot (20)

Viewers also liked (8)

Similar to US Data Show Inflation, Already Low, Slowed Further in July (20)

More from Ed Dolan (20)

Recently uploaded (20)

US Data Show Inflation, Already Low, Slowed Further in July

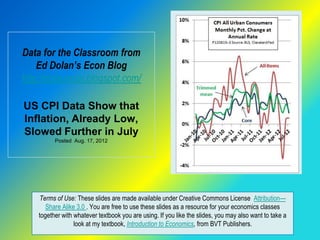

- 1. Data for the Classroom from Ed Dolan’s Econ Blog http://dolanecon.blogspot.com/ US CPI Data Show that Inflation, Already Low, Slowed Further in July Posted Aug. 17, 2012 Terms of Use: These slides are made available under Creative Commons License Attribution— Share Alike 3.0 . You are free to use these slides as a resource for your economics classes together with whatever textbook you are using. If you like the slides, you may also want to take a look at my textbook, Introduction to Economics, from BVT Publishers.

- 2. Headline Inflation was Near Zero The headline inflation rate in the latest BLS inflation report was zero for July, as it was for June Using unrounded data and stating the monthly change at an annual rate, seasonally adjusted inflation was 0.6% Energy prices fell in July, while food prices rose slightly. The largest price increases were for health care goods and services Posted Aug. 17, 2012 on Ed Dolan’s Econ Blog http://dolanecon.blogspot.com

- 3. Weak Energy Prices Bring Core Inflation Down Food and energy prices are volatile and usually account for much of the month-to-month change in the CPI Their effect can be removed by taking food and energy out of the CPI. The result is called the core inflation rate. The rate of core inflation for July, stated as an annual rate, was 1.09% Seasonally adjusted energy prices fell, let by lower prices for electricity and natural gas. Refinery disruptions caused an increase in retail gasoline prices Posted Aug. 17, 2012 on Ed Dolan’s Econ Blog http://dolanecon.blogspot.com

- 4. Trimmed Mean Inflation Also Remains Low Another way to remove volatility is the 16% trimmed mean CPI published by the Federal Reserve Bank of Cleveland. It removes the 8% of prices that increase most and the 8% that increase least in each month (or decrease most), whatever they are The 16 percent trimmed mean CPI slowed to an annual rate of 1.29 percent in July Posted Aug. 17, 2012 on Ed Dolan’s Econ Blog http://dolanecon.blogspot.com

- 5. Which Measure is Best? The CPI for all items gives the most accurate measure of current changes in the cost of living Economists at the Fed look closely at the core and trimmed mean CPIs to judge the effect of monetary policy on underlying inflationary trends The Fed considers inflation of about 2 percent to be consistent with prudent monetary policy. All three measures shown here were below the target for July Posted Aug. 17, 2012 on Ed Dolan’s Econ Blog http://dolanecon.blogspot.com

- 6. The Longer Term Trend To see longer term trends in inflation, it is useful to look at year- on-year changes, which compare each month’s price level with that of the same month in the year before All y-o-y measures of inflation rates slowed during the global recession, then rose again for most of 2011. The three measures shown here have moved steadily downward in 2012. All are close to or below the Fed’s targets Posted Aug. 17, 2012 on Ed Dolan’s Econ Blog http://dolanecon.blogspot.com

- 7. Index of Sticky Prices Falls Some prices, like those for food and energy, are flexible. They change daily in response to market condtions Others, like those for restaurant food, insurance, clothing, and medical care are sticky. Sellers of those goods adjust prices only when they are sure changes in market conditions will last Economists at the Atlanta Fed publish an index of sticky prices, which they think is a better indicator of future inflation trends than the CPI The rate of inflation measured by sticky prices showed sharply in July Posted Aug. 17, 2012 on Ed Dolan’s Econ Blog http://dolanecon.blogspot.com