The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1086-7376.htm

SEF

28,2

Saving and investment

in Saudi Arabia:

an empirical analysis

136

Reetu Verma

School of Economics, Faculty of Commerce, University of Wollongong,

Wollongong, Australia, and

Ali Salman Saleh

Accounting, Economics, Finance & Law (AEFL) Group,

Faculty of Business and Enterprise, Swinburne University of Technology,

Hawthorn, Australia

Abstract

Purpose – This paper examines the long-term relationship between saving and investment as a

criterion for assessing international capital mobility for the case of Saudi Arabia, the largest economy

among the Middle Eastern and Arab nations.

Design/methodology/approach – The approach is modeled on Feldstein and Horioka covering

the period 1963-2007 for Saudi Arabia. We use the bounds testing approach and the Gregory and

Hansen cointegration methods to test for the long-run relationship between saving and investment.

Additionally, before testing for this relationship, we conduct unit root tests, including the additive outlier

model developed by Perron with an endogenously determined structural break.

Findings – The study finds no evidence of a long-run relationship between saving and investment

and therefore concludes that capital is highly mobile in Saudi Arabia. This finding is plausible given

the economic and financial reforms which have occurred in Saudi Arabia along with increased capital

inflows into the country in the last few decades.

Originality/value – Of the limited studies so far on developing countries, none has considered the

capital mobility issue for an oil-dependent country.

Keywords Saving, Investment, Capital mobility, Saudi Arabia

Paper type Research paper

Studies in Economics and Finance

Vol. 28 No. 2, 2011

pp. 136-148

q Emerald Group Publishing Limited

1086-7376

DOI 10.1108/10867371111137139

1. Introduction

A sound grasp of the relationship between saving and investment is important for

understanding a country’s growth and economic development. Further to this, growth

models suggest that it is the amount of capital accumulation that determines the growth

of output and the amount of capital accumulation in an economy is ultimately

constrained by its saving rate. As the economy increases its saving, more funds will be

available for investment. Thus, the issue of correlation between saving and investment

assumed importance in economics. Much of the literature in this area focuses on the

relationship between saving and investment at both theoretical and empirical levels.

In their seminal paper, Feldstein and Horioka (1980) interpret the high correlation

between saving and investment rates as evidence of low international capital mobility.

Theoretically, in a closed economy with low capital mobility, domestic saving finances

JEL classification – C22, E20, E30

�all investment and hence the correlation is high. However, in an open economy, domestic

saving is not necessarily used to finance domestic investment, but will be used to gain

better returns in international capital markets. Contrary to these expectations, Feldstein

and Horioka (1980) find that capital is not very mobile internationally among developed

countries. Since then, many studies examine the relationship between saving and

investment for different time periods, data sets and country samples; both time-series

and cross-section studies exist. While the Feldstein and Horioka’s (1980) proposition

emphasizes the empirical association between savings and investment, no consensus

from the literature has emerged explaining this link.

Using US data from 1946 to 1987, Miller (1988) studies the relationship between saving

and investment by using cointegration techniques. He finds that the two variables shared

a cointegrating relationship prior to the Second World War period but the long-run

relationship did not exist after that period, leading Miller to conclude that the findings

could be explained by the increased level of international capital mobility after the war.

Many studies investigate the observed correlation between domestic saving and

investment in the European Union (EU) countries including Arginon and Roldan (1994),

Apergis and Tsoulfidis (1997), and Kollias et al. (2008). The first two studies find that saving

and investment are cointegrated and therefore conclude that capital is not very mobile in the

EU countries. Kollias et al. (2008) examine the saving-investment correlation using the

autoregressive distributed lag (ARDL) approach and panel regressions for 15 EU member

countries from 1962 to 2002. They find that a long-run relationship between the two

variables exists only for eight countries[1]. The authors accept the Feldstein and Horioka

explanation and interpret the finding as evidence of high capital mobility.

Using data covering the 1975-1995 period and dividing 90 developing countries into

four regions of Africa, Asia, Latin America, and the Middle East. Isaksson (2001) finds

that capital is relatively immobile for developing countries. On the other hand,

AbuAl-Foul (2006) examines the relationship between saving and investment rates by

using the Johansen and Juselius (1990) cointegration procedure. He finds that the two

variables are not cointegrated and concludes that capital is mobile in the four MENA

countries[2].

Ho (2000) extends the Feldstein and Horioka model to test for the capital mobility

issue by drawing two samples from two different regimes for Taiwan. He concludes that

the Feldstein and Horioka model is supported for the more open regime. Jansen (1996)

uses an error correction model to study the saving-investment relationship and finds

that the two rates have a long-run relationship for most of the Organisation for Economic

Co-operation and Development (OECD) countries. This is different from Chaudhri and

Wilson (2000) and Sachsida and Mendonça (2006) who find no long-run relationship

between saving and investment for Australia and Brazil, respectively.

Cooray and Sinha (2007) study the relationship between saving and investment rates

for 20 African countries. They use both the Johansen cointegration and fractional

cointegration tests which indicate mixed results. The Johansen cointegration test shows

that the saving and investment rates are cointegrated only for Rwanda and South Africa,

implying that for the other 18 countries, there is evidence of capital mobility. However,

the two rates are found to be fractionally cointegrated in 12 of the 20 countries examined.

Last, Ang (2007) examines the cointegrating relationship between domestic saving and

investment in Malaysia using the ARDL framework. Using data for the period 1965-2003,

he finds a long-run relationship between domestic saving and investment in Malaysia.

Saving and

investment

137

�SEF

28,2

138

There is one strand of the theoretical literature which departs from the FeldsteinHorioka approach. These studies describe a strong saving-investment correlation in the

presence of high capital mobility. They argue that the saving-investment correlation is

due to other macroeconomic factors such as country size (Baxter and Crucini, 1993),

non-traded goods (Murphy, 1986; Wong, 1990), current account solvency (Coakley et al.,

1996) and financial structure (Kasuga, 2004). But even here the empirical results

resulting from these studies vary considerably.

The objective of this study is to investigate whether a long-run relationship exists

between saving and investment in Saudi Arabia as a criterion for assessing the capital

mobility issue for this country. Our paper contributes to the existing literature in three

ways. First, of the limited studies so far on developing countries, none has considered the

issue of capital mobility for an oil-dependent country. Saudi Arabia is an interesting

case: not only is it is the largest economy among the Middle Eastern and Arab nations,

but also its economy is dominated by the oil sector. The oil sector accounts for

75-85 percent of government revenue and 90 percent of export revenue (Economic

Intelligence Unit (EIU, 2007). The country has also undergone remarkable changes in its

financial sector. The changes include the establishment of credit agencies and banks

during the 1960s and 1970s and the stock market in the 1980s leading to a considerable

financial and monetary system revolution (Albatel, 2003). Second, studies on the

saving-investment correlation fail to take into account any potential structural break in

their stationarity and/or cointegration estimations. It is well known that traditional tests

which do not allow for a structural break may produce spurious results. Last, the

availability of lengthy data series for Saudi Arabia also makes it an eminently suitable

case as it allows for a robust, in-depth country analysis to be conducted. According to

Ang (2007, p. 2168), “cross-sectional empirical analyzes conducted at the aggregate level

are unable to capture and account for the complexity of financial environments and

economic histories of each individual country”.

The aim of this paper is achieved in two-steps. In the first step, a detailed unit root

treatment of the data series is undertaken to establish their order of integration. The idea

behind this exercise is to ascertain whether, in the presence of structural break in the

data, the series are integrated of order one, or otherwise. To accomplish this step,

Perron’s (1997) one break unit root test with an endogenously determined structural

break is used. In the second step, the ordinary least square-based ARDL bounds test

(Pesaran et al., 2001) and the Gregory and Hansen (1996) methods for cointegration

between Saudi Arabia’s saving and investment are applied.

The remainder of the paper is organized as follows. Section 2 overviews the economy

of Saudi Arabia and Section 3 examines the conceptual model of the study. Sections 4

and 5 discuss the unit root and cointegration methodologies. The data and empirical

results are reported in Section 6. Section 7 concludes with some policy implications.

2. An overview: Saudi Arabia

Saudi Arabia is a very wealthy, oil producing country in the Middle East and has the

largest economy in the Arab and Gulf region. According to Al-Rajhi et al. (2003), gross

domestic product (GDP) in Saudi Arabia has increased dramatically since 2001 such that

Saudi Arabia is now by far the largest economy in the region, almost twice the size of

Israel or Egypt. However, the country’s growth is highly volatile due to its dependency

on oil revenues which are prone to price fluctuations. High economic growth occurred in

�Saudi Arabia during the 1970s and early 1980s but the country suffered a recession in the

mid 1980s. Saudi Arabia’s economy subsequently strengthened and again experienced

strong growth in the late 1980s and early 1990s. During the period 1993-2002, real GDP

growth averaged at approximately 1.5 percent a year. The rate of real GDP growth

increased to 7.7 percent per annum and the growth rate of nominal GDP rose to

19.8 percent. These growth rates were due to an increase in oil revenues as well as higher

oil prices in the overseas market. The high oil prices during 2004-2006 contributed to an

average real GDP growth of approximately 5 percent and an average nominal GDP of

approximately 17 percent (EIU, 2007).

Despite the government’s attempt to diversify its economy to non-oil sectors and

to promote private sector businesses, oil remains the major source of government

revenue. This sector accounted for 50 percent of GDP during 2005-2006 and provided

75-85 percent of government revenue (EIU, 2007). These figures were driven mainly by

oil exports and the accumulation of domestic capital. More recently, the non-oil sector

has attracted attention as the government is starting to realize the importance of

diversifying the economy. According to EIU (2007), 4.3 percent of real GDP growth for

the year 2006 was attributable to non-oil sectors and the private sector played an

important role in these activities.

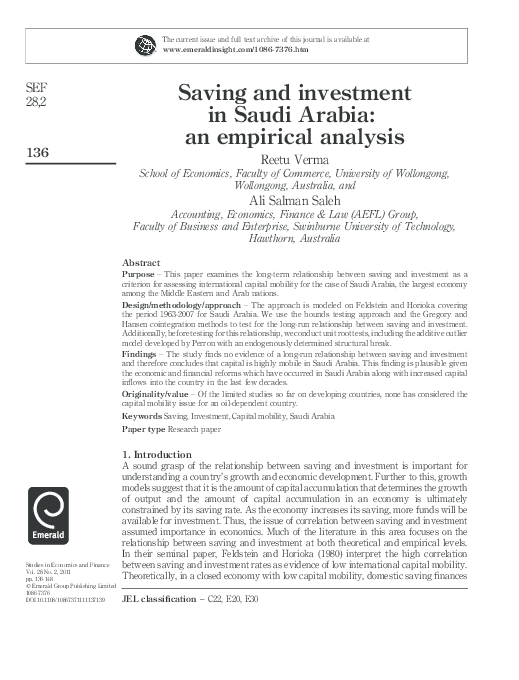

As shown in Figure 1, the country achieved remarkably high saving rates during

the 1970s and early 1980s indicating that Saudi Arabia was successful in mobilizing

saving. However, with expanded investment in infrastructure, the share of domestic

saving as a percentage of GDP decreased from approximately 60 percent in 1970 to

about 25 percent in 1992. The dramatic fall was mainly due to the Gulf War and the

energy crisis of the early 1990s. Domestic saving once again started to increase during

the late 1990s and 2000s reaching approximately 50 percent of GDP in 2007. This result

was achieved once again as a result of the improvement in oil prices, producing larger

oil revenues and increase in saving. Along with the rise in saving, broad money in the

country increased during 2006-2007; for example, broad money based on 10 months’

data grew from 11.8 percent in 2006 to over 13 percent in 2007 (SAMBA, 2008)[3].

Gross domestic investment also increased from an average of 11 percent in the 1970s

to 20 percent in 1992 and has remained around this level since then.

Note: Percentage of GDP

Source: The World Bank (2008)

139

2007

2005

2003

2001

Investment rate

1997

1995

1993

1991

1989

1987

1985

1983

1981

1979

1977

1975

1973

1971

1969

1967

1965

1963

Saving rate

1999

90

80

70

60

50

40

30

20

10

0

Saving and

investment

Figure 1.

Saving and investment

trends in Saudi Arabia

1963-2007

�SEF

28,2

140

Before 1952, Saudi Arabia had a simple, but an inadequate financial system. This

situation changed after the increase in oil prices in the 1970s-1980s when the government

realized the need for an adequate and effective financial system. The system underwent

major changes, including the establishment of the Saudi Arabian Monetary Agency in

1952, credit and other banking and financial institutions in the 1970s and the stock

market in the 1980s. According to Albatel (2003), the recent reforms in the financial

system in Saudi Arabia have impacted positively on the country’s economic growth and

the financial reforms have affected the relationship between saving and investment.

Thus, it becomes even more important to study the relationship between the two

variables given these changes in the last few decades in Saudi Arabia.

3. The conceptual framework

As indicated earlier, the correlation between saving and investment was first introduced

as a criterion for assessing international capital mobility by Feldstein and Horioka

(1980). The idea was that in a closed economy with low capital mobility, domestic saving

finances all investment. However, in an open economy, domestic saving is not

necessarily used to finance domestic investment, as saving will be used to gain better

returns in international capital markets. In the words of Feldstein and Horioka (1980,

p. 317) with perfect capital mobility, “there should be no relation between domestic

saving and domestic investment: saving in each country responds to the worldwide

opportunities for investment while investment in that country is financed by the

worldwide pool of capital”.

Feldstein and Horioka (1980) fit the following regression:

IR ¼ a þ b SR

ð1Þ

where a is the constant, IR is the investment rate and SR is the saving rate. IR is

defined as investment divided by GDP and SR is national saving divided by GDP.

Their empirical finding for equation (1) using a sample of 16 countries from 1960-1974

yields a very high degree of correlation between the two rates, prompting the authors

to conclude that capital is not very mobile among the major OECD countries.

To examine the saving-investment correlation in Saudi Arabia as expressed in

equation (1), we apply two cointegration techniques: ARDL bounds testing approach to

cointegration and the Gregory and Hansen (1996) cointegration method with an

endogenously determined structural break. The use of more than one estimator will

ensure the robustness of the results.

4. Unit root tests

Prior to conducting the cointegration tests, it is essential to check each time series for

stationarity. If a time series is non-stationary, traditional regression analysis will

produce spurious results. To ascertain the order of integration, we apply the traditional

augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests. However,

Perron (1989) shows that ignoring a structural break, as is the case with both ADF and

PP tests can lead to the false acceptance of the unit root null hypothesis. Therefore,

the Perron’s (1997) additive outlier (AO) model is applied, taking into account an

endogenously determined structural break.

When considering the AO model for testing a unit root, a two-step procedure is

used. First the series is de-trended using the following regression:

�yt ¼ m þ bt þ gDT*t þ y~ t

ð2Þ

where y~ t is the de-trended series and DT*t ¼ 1ðt 2 T b Þ if t . Tb and zero otherwise.

This procedure assumes that a structural break only affects the slope coefficient. Thus,

the test is then performed using the t-statistic for a ¼ 1 in the regression:

k

X

ci Dyt2i þ et

ð3Þ

y~ t ¼ ay~ t21 þ

i¼1

These equations are estimated sequentially for all possible values of Tb

(T b ¼ k þ 2; . . . ; T 2 1), where T is the total number of observations, so as to

minimize the t-statistic for a ¼ 1. The null hypothesis is rejected if the t-statistic for

a ¼ 1 is larger in absolute value than the corresponding critical value. The break date

is assumed to be unknown and endogenously determined by the data. The lag length, k is

data-determined using the general-to-specific method.

5. Cointegration tests

The ARDL cointegration approach

The cointegration concept is associated with the long-run equilibrium relationship between

two or more variables. Commonly used methods for conducting cointegration tests include

the residual-based Engle and Granger (1987) test and the maximum likelihood-based

Johansen (1991, 1995) and Johansen and Juselius (1990) tests. Owing to low power and other

problems associated with these tests, the ARDL bounds testing approach to cointegration

has become popular in recent years[4]. The ARDL bounds testing procedure has numerous

advantages over other cointegration techniques as outlined below:

.

The ARDL method avoids the pre-testing problems associated with the standard

cointegration techniques. The pre-testing procedure in the unit root cointegration

literature is problematic because the power of unit root tests are known to be

typically low and there is a switch in the distribution function of the test

statistics as one or more roots of the xt process approaches unity (Pesaran, 1997).

.

A further advantage of the ARDL method is that it is a more statistically

significant approach for determining cointegrating relationships in small

samples, whereas the Johansen cointegration technique requires larger samples

to be valid (Ghatak and Siddiki, 2001).

.

By using the F-test, the ARDL cointegration method can distinguish which series

is the dependent variable when cointegration exists (Narayan and Narayan, 2003).

To investigate the existence of a long-run relationship in equation (1), we

estimate the following unrestricted error-correction model (UECM):

n

n

X

X

cj DI t2j þ d1 S þ d2 I t21 þ 11t

bj DS t2j þ

ð4Þ

DS t ¼ a0 þ

j¼1

DI t ¼ a0 þ

n

X

j¼1

bj DI t2j þ

j¼1

n

X

cj DS t2j þ f1 I t21 þ f2 S t21 þ 12t

ð5Þ

j¼1

where D is the first difference operator, S is the saving rate and I is the investment

rate. The F-test is used for testing the existence of a long-run relationship between

Saving and

investment

141

�SEF

28,2

142

these two variables through testing the significance of the lagged level of variables

in the right-hand side of UECM. That is, we test for the null hypothesis of no

cointegrating relation in equation (4), H0:d1 ¼ d2 ¼ 0 against the alternative

HA:d1 ¼ d2 – 0. In equation (4), saving is the dependent variable and is expressed

as F(S/I). In equation (5), where investment is the dependent variable, denoted as

F(I/S), we test for the null hypothesis of no cointegration, H0:f1 ¼ f2 ¼ 0 against

the alternative HA:f1 ¼ f2 – 0.

These hypotheses are tested using the F-test with critical values tabulated by Pesaran

et al. (2001). The asymptotic distributions of the F-statistics are non-standard under the

null hypothesis of no cointegrating relationship between the examined variables,

irrespective of whether the variables are purely I(0) or I(1), or mutually cointegrated.

Pesaran et al. (2001) offer two sets of asymptotic critical values. The first set assumes

that all variables are I(0) and the second set assumes that all variables are I(1). The null

hypothesis of no cointegration is rejected if the calculated F-statistic is greater than the

upper bound critical value. If the computed F-statistics is less than the lower bound

critical value, then the null of no cointegration cannot be rejected.

Pesaran et al. (2001) report the two sets of critical values based on 40,000

replications of a stochastic stimulation which provide critical value bounds for all

classifications of the regressors into purely I(0), purely I(1) or mutually cointegrated

for a sample size of 1,000 observations. However, Narayan (2005) computes the

critical values for bounds for F-test for small samples sizes, which is also used in this

study.

Gregory-Hansen cointegration test

The above ARDL bounds testing approach ignores the issue of any potential structural

break in a cointegrating relationship. As with the unit root tests, Kunitomo (1996) argues

that, in the presence of structural change, traditional cointegration tests which do not

allow for a structural break may produce “spurious cointegration results”. Gregory and

Hansen (1996) also show that the ADF test tends to “under-reject” the null hypothesis of

no cointegration in the presence of a structural break. Gregory and Hansen address the

problem of estimating cointegration relationships in the presence of a structural break

by introducing a residual-based technique. The Gregory-Hansen methodology tests for

the null hypothesis of no cointegration against the alternative of a cointegrating

relationship in the presence of a potential break. The advantage of the Gregory and

Hansen (1996) methodology is that, this testing procedure determines the time of the

break endogenously[5]. In other words, the break point (TB) is unknown and is

determined by finding the minimum values for the ADF t statistic.

By taking into account the existence of a potential unknown and endogenously

determined one-time break, the Gregory-Hansen approach allows for structural shifts

in either the intercept alone, in both the trend and the level shift or for a full break.

Thus, they present three models for testing cointegration allowing for the existence of a

structural break in the cointegrating vector.

The first model, known as a level shift model (Model C) contains an intercept and

a level shift dummy as follows:

y1t ¼ u1 þ u2 w1t þ a T y2t þ et

t ¼ 1; . . . ; n:

ð6Þ

�The second model (C/T) contains an intercept and a trend with a level shift dummy:

y1t ¼ u1 þ u2 w1t þ bt þ a T y2t þ et

t ¼ 1; . . . ; n:

ð7Þ

Saving and

investment

The third model is the full break model, called a regime shift (C/S); this allows for

changes in both intercept and slope, as follows:

y1t ¼ u1 þ u2 w1t þ aT1 y2t þ aT2 y2t wtt þ et

t ¼ 1; . . . ; n:

ð8Þ

143

Model C/S includes two dummy variables, one for the intercept and one for the slope.

In the context of our analysis, y1t and y2t are the saving and investment rates; u1 and

a1 are the intercept and slope coefficients before the shift; u2 and a2 denote the changes

to the intercept and slope coefficients at the time of the shift. The dummy variable is

denoted by w1r and is defined by:

w1t ¼ 0; if t # ½ht� and w1t ¼ 1; if t . ½ht�

where the unknown parameter t 1(0,1) denotes the relative timing of the change point.

6. Empirical findings

Unit root results

This study uses annual data from 1963 to 2007 for Saudi Arabia. The data for gross

domestic saving, gross domestic investment and GDP are obtained from the World

Bank (2008), World Bank World Tables. The data for gross domestic saving and gross

domestic investment are measured as a proportion of GDP, consistent with the

Feldstein and Horioka (1980) study. To ascertain the order of integration, we first

conduct the traditional ADF and PP unit root tests. These tests suggest that both the

variables in the model are non-stationary (Refer to Table I).

Since the ADF and PP tests suffer from power deficiency in the presence of a

structural break, we also apply Perron’s (1997) AO model to the data. The results

reported in Table II also find evidence of unit root (non-stationary), confirming the

results computed by the ADF and PP tests. The estimated break date of 1998 for

Description

Saving rate

Investment rate

ADF test statistics

Result

Unit root

Unit root

21.3592

22.5947

PP test statistics

2 1.4261

2 2.6991

Result

Unit root

Unit root

Note: Critical value at the 5 percent level is 2 3.5155

Description

k

Tb

Saving rate

Investment rate

8

6

1998

1979

Test statistic

2 2.6774

2 3.5523

Table I.

ADF and PP unit root test

results

Result

Unit root

Unit root

Notes: Critical values at the 1, 5 and 10 percent are 2 5.45, 24.83 and 24.48, respectively; the

maximum k ¼ 8

Table II.

AO model for

determining the break

date

�SEF

28,2

144

saving and 1979 for investment correspond with real events in Saudi Arabia. The 1979

break for the investment rate coincides with the oil price shock, the Iranian revolution

and the energy crisis. The structural break for the saving rate in 1998 coincides with

the economic and financial reforms that took place in Saudi Arabia. During this period,

the country experienced large budget deficits associated with low oil prices worldwide.

The local currency was also subject to a wave of speculation leading the government

to intervene to prop up the currency (Dibooglu and Aleisa, 2004). This period

also coincided with the Asian financial crisis of 1997 which negatively affected

Saudi Arabia in particular and the Gulf region in general.

Cointegration results

To investigate the existence of a long-run relationship in equation (1), we estimate

equations (4) and (5). As explained earlier, the ARDL bounds testing procedure involves

the comparison of the computed F-statistics with the critical values. Both the computed

F-statistics of 1.7538 and 4.1662 (given in Table III) are less than the lower bound critical

values given by Pesaran et al. (2001) and Narayan (2005). As the computed F-statistics

are below the lower bound critical value at the 5 percent significance level, the null of

no cointegration cannot be rejected. Therefore, no evidence exists for a long-run

relationship between saving and investment in Saudi Arabia.

The Gregory-Hansen procedure for cointegration in the three models (equations 6-8)

is estimated to test for the existence of a long-run relationship between saving

and investment with an endogenously determined structural break. The results and

the critical values are reported below in Table IV. The results for all the three models

(C, C/T, and C/S) indicate that the null of no cointegration cannot be rejected at the

5 percent significance level. The break dates of 1976, 1983, and 1984 detected by the

Gregory-Hansen procedure correspond with the oil crisis leading to the world recession,

and the reforms that occurred in Saudi Arabia during the mid 1970s and early 1980s[6].

This finding is consistent with the result of the ARDL bounds testing cointegration

approach, leading to conclusion that no long-run relationship exists between saving and

investment. As per Feldstein and Horioka, evidence of no correlation between the two

Table III.

F-test for testing the

long-run relationship

between saving and

investment

Computed F-statistics (FBounds) 2 F(S/I)

Computed F-statistics (FBounds) 2 F(I/S)

Critical bounds for n ¼ 45 from Narayan (2005)

Critical bounds from Pesaran et al. (2001)

UCB: 7.91

UCB: 7.30

Note: Critical bounds from the two authors are from Table CI v Case V with unrestricted intercept and

trend in the model

Model

Table IV.

Gregory-Hansen

cointegration test with

structural break

1.7538

4.1662

LCB: 7.08

LCB: 6.56

C

C/T

C/S

Break point

ADF

Critical value at 5%

1976

1983

1984

2 2.62

2 4.11

2 2.92

24.61

24.99

24.95

Note: The null hypothesis being no cointegration between saving and investment

Source: Critical values are provided by Gregory and Hansen (1996)

Result

Do not reject H0

Do not reject H0

Do not reject H0

�variables indicates a high degree of international capital mobility for Saudi Arabia. This

result is consistent with many other studies including AbuAl-Foul (2006), Chaudhri and

Wilson (2000), Sachsida and Mendonça (2006), and Kollias et al. (2008) but it contradicts

the studies by Jansen (1996), Isaksson (2001), and Ang (2007).

Overall, our empirical results indicate that no relationship exists between saving

and investment in the long-run and thus, capital is highly mobile in Saudi Arabia. This

is plausible given the country has undergone tremendous financial and economic

reforms during the last few decades These reforms have led to massive capital inflows,

dominated by oil revenue flows to the Saudi government. However, other investment

and private inflows into the assets markets have also increased recently, especially

with the country’s accession to the World Trade Organization in 2005. Further to this,

foreign direct investment sharply increased registering at US$18 billion in 2006, with

the stock of foreign direct investment accounting for US$48 billion in 2006 (Al-Jasser

and Banafe, 2009).

7. Summary and conclusion

The aim of the paper is to examine the long-run relationship between saving and

investment as a criterion for assessing international capital mobility. Saudi Arabia is a

suitable case given that, it is the largest economy in the Middle Eastern and Arab nations

and a heavily oil-dependent country. The approach adopted here follows the Feldstein

and Horioka (1980) study and applies various stationarity and cointegration tests. These

include the traditional ADF and PP unit root tests as well as the Perron’s (1997)

stationary test with an endogenously determined structural break. For robustness, we

also apply two cointegration procedures, to test for the long-run relationship between the

saving and investment, the ARDL bounds testing procedure and the Gregory and

Hansen (1996) cointegration method.

Our empirical results from both the cointegration procedures suggest that no

long-run relationship exists between saving and investment, indicating the presence of a

high degree of capital mobility in Saudi Arabia for the 1963-2007 period. The absence of

this relationship is plausible as the country has undergone financial and economic

reforms leading to massive capital inflows, which are dominated by oil revenue flows to

the Saudi government. This chain of events has been reinforced with the country’s

accession to the World Trade Organization during 2005 which saw increases in other

investment and private inflows into assets markets. The effect of capital being highly

mobile for an oil dependent country of Saudi Arabia is consistent with the Feldstein and

Horioka proposition. But, this conclusion cannot be generalized for all oil-dependent

countries and thus further research on the capital mobility issue is needed for other

oil-dependent countries.

Notes

1. Austria, Belgium, Germany, Greece, Italy, Luxembourg, Spain, and the UK.

2. Egypt, Jordan, Morocco, and Tunisia.

3. Broad money is defined as M3 (which consists of money circulation plus deposits savings

and other deposits) plus quasi-monetary deposits.

Saving and

investment

145

�SEF

28,2

4. Numerous cointegration studies employ the ARDL model instead of the traditional

maximum likelihood test based on Johansen (1988) and Johansen and Juselius (1990). These

studies include Bahmani-Oskooee and Nasir (2004), Narayan (2005), and Kollias et al. (2008).

5. The Gregory and Hansen (1996) test is applicable only for I(1) processes. The ADF, the PP

and the AO unit root tests all show that both the saving rate and investment rate are I(1).

146

6. The break dates given by the Perron (1997) unit root test are somewhat different from those

given by the Gregory and Hansen (1996) cointegration test. The different break dates occur

because the Perron (1997) unit root test searches for a break in individual series, while the

cointegration test searches for a break in the residual of two series.

References

AbuAl-Foul, B. (2006), “The relationship between savings and investment in MENA countries”,

paper presented at the 42nd Annual MBAA/ABE Conference in Chicago, IL.

Albatel, A. (2003), “Money, finance and economic growth the case of Saudi Arabia”, available at:

www.erf.org.eg/cms.php?id¼conferences_details&conference_id¼5 (accessed October 24,

2008).

Al-Jasser, M. and Banafe, A. (2009), “Capital flows and financial assets in emerging markets:

determinants, consequences and challenges for central banks”, available at: www.bis.org/

publ/bppdf/bispap44v.pdf (accessed February 12, 2009).

Al-Rajhi, A., Al-Salamah, A., Malik, M. and Wilson, R. (2003), Economic Development in

Saudi Arabia, Routledge, London.

Ang, J. (2007), “Are savings and investment cointegrated? The case of Malaysia (1965-2003)”,

Applied Economics, Vol. 39, pp. 2167-74.

Apergis, N. and Tsoulfidis, L. (1997), “The relationship between saving and finance: theory and

evidence from E.U. countries”, Research in Economics, Vol. 51 No. 4, pp. 333-58.

Arginon, I. and Roldan, J. (1994), “Saving, investment and international capital mobility in EC

countries”, European Economic Review, Vol. 38 No. 1, pp. 59-67.

Bahmani-Oskooee, M. and Nasir, A. (2004), “ARDL approach to test the productivity bias

hypothesis”, Review of Development Economics, Vol. 8 No. 3, pp. 483-8.

Baxter, M. and Crucini, M. (1993), “Explaining savings investment correlations”, American

Economic Review, Vol. 83 No. 3, pp. 416-36.

Chaudhri, D. and Wilson, E. (2000), “Savings, investment, productivity and economic growth of

Australia 1861-1990: some explorations”, The Economic Record, Vol. 76, pp. 55-73.

Coakley, J., Kulasi, F. and Smith, R. (1996), “Current account solvency and the Feldstein-Horioka

puzzle”, Economic Journal, Vol. 106 No. 436, pp. 620-7.

Cooray, A. and Sinha, D. (2007), “The Feldstein-Horioka model re-visited for African countries”,

Applied Economics, Vol. 39 No. 12, pp. 1501-10.

Dibooglu, S. and Aleisa, E. (2004), “Oil prices, terms of trade shocks, and macroeconomic

fluctuations in Saudi Arabia”, Contemporary Economic Policy, Vol. 22 No. 1, pp. 50-62.

EIU (2007), Country Profile Saudi Arabia, Annual Report, Economist Intelligence Unit, London.

Engle, R. and Granger, C. (1987), “Co-integration and error correction: representation estimation

and testing”, Econometrica, Vol. 55 No. 2, pp. 251-76.

Feldstein, M. and Horioka, C. (1980), “Domestic savings and international capital flows”,

The Economic Journal, Vol. 90, pp. 314-29.

Ghatak, S. and Siddiki, J. (2001), “The use of ARDL approach in estimating virtual exchange

rates in India”, Journal of Applied Statistics, Vol. 28 No. 5, pp. 273-583.

�Gregory, A. and Hansen, B. (1996), “Tests for cointegration in models with regime and trend

shifts”, Oxford Bulletin of Economics and Statistics, Vol. 58 No. 3, pp. 555-60.

Ho, T. (2000), “Regime switching investment-savings correlations and international capital

mobility”, Applied Economics Letters, Vol. 7 No. 9, pp. 619-22.

Isaksson, A. (2001), “Financial liberalisation, foreign aid, and capital mobility: evidence from

90 developing countries”, Journal of International Financial Markets, Institutions and

Money, Vol. 11 No. 3, pp. 309-38.

Jansen, W. (1996), “Estimating saving-investment correlations: evidence for OECD countries

based on an error correction model”, Journal of International Money and Finance, Vol. 15

No. 5, pp. 749-81.

Johansen, S. (1988), “Statistical analysis of cointegration vectors”, Journal of Economic Dynamic

and Control, Vol. 12, pp. 231-54.

Johansen, S. (1991), “Estimations and hypothesis testing of cointegration vectors in Gaussian

vector autoregressive models”, Econometrica, Vol. 56 No. 6, pp. 1551-80.

Johansen, S. (1995), Likelihood-Based Inference in Cointegrated Vector Autoregressive Models,

Oxford University Press, New York, NY.

Johansen, S. and Juselius, K. (1990), “Maximum likelihood estimation and inference on

cointegration with application to the demand for money”, Oxford Bulletin of Economics

and Statistics, Vol. 52 No. 2, pp. 169-210.

Kasuga, H. (2004), “Savings-investment correlations in developing countries”, Economics Letters,

Vol. 83 No. 3, pp. 371-6.

Kollias, C., Mylonidis, N. and Paleologou, S. (2008), “The Feldstein-Horioka puzzle across EU

members: evidence from the ARDL bounds approach and panel data”, International

Review of Economics and Finance, Vol. 17, pp. 380-7.

Kunitomo, N. (1996), “Tests of unit roots and cointegration hypotheses in econometric models”,

Japanese Economic Review, Vol. 47 No. 1, pp. 79-109.

Miller, S. (1988), “Are saving and investment cointegrated?”, Economic Letters, Vol. 27 No. 1, pp. 31-4.

Murphy, R. (1986), “Productivity shocks, non-traded goods and optimal capital accumulation”,

European Economic Review, Vol. 30 No. 5, pp. 1081-95.

Narayan, P. (2005), “The savings and investment nexus for China: evidence from cointegration

tests”, Applied Economics, Vol. 37 No. 1, pp. 1979-90.

Narayan, P. and Narayan, S. (2003), “Savings behaviour in Fiji: an empirical assessment using

the ARDL approach to cointegration”, Discussion Papers 02/03, Monash University,

Melbourne.

Perron, P. (1989), “The great crash, the oil price shock, and the unit root hypothesis”,

Econometrica, Vol. 57 No. 16, pp. 1361-401.

Perron, P. (1997), “Further evidence on breaking trend functions in macroeconomic variables”,

Journal of Econometrics, Vol. 80 No. 2, pp. 355-85.

Pesaran, M. (1997), “The role of economic theory in modelling the long-run”, Economic Journal,

Vol. 107 No. 1, pp. 178-91.

Pesaran, M., Shin, Y. and Smith, R. (2001), “Bounds testing approaches to the analysis of level

relationships”, Journal of Applied Econometrics, Vol. 16 No. 3, pp. 289-326.

Sachsida, A. and Mendonça, M. (2006), “Domestic saving and investment revised: can the

Feldstein-Horioka equation be used for policy analysis?”, Discussion Papers 1158, Instituto

de Pesquisa Econômica Aplicada – IPEA.

Saving and

investment

147

�SEF

28,2

148

SAMBA (2008), “Saudi’s Arabia’s 2008 budget, 2007 performance”, available at: http://www.

samba.com/GblDocs/sa2008_en.pdf (accessed November 28, 2008).

Wong, D. (1990), “What do savings-investment relationships tell us about capital mobility?”,

Journal of International Money and Finance, Vol. 9 No. 1, pp. 60-74.

(The) World Bank (2008), World Bank World Tables, The World Bank, Washington, DC.

About the authors

Reetu Verma is a Lecturer in the School of Economics at the Faculty of Commerce at the

University of Wollongong. She completed her Honours, Master’s and PhD in Economics at the

University of Wollongong, Australia. She has published extensively in reputable international

journals (for example, ASEAN Economic Bulletin, The Middle East Business & Economic Review,

and South Asia Economic Journal ).

Ali Salman Saleh is a Senior Lecturer and Coordinator for postgraduate studies by research at

the School of Economics and Finance, Victoria University, Australia. He completed his Master’s

and PhD in Economics at the University of Wollongong, Australia. Dr Saleh has published

extensively in reputable international journals (for example, Journal of Policy Modeling,

Singapore Economic Review, and the Asia Pacific Journal of Economics and Business). His current

research interests concentrate on the areas of applied economics, and development issues in

small and medium enterprises.

To purchase reprints of this article please e-mail: reprints@emeraldinsight.com

Or visit our web site for further details: www.emeraldinsight.com/reprints

�

Dr. Reetu Verma

Dr. Reetu Verma